Net Interest - Insuring the Unknown

Happy New Year! Welcome back to another issue of Net Interest, my newsletter on financial sector themes. This one’s about the reinsurance industry. If it’s not something you know much about, it’s worth reading because it carries lessons into investing. Also, if you’re not already a paid subscriber, please do sign up: You’ll be able to unlock the archive and receive weekly updates on other topics – this week Blackstone, Crypto Banks and Citadel Securities. For most people in finance, January 1st is a day to gear up for the year ahead. For those in the reinsurance industry, however, it is a chance to wind down. While others enjoy a festive lull during the last two weeks of December, reinsurance professionals remain hard at work, finalising customer contact renewals. By the time January 1st comes around, it’s all done. The process kicks off every September at a three-day conference in Monte Carlo. Representatives from across the insurance industry gather in a cluster of the most prestigious hotels around the Place du Casino to discuss where to set pricing and other terms for the year ahead. Insurance companies rely on reinsurers to lay off risk. Passing some of their risks onto reinsurers allows them to underwrite larger risk limits on individual policies and a greater number of policies overall. It can also help them reduce earnings volatility and manage their capital more effectively. The transfer of risk to a reinsurer requires the primary insurer to pay a premium; the conference provides a forum for insurers and reinsurers to begin thrashing out what that should be. Of over $7 trillion in worldwide insurance premium volume, around 5% hits the reinsurance market every year. Although a relatively small proportion, it covers the largest and most complex risks in the insurance system – war, natural disaster, severe recession. Around half the market comes up for renewal every January, which means that in the months between Monte Carlo and year-end, reinsurance underwriters are at their busiest. Efforts in the run-up to this year’s renewal date were particularly challenging. “The market has faced a very late, complex and in many cases frustrating renewal,” said one broker. The reason, according to another, is that the world has become a riskier place. The war in Ukraine and extreme weather events in the US and Europe reduced reinsurers’ risk appetite at the same time as inflationary pressure boosted demand from primary insurers. As a result, prices went up. According to reinsurance broker Howden, global property catastrophe prices rose by 37% on January 1st, 2023, their biggest annual increase since 1992. Some segments saw even higher price rises. According to broker Gallagher Re, rate increases in global aerospace rose by 150-200%. We discussed the nature of aviation insurance in Who Owns All the Planes back in March; it seems a lot of the risk was passed down to reinsurers and they are now reevaluating how they price it.

But what do these prices mean? In traditional financial markets, prices contain some information about the future. Even in insurance, premiums reflect the probability a policyholder might make a claim. No surprise that my 19-year old son pays more for his auto policy than me: 23% of drivers aged between 18 and 24 have an accident within two years of passing their test. That data point gives insurance companies a useful handle on how to price risk. Reinsurance is harder to frame in this way, especially in the catastrophe segment where the key variables are unknown. Natural disasters do share some statistical properties. Researchers Charles Richter and Beno Gutenberg showed in 1949 that the relationship between the number and size of earthquakes follows a power law distribution: There are many small impact events and fewer large impact events and their relative frequencies follow a consistent distribution. Other researchers showed similar patterns in the distribution of forest fires and landslides, and in the number of casualties in whole wars, global terrorist events and war events. These analyses tell us how many ‘big ones’ may be likely, but not when they will hit. Reinsurance companies are left dealing with unknowns. Such uncertainty is beyond that considered in traditional models of finance. Indeed, this is the very reason primary insurers shy from such risks. “It’s the unknown unknowns that we have to think about,” says a senior executive in a large insurance company explaining the purpose of reinsurance. “By buying reinsurance we’re transferring the risk of what we don’t know, what we don’t understand. And if we don’t buy enough cover, then we could have some very nasty shocks.” For the reinsurer, this provides an opportunity. The one thing you can say about natural disasters is that no-one has an inside edge on when and how severely they will strike. The issue of adverse selection that arises in other areas of insurance doesn’t apply – everybody has the same information. Reinsurers don’t need to worry that the insured party knows more than they do; all they need to focus on is how they manage the risks they assume. One person who does this very well is Warren Buffett. Berkshire Hathaway’s Reinsurance EmpireOver the years, Warren Buffet has built Berkshire Hathaway into one of the largest reinsurance companies in the world. In 2021, it ranked fifth behind Munich Re, Swiss Re, Hannover Re and Lloyd’s by gross premiums written. But Buffett wasn’t always good at reinsurance. He launched his first reinsurance operation in 1969, hiring George Young, “a gentle, professorial man”, to run it. Earnings were initially very strong. The firm entered the market at a time when rates had risen substantially and capacity was tight, leading to exceptional profitability in 1971. However, the market soon turned and George Young didn’t manage it well. “Net, counting the value of float, it was not a good business for us for 15 years,” said Buffett in 2011. “It’s not an easy business. It looks easy most of the time.” The reason it looks easy most of the time is that most of the time big losses don’t occur. Buffett explains in his 1997 shareholder letter (emphasis added throughout):

Buffett suffered from the poor business he wrote in the 1970s for many years. “After more than 20 years, [we] regularly receive significant bills stemming from the mistakes of that era,” he wrote in his 1995 shareholder letter. “A bad reinsurance contract is like hell: easy to enter and impossible to exit.” In 1986, Buffett recruited Ajit Jain into his insurance business to help turn things around. Jain developed an expertise in underwriting very large catastrophic loss events. Jain is now Vice Chairman of Insurance Operations for Berkshire Hathaway and Buffett reserves his highest praise for him, once saying that the search expenses that brought Ajit Jain to Berkshire was the highest return investment he’d ever made. The pair developed a number of principles to help guide them through the reinsurance market: First, they avoid over-specifying risk. The dice example illustrates a point but real-life probabilities are fuzzier to gauge. In 1997, Berkshire wrote a policy for the California Earthquake Authority that others wouldn’t touch. It put the firm on the hook for a potential loss of up to $600 million:

Unlike other investors, Buffett recognises that states and probabilities in the world are more vague than models often discount. He captures this another way in his observation that “the earthquake doesn’t know the premium you receive”. “You know, you don’t have somebody out there on the San Andreas Fault that says, ‘Well, he only charged a 1 percent premium so we’re only going to do this once every 100 years.’” Second, they adopted an organisational structure capable of holding unknowable risk. With precision pricing not available to mitigate risk, other tools are required and organisational structure is a big one. Berkshire’s 1989 shareholder letter explains:

That year, Berkshire advertised that it would write up to $250 million of catastrophe coverage. It recognised some probability that it could lose the full $250 million in a single quarter but, with a balance sheet large enough to absorb it, the loss would be “a blow only to our pride, not to our well-being.” In addition, Buffett reckons that his diversified overall business interests makes him a better underwriter of reinsurance risk than pure play firms. As he said at his 1994 shareholder meeting:

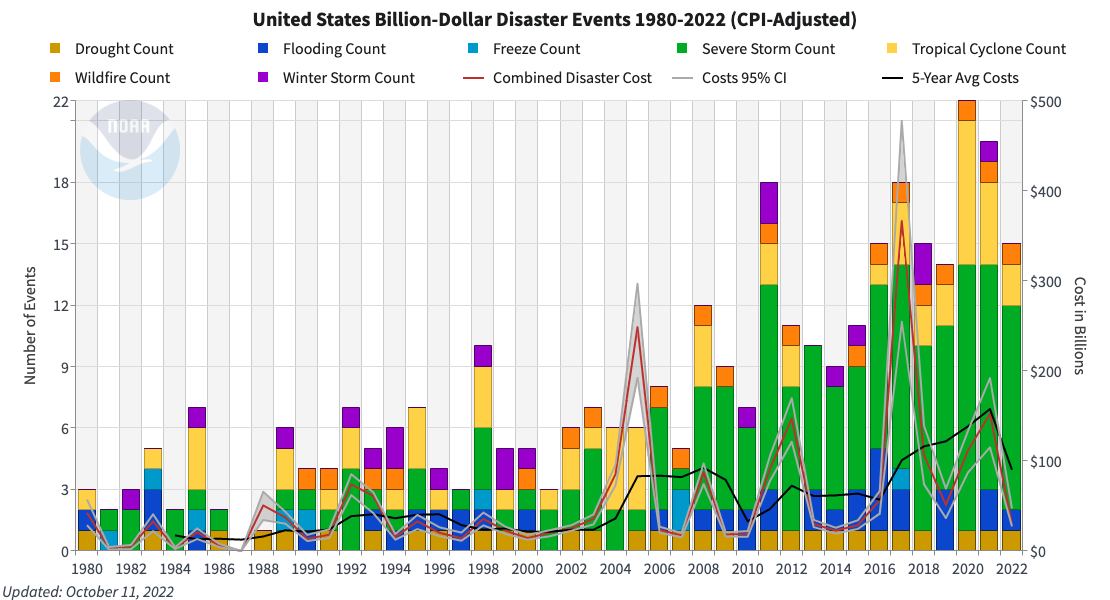

Third, Berkshire’s ability to dip in and out of the market allows it to ride the reinsurance cycle and Buffett and Jain have a keen understanding of the cycle. Because pricing is not as forward-looking as in other financial markets, it becomes a function of capacity. And when times are good and losses are low, capacity tends to swell; it’s only when losses hit that it retracts. Buffett was talking about insurance when he first wrote (in his 1992 shareholder letter): “It's only when the tide goes out that you learn who's been swimming naked.” He was referring to Hurricane Andrew which caused the largest insured loss in history up to that time, wiping out a few small insurers. It’s a strange thing to observe the insurance cycle. Everyone knows hurricanes are a persistent feature of the environment, so why would capacity increase after a few benign years and retrench as soon as a storm hits? It can’t be that insurers are always extrapolating the present? In the aftermath of Hurricane Andrew in 1992, prices for the global property catastrophe market increased by 65%, yet that risk was by then in the rear view mirror. The reason is that reinsurers react to the capital they have available. Large payouts following a natural catastrophe deplete reinsurers’ capital, lowering the global capital supply to the industry. Firms respond by pushing up prices to replenish capital. How high they rise depends on how much capital is available in the industry globally and how unexpected the loss event was. Through this process, cycles serve to stabilise longer-term capital flows in a market where losses remain unknown until after the fact. The current hardening of prices reflects a lot of capacity having been taken out of the market over recent years. Broker Howden estimates that $66 billion of capital erosion took place in 2022, the biggest squeeze on reinsurance capital since 2008. The firm states that “the mismatch between supply and demand was already estimated to be in the tens of billions of dollars when Hurricane Ian hit Florida as a category 4 storm to reinforce one of the hardest reinsurance markets in living memory.” Berkshire Hathaway itself withdrew some capacity in October, according to Insurance Insider. But it’s not just Hurricane Ian. There is a sense that natural catastrophes are growing more severe. In the last 30 years, eight hurricanes have hit the US wreaking over $30 billion of insured losses each – from Andrew in 1992 ($31 billion) through to Ian in 2022 ($55 billion). That’s more than what risk modellers would typically expect. In the first nine months of 2022 alone, there were fifteen separate billion-dollar weather and climate disaster events in the US (ten severe storm events, two tropical cyclones, the Kentucky/Missouri flooding, the Western/Southern Plains drought/heatwave and Western wildfires).

The key debate facing the reinsurance industry is whether recent price hikes are sufficient to cover such heightened risk. Investing vs InsuringFor investors, the reinsurance industry provides a useful case study. It’s no coincidence Warren Buffett excels at both investing and insurance. The synergy between the two is conventionally seen in the context of insurance “float” – a topic we discussed in Other People’s Money – but a reinsurance framing of the world helps on the investing side, too. In particular, it instils a framework to price unknown risks. Nassim Taleb is a big fan of the reinsurance approach to risk. “This is a beautiful industry. I marvel at the sophistication of insurance,” he told an insurance industry conference a few years ago. “They make mistakes when they go to finance. The AIG problem was entirely a finance problem not an insurance problem.” In particular, Taleb praises insurers for knowing how to limit extreme – low frequency, high severity – losses so they don’t spiral out of control with tools like exclusions, caps, limits and pricing adjustments:

The reinsurance industry isn’t immune from risk. The Lloyd’s crisis of the 1990s casts a long shadow. But it manages it pretty well and higher prices can only help. Thanks for reading! If you enjoyed this piece, please hit the “Like” button. Better yet, join the community by signing up as a paid subscriber! You’re on the free list for Net Interest. For the full experience, become a paying subscriber. Read Net Interest in the app Listen to posts, join subscriber chats, and never miss an update from Marc Rubinstein.

|

Older messages

Generation Rent

Friday, December 9, 2022

Plus: Trafigura, Sberbank, FlatexDEGIRO

The New Conglomerates

Friday, December 2, 2022

Plus: S&P Global, Financial Services Comp, Blackstone

Printing Money and More

Friday, November 25, 2022

Printing Money, Equity Research, Petershill, Credit Suisse

Circle of Trust

Friday, November 18, 2022

Plus: Norinchukin, Jefferies, Ergodicity

The Latest Domino to Fall

Friday, November 11, 2022

Plus: Sculptor Capital Management, Goldman Sachs, Retail Trading

You Might Also Like

Longreads + Open Thread

Saturday, March 8, 2025

Personal Essays, Lies, Popes, GPT-4.5, Banks, Buy-and-Hold, Advanced Portfolio Management, Trade, Karp Longreads + Open Thread By Byrne Hobart • 8 Mar 2025 View in browser View in browser Longreads

💸 A $24 billion grocery haul

Friday, March 7, 2025

Walgreens landed in a shopping basket, crypto investors felt pranked by the president, and a burger made of skin | Finimize Hi Reader, here's what you need to know for March 8th in 3:11 minutes.

The financial toll of a divorce can be devastating

Friday, March 7, 2025

Here are some options to get back on track ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Too Big To Fail?

Friday, March 7, 2025

Revisiting Millennium and Multi-Manager Hedge Funds ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The tell-tale signs the crash of a lifetime is near

Friday, March 7, 2025

Message from Harry Dent ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

👀 DeepSeek 2.0

Thursday, March 6, 2025

Alibaba's AI competitor, Europe's rate cut, and loads of instant noodles | Finimize TOGETHER WITH Hi Reader, here's what you need to know for March 7th in 3:07 minutes. Investors rewarded

Crypto Politics: Strategy or Play? - Issue #515

Thursday, March 6, 2025

FTW Crypto: Trump's crypto plan fuels market surges—is it real policy or just strategy? Decentralization may be the only way forward. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

What can 40 years of data on vacancy advertising costs tell us about labour market equilibrium?

Thursday, March 6, 2025

Michal Stelmach, James Kensett and Philip Schnattinger Economists frequently use the vacancies to unemployment (V/U) ratio to measure labour market tightness. Analysis of the labour market during the

🇺🇸 Make America rich again

Wednesday, March 5, 2025

The US president stood by tariffs, China revealed ambitious plans, and the startup fighting fast fashion's ugly side | Finimize TOGETHER WITH Hi Reader, here's what you need to know for March

Are you prepared for Social Security’s uncertain future?

Wednesday, March 5, 2025

Investing in gold with AHG could help stabilize your retirement ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏