|

The University of California claims part of its mission is to serve society and provide public service for California and the nation. But as today’s featured story reveals, that mission didn’t stop the university’s board of regents from delivering a $4.5 billion bailout to a giant Wall Street real estate fund that’s planning on ramping up rent increases and evictions amid a housing crisis already wreaking havoc on the public university’s students and staff. The Lever holds the powerful accountable through reader-supported investigative journalism that corporate media will not undertake. Join in our mission by becoming a paid supporting subscriber, and get great perks in return. Rock the boat.

The University of California Bails Out Eviction-Happy Private Equity

By Matthew Cunningham-Cook  Blackstone UC Investment (AP Photo/Mark Lennihan) [View in browser] As the world’s largest private equity firm faces potential losses from a cloudy real estate market, its executives blocked jittery investors from withdrawing their money from one of its real estate funds, while insisting that rent increases and evictions will bolster returns. Now, the Blackstone Group’s real estate investment trust has received a multibillion-dollar bailout from a source whose employees and students are already suffering through the housing crisis: California’s public university system. Just months after Blackstone’s real estate investment trust purchased America’s largest owner of private student housing, the same trust received a $4.5 billion infusion from the University of California’s Board of regents, two of whom have close ties to the company. The investment rewards the financial firm only a few years after the company and its executives spent $5.6 million to kill California ballot initiatives that would have expanded rent control in the state. Blackstone, a firm that’s valued at $111 billion and manages $991 billion in assets, also faces broader headwinds in its real estate sector. The profits that the firm distributes to shareholders plunged 36 percent last year, driven by real estate losses. Effectively, University of California (UC) is funneling cash into privatized student housing and corporate landlords — doubling down on a controversial investment strategy that comes with a massive layer of fees and Wall Street profits — instead of doing its part to address a growing housing crisis, one that affects its students and employees. 💡 Follow us on Apple News and Google News to make sure you see our stories first, and to help make sure others see our breaking news as well. In 2021, five percent of UC students, or more than 14,000, experienced homelessness, while the university’s unions report that many of their mostly blue-collar members simply cannot make ends meet due to California’s spiraling cost of rental housing. The latest episode revolves around the Blackstone Real Estate Income Trust, or BREIT. In August 2022, BREIT purchased 69 percent of American Campus Communities (ACC), the country’s largest student housing company, in a $12.8 billion deal. ACC’s business model is built around rent revenues; in January 2022 the company’s CEO boasted that it was “experiencing the most substantial fundamental tailwinds we've seen in many years” thanks in part to soaring rents. ACC has apartments at the University of California, Berkeley, and the University of California, Irvine. Five months after this acquisition, the UC Regents pumped $4.5 billion into BREIT. Around the same time, Blackstone spent more than $150,000 in the final quarter of 2022 on lobbying UC for more investment dollars, doubling the amount it spent the previous quarter. In December, Nadeem Meghji, Blackstone’s head of real estate for the Americas, told CNBC in December that UC’s unprecedented bailout of BREIT “changed the narrative” around the fund. In December, Blackstone began blocking redemptions to investors, after it received an influx of redemption requests. But that didn’t stop Blackstone from distributing to itself more than $200 million in management fees in the fourth quarter of 2022, a Lever review of Securities and Exchange Commission (SEC) filings show. Between management and performance fees, Blackstone extracted more than $1.5 billion in fees from the $50 billion fund in 2022. Blackstone CEO Stephen Schwarzman earned $1.3 billion in 2022 and has a net worth of $30.7 billion, according to Bloomberg, and is a major donor to Republican candidates. Now, in a nearly unprecedented coordinated intervention, the university’s labor unions — representing 110,000 workers — have called on UC to divest itself not just from the university’s holdings in the Blackstone real estate fund, but all of the university’s $6.5 billion invested in Blackstone holdings. “Essentially UC is investing in a corporation that further drives UC’s own workers’ housing insecurity,” said Kathryn Lybarger, the President of AFSCME Local 3299, which represents blue collar and health care workers at the University of California. “The bottom line is that people’s housing should not be a basis for making a profit, especially when it’s a public institution like UC. We’re demanding they divest and it’s on the scale of divesting from South Africa in the ‘80s. We’re talking about housing as a human right, not as an investing opportunity.” Blackstone’s Housing PlayReal estate investment trusts are pools of investor-backed cash that purchase real estate. While pension funds routinely invest in both REITs and private equity real estate, it is extremely uncommon to have a pension effectively do a bailout of a fund facing massive redemption requests. Blackstone’s BREIT differs substantially from the $1.3 trillion real estate investment trust, or REIT, market. Nearly all REITs are publicly traded, which means that investors can cash out their money at will. This is not the case with BREIT, which allows Blackstone to suspend redemptions. In response to questions from The Lever, Blackstone spokesman Jeffrey Kauth noted in an email that “BREIT is not a mutual fund and has never gated. It is a semi-liquid product and is working exactly as planned.” “Gating” refers to a practice by hedge funds and private equity where redemptions are entirely blocked, as opposed to just partially blocked, like with BREIT. Blackstone is the largest private landlord in the country, owning 300,000 units across the United States. In California alone, Blackstone and its affiliates, including BREIT, own at least 9,000 housing units, including concentrations in San Diego, Los Angeles, Sacramento, and the Bay Area, according to research done by the Private Equity Stakeholder Project.  | Learn All Our Investigative Tricks |  | Score a copy of our Citizens’ Guide to Following the Money and Holding the Powerful Accountable, free with a paid subscription. The e-book gives you all the tools and tricks our reporting team uses to scrutinize power. | |

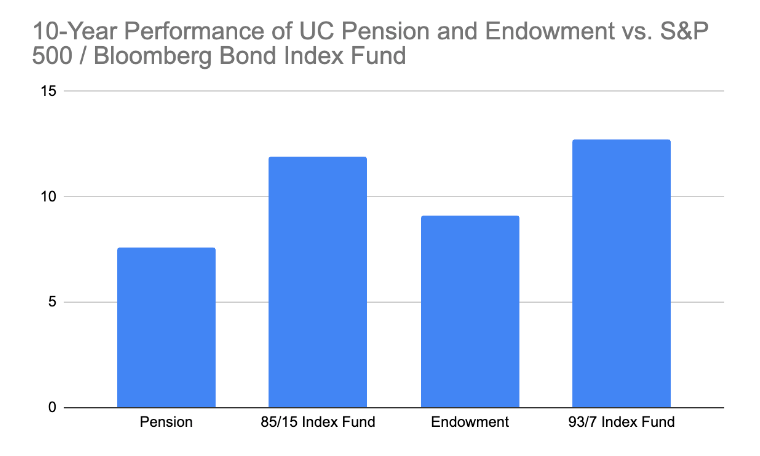

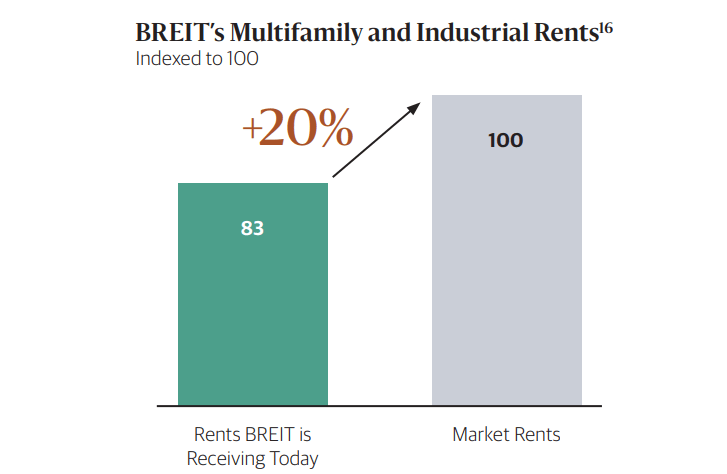

Those units tend to be located in lower-income census tracts, where on average residents make roughly 25 percent less than the state’s median household income. Over the past few years, BREIT has also made a play into mobile home parks, acquiring nearly 6,000 units are in the San Diego area, where Blackstone has been routinely jacking up listed rents by 40 percent or more. Escalating housing costs are integral to Blackstone’s business strategy. “Our major concern with Blackstone is that this is a company whose model for making money for investors is to buy up rental properties and raise the rent,” said Lybarger at AFSCME. Blackstone spent more than $5.6 million opposing a 2018 ballot initiative that would have allowed California cities to implement new rent control measures. In 2019, the UN accused Blackstone of “wreaking havoc” in the housing market by its aggressive pursuit of evictions and higher rents. Some tenants have successfully fought back as it seeks to expand its presence in the housing market, however. In January, tenants at the StuyTown complex in New York City successfully fought an effort to raise rents, and in San Diego, Blackstone tenants have formed a union. “We believe we have the most favorable resident policies among any large landlord in the U.S., including not making a single non-payment eviction for over two years during COVID,” noted Kauth in his email.“We operate in accordance with California’s rent stabilization laws and are investing $100 million to make these communities better places to live.” But some BREIT tenants say that if anything, the trust’s massive foray into housing has been anything but beneficial. One tenant, Michael McBride, says that since BREIT purchased his apartment complex in Chula Vista outside of San Diego a couple of years ago, basic maintenance has fallen by the wayside. It took “at least” a month for BREIT to fix the heat in his apartment after he had complained about it in winter. “I just got heat inside my apartment,” he said. “Now my front room thermostat is not working, and we’re having water issues — it smells like bleach. Something needs to be done.” BREIT currently owns 66 apartment buildings in San Diego County. BREIT’s approach has lately faced turbulence. Because the fund is substantially indebted – it carries $90 billion in debt on $140 billion in total assets — even small downturns like the recent economic decline put the fund in jeopardy, since both gains and losses are magnified because of high leverage. What’s more, BREIT has a small but significant portion of its holdings in the office and retail sector, which have been battered in the post-pandemic economy. Earlier this month, BREIT sold two office towers in Orange County, California, for 36 percent less than it paid for them nine years ago. Multifamily housing like that owned by BREIT has also faced headwinds as the Federal Reserve has repeatedly raised interest rates, which make it more difficult for potential buyers — typically other real estate investment trusts or private equity firms — to purchase housing. Sales of apartment buildings fell by two-thirds in the most recent quarter, according to data from the CoStar Group. Such upheaval has led many BREIT investors to get cold feet. In March, BREIT received $4.5 billion in redemption requests, but only fulfilled $666 million of them. But now, UC has come to the rescue. In January, the university announced it was investing $4.5 billion in the struggling fund — which in effect allows it to start refunding other investors’ money. “I Have To Make Some Capitalistic Decisions”UC’s pension system is fairly unique in that workers have no power over how investment decisions are made. All decisions are made by the regents, which are appointed by the California governor for 12-year terms. One of the main decision-makers behind the plan to pump billions of UC dollars into Blackstone was Richard Sherman, chair of the UC Investment Committee, who has strong connections to the investment firm. On January 3, Sherman announced in a Blackstone press release, “This type of large, opportunistic investment effectively leverages the UC’s more than $150 billion portfolio to benefit the 600,000 students, faculty, staff, and pensioners from our 10 campuses and six academic health centers.” Sherman, who heads up music mogul David Geffen’s investment office, collaborated with Blackstone on the 2012 buyout of music publisher EMI. What’s more, the late Blackstone co-founder Pete Peterson purchased his New York penthouse from Geffen in 2007. An additional member of the eleven-person Investment Committee, Mark Robinson, also has ties to Blackstone. Robinson is a partner at investment banking firm Centerview Partners, which advised Blackstone on a $2.2 billion acquisition in 2021. On behalf of the Regents, the investment was launched by Jagdeep Singh Bachher, UC’s Chief Investment Officer — who has been accused of making investments in response to pressure from individual Regents with conflicts of interest in the past. In 2018, he invested an unprecedented $240 million into a fund meant for high-net-worth individuals headed by the former chair of the Regents’ Investment Committee, Paul Wachter. According to Kauth, the Blackstone spokesperson, “The UC Investments team saw [Blackstone President] Jon Gray speaking on CNBC in December and reached out to Blackstone to see if they could be helpful by deploying capital in a way that would create a win-win. Following the initial call, UC Investments did extensive diligence on the portfolio and as a result of that process, decided to invest $4 billion in the fund. To suggest that the investment was the result of anything other than robust diligence is a complete mischaracterization.” Kauth added, “Blackstone has never had a corporate PAC or made corporate donations to political candidates. The firm has always been bipartisan, and all of our executives’ political donations are strictly personal.” Schwarzman pumped $20 million into the SuperPACs of Congressional Republicans in the 2022 election and was a major adviser to Donald Trump. In response to uproar over UC’s investment in Blackstone, Baccher played it off as a zero-sum game of capitalism. “The job of this team day in and day out is to pick assets that are going to be accretive to future generations and future retirees,” Bachher said at a Regents meeting in March. “And to do that... I have to make some capitalistic decisions. And that decision around Blackstone... was purely an investment decision for the benefit of the UC... and to help the needs of our pensioners and our endowment.” But a Lever review of UC’s performance under Bachher’s leadership shows that his “capitalistic“ investment decisions have resulted in the university’s pension and endowment funds massively trailing a plain vanilla index fund of stocks and bonds. Had the pension fund pursued a lower-risk index fund strategy for the last decade — the kind advocated by Warren Buffett — it would now boast $32 billion more in its coffers, or 40 percent more than its current value. Likewise, the university’s endowment fund would have an additional $6.4 billion in its coffers, or 36 percent increase of its current value. In response to a request for comment from The Lever, the university spokesperson stated that a substantial portion of the UC’s investment approach was in index funds. They did not answer questions about poor fund performance under Bachher’s leadership, and Bachher declined an interview with The Lever. According to Kauth, “UC Investments’ recent commitment to BREIT builds upon its 15-year partnership with Blackstone. Before its recent investment in BREIT, UC Investments had already invested $2 billion in Blackstone funds for more than a decade and has a deep working relationship across the entire firm.” “A Meaningful Increase In Economic Occupancy”While Blackstone likes to emphasize that it halted all non-payment evictions during the height of the pandemic, that policy is no longer in place. UC’s bailout came just as Blackstone began ramping up evictions. The Financial Times reported at the end of January that Blackstone’s global real estate head had said that the firm was “seeing a meaningful increase in economic occupancy as we move past what were voluntary eviction restrictions that had been in place for the last couple of years,” acknowledging that the removal of eviction restrictions has allowed Blackstone to improve its cash flow. The article also stated that consultants working with Blackstone had reached out to local elected officials in California to say that Blackstone planned on restarting eviction proceedings that had been dormant during the COVID-19 pandemic. Research from the Private Equity Stakeholder Project in March found that Blackstone launched eviction proceedings against a tenant in Orange County, Florida, for being one month late on rent. Additionally, Blackstone declared in December reporting from SeekingAlpha that what they were charging for rents could go 20 percent higher in the multifamily and industrial sectors if they charged what they considered to be “market rates.”  Blackstone BREIT showcasing its intention to raise rents An estimated 2.5 million Californians are cost burdened in paying their rent, meaning that they spend more than 30 percent of their income on housing, according to a report produced at the end of February by the California Legislative Analyst’s Office.

Help us spread the word! Please forward this email to family and friends. Was this email forwarded to you? Sign up for free to receive original reporting like this in your inbox every day.

|