|

There’s a major bank heist afoot — one in which the banks are swindling folks just like you. In today’s featured story below, David Sirota lays out how banks are making billions off the yawning gap between the paltry rates they pay you in interest and the much higher rates they earn from other institutions when they loan out your money — and thanks to the Federal Reserve hiking interest rates, that gap keeps getting bigger. The Lever holds the powerful accountable through reader-supported investigative journalism that corporate media will not undertake. Join in our mission by becoming a paid supporting subscriber, and get great perks in return. Rock the boat.

The Great Bank Robbery Of 2023

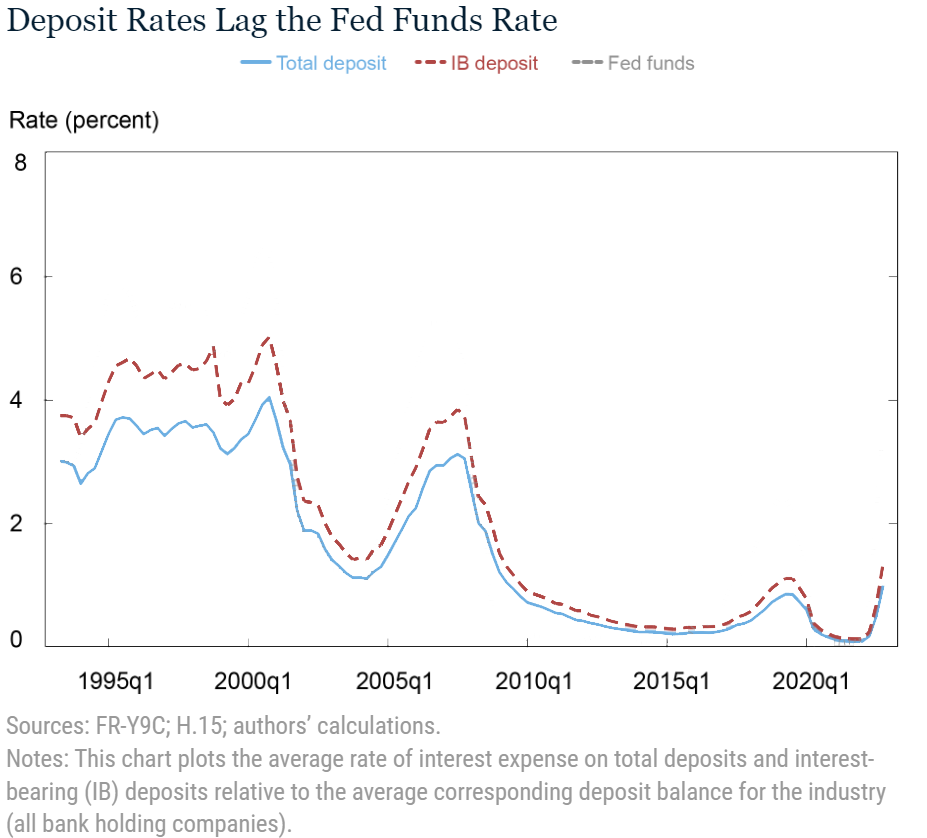

By David Sirota  Illustration by Lindsay Ballant/The Lever [View in browser] “It is easier to rob by setting up a bank than by holding up a bank clerk.” — Bertolt Brecht The last time you checked your bank statement, did you take a moment to look at the fine print that shows the interest rate you are being paid on your deposits? If you did, you may have noticed that it still seems pretty negligible, even though you’ve seen so many headlines about the Federal Reserve hiking the interest rates that banks charge for loans. This is the Great Bank Robbery of 2023 — the yawning gap between what you are paid on your deposits and what banks are earning from other institutions when they loan out your money. It’s a caper that has quietly become a systemic upward transfer of wealth thrumming beneath the macroeconomy — but as you’ll see below, the theft can be stopped. This particular heist is predicated on an asymmetry: Banks collect depositors’ money and pay them very little interest, while using depositors’ money to earn a lot more interest when the Federal Reserve raises lending rates. Banks can earn those higher yields by making high-interest loans to borrowers. They can also take advantage of the Fed’s own interest rates for interbank lending or for simply parking their excess reserves at the central bank — and those rates are not available to the general public. 💡 Follow us on Apple News and Google News to make sure you see our stories first, and to help make sure others see our breaking news as well. This spread isn’t new — the basic business of a bank is to collect deposits, pay depositors’ some interest, and then make loans at higher interest rates, with the difference used to pay for bank services (tellers, ATM machines, etc.) and generate a fair profit from such “net interest income.” The larceny here is in the size of the gap between what banks are paying savers and what banks can earn through the Federal Reserve. That spread is now “at a modern high,” according to a recent Fed report. In an $18 trillion deposit market, that means savers are missing out on hundreds of billions of dollars that are being skimmed off their nest eggs and funneled to bankers and their shareholders. It means bank statements showing almost no interest payments on your deposits, while a series of recent earnings reports show banks reaping ever-higher profits from net interest income. “The banks are getting free money from depositors to make loans and investments with, but savers aren’t getting any share of the gains,” former Federal Reserve counsel and current Cornell University professor Robert Hockett told The Lever. “Exploiting The Higher Interest Rate Environment”Federal Reserve Chairman Jay Powell has said his interest rate hikes aim to “get wages down” — and that has started to happen. But typically the other effect of such hikes is a boost in bank profits. “When interest rates rise, profitability in the banking sector increases,” Investopedia explains. “Banks make money by accepting cash deposits from their customers in return for interest payments and then investing that money elsewhere. The bank’s profit is the difference between the interest they pay their depositors and the yield they make through investing. Higher interest rates increase the yield on their investments.” The current moment is an extreme example of this axiom: Big banks are reaping outsized payouts from net interest income because the spread between depositor payment rates and interest rates has become so enormous. Last month, the Federal Deposit Insurance Corporation reported that banks are on the whole paying a 0.4 percent interest rate to depositors. At the same time, banks get paid on average more than 7 percent when they are making 30-year fixed rate mortgage loans. They are also being paid more than 5 percent of interest when they park money at the Federal Reserve — and the Fed does not require banks to pass on those government payments to depositors in the form of higher interest payments. Now zoom in and look at just the country’s five biggest banks, where the government’s too-big-to-fail guarantees entice depositors with special promises of safety that aren’t extended to customers of other financial institutions. There, the Wall Street Journal estimates that since 2019, depositors have missed out on more than $290 billion worth of interest they might have earned at better interest rates at other banks or in different financial vehicles. For Americans needing basic banking services, this translates into predation. As Sen. Jack Reed (D-R.I.) noted in a recent letter spotlighting the scheme, a new Bank of America customer will receive about “0.01 percent on a savings account, but pay 6.90 percent on a mortgage and 15 percent to 27 percent on a credit card.” Not surprisingly, that bank just reported $14 billion in net interest income in the most recent quarter — a 25 percent increase. “The biggest banks are exploiting the higher interest rate environment to benefit their executives and shareholders, not the ordinary Americans whose deposits provide the funding necessary for those banks to operate,” Reed wrote in his letter to bank CEOs, demanding to know “why your bank still pays the same very low interest rates on deposits even as it makes giant profits by charging borrowers higher interest rates on loans.” This is no fleeting anomaly, nor is it a bug — it is a feature. A Federal Reserve study in 2013 found that while banks are quick to lower payments to depositors when government interest rates decline, they are slow to raise those payments when interest rates increase. The analysis found that if the speeds of change were similar in either direction, depositors would earn roughly $100 billion a year more than they do in periods with rising market rates. The discrepancy means the $100 billion is instead pocketed by banks and their shareholders. 🎥 Follow us on YouTube to see all of our latest video reports and filmed podcast segments. Too Big To Fail = Too Big To Pay A Fair RateSeven large banks responded to Reed’s inquiry with letters arguing that the giant yield from the gap between their high loan rates and low deposit payments isn’t naked profiteering, but is instead paying for exceptional services for customers. “Clients value the breadth and depth of the relationship for reasons that go beyond the rates paid for deposits,” wrote Bank of America in a typical response. “This includes, but is not limited to, our best-in-class digital and mobile capabilities that provide our customers with the ability to complete necessary banking services such as depositing a check or transferring money in a safe and secure manner, wherever they may be located.” The argument parrots talking points from the Bank Policy Institute, the industry’s lobby group, which insists: “Deposits come with payment services — the ability to transmit or receive funds, transfer balances between accounts or withdraw cash, usually at no additional fee to the customer. All of these differences are reasons why deposit rates should be expected to be below the fed funds rate” — i.e., the Fed-created interbank interest rate that banks themselves have access to but individual depositors don’t. While it’s true that the spread between loan rates and deposit rates provide banks with resources to provide basic services, it doesn’t explain why that spread is at a record high. After all, higher interest rates do not mean banks suddenly need to spend more on ATM machines, tellers, and customer website portals. In truth, three factors have created this ripoff. First and foremost, after a long era of lax antitrust enforcement, the banking industry has become monstrously consolidated, to the point where just 15 banks control more than three quarters of all deposits in America. When these major banks insisted in their letters to Reed that they offer “competitive rates,” that was technically true but also wildly deceptive — they are the oligopolies that collusively set the parameters of the competition. “The market is dominated by a small number of big players,” wrote Frederic Malherbe, an economist at University College London. “It may be the case that no major player has an incentive to deviate and offer higher rates, as long as the others do not either.” Second, these oligopolies not only face little serious competition for depositors, they also benefited from $5 trillion of new deposits after customers placed emergency stimulus payments and PPP checks into their accounts. That means banks have felt little immediate pressure to compete for depositors by offering higher rates. “Banks are likely to allow excess deposits to run off before re-pricing deposits upward, which should support net interest income and margins,” wrote Fitch analysts last year. As Bankrate’s chief financial analyst told CNBC last year: “The biggest banks in particular are sitting on a mountain of deposits, the last thing in the world they’re going to do is raise what they’re paying on those deposits.” At an investor presentation late last month, JPMorgan Chase’s chief financial officer boasted about how little pressure the too-big-to-fail behemoth now feels to pay depositors any more of the spread. “We are not going to chase every dollar of deposit balances,” he declared, as JP Morgan is now projected to rake in $84 billion of net interest income. With this let-them-eat-cake attitude so pervasive in the banking sector, why aren’t more Americans flipping off the big players and chasing better yields at smaller banks or with different investment vehicles? That gets to the third factor: customer stickiness. Simply put, after a long era of near-zero interest rates, Americans are not conditioned to shop their deposits, and the process itself can be a byzantine, time-consuming morass of paperwork and esoterica. Additionally, as financial panics generate headlines about midsized banks teetering on the brink of collapse, depositors may be generally hesitant to move. They may also be particularly averse to depart the too-big-to-fail banks because of the government’s implicit backstop guarantees that are not offered to other financial institutions. Meanwhile, as the Bank Policy Institute notes, the rise of automatic payments and direct deposits “may have made deposit relationships stickier” — once you’ve taken the time to set up your family’s banking process, you probably don’t want to go through the pain in the ass of doing it all over again at another bank, even if you might be able to get slightly higher interest payments. There’s a classic collective action problem at play here, too. For the more than half of Americans who have less than $5,000 in savings, a few more points in interest only translates to a few more bucks a year, so it may not seem worth the hassle to change banks. But when that is multiplied over millions of customers and transactions in an $18 trillion deposit market (think: Superman III and Office Space) those few bucks add up to billions of dollars of upward wealth transfer from non-rich savers to bank executives. The result: Even as banks refuse to pass on more of their interest profits to depositors, “customers remain loyal to their primary bank in high proportions,” as a J.D. Power executive told Investopedia. Summarizing the situation, the chief economist at Raymond James said: “It will take a very, very large increase in rates to make people really change banks…People either don’t know or they are too lazy to go and open up an account in a different bank.” Giving Americans The Same Interest Rates That Banks EnjoyPaying almost nothing to depositors while lending out their savings at high interest rates is a dream come true for bankers. As a Deloitte report put it: “Such economic calculus makes sense: why not grow interest income while keeping interest expenses under control?” For everyone else, though, this is a scam. Short of nationalizing the banking system, what can be done about such a systemic rip off? Plenty. For one thing, you can go take a look at the interest rate — or APY — on your own savings and checking accounts and compare it to the 5 percent interest rate that your bank now gets when it deposits your money at the Fed. If the spread is preposterously large, you can start looking for better treatment somewhere else. If you keep the amount under $250,000 or use an insured cash sweep to spread deposits around (not necessary for most Americans, who don’t have a quarter million dollars lying around), you can get the same government guarantee of safety that the too-big-to-fail banks enjoy. You can also explore moving your money into different financial instruments (Treasury ladders, money market mutual funds, etc.) that could pay better interest rates — which more savers are now doing. Indeed, in the last 16 months, almost $1 trillion of deposits have flowed out of commercial banks — and much of that is probably savers searching for better yield. Slowly, this capital flight is starting to exert at least some pressure on bank CEOs to stop treating depositors’ savings as free money that they don’t have to pay for. One too-big-to-fail bank, Citi, is already feeling the squeeze to pass on more of its yields to savers. In its report on the record-high spread between the federal funds rate and deposit interest rates, the Fed predicts that more banks will follow the same path. As Axios put it after three big banks saw deposit outflows: “For the first time in a long time, banks are going to compete to pay you more for your money.” Good. Beyond the righteous public shaming that Reed, the Rhode Island senator, engaged in, lawmakers and regulators could also start championing specific policies that would make a difference. For example, regulators can ignore Treasury Secretary Janet Yellen’s push for more bank consolidation, and they can stop listening to finance industry advocacy groups like the Bank Policy Institute, whose lobbyist told Politico he wants government officials to declare that “midsize banks need to be allowed to merge and be acquired potentially by larger banks.” (Sidenote: the lobbyist’s quote appeared in a Politico newsletter edition that was literally “presented by the American Bankers Association,” yet another bank lobby group). Instead, regulators can start blocking bank mergers. More consolidation reduces consumer-benefiting competition between banks to offer lower-interest loans and higher-interest deposit payments. Moreover, Malherbe asserts that central banks could make the special interest rates they offer to commercial banks contingent on those banks treating the public more fairly — something British regulators are now considering. “The solution is simple: Make interest payment on reserves conditional on banks passing the higher rates to depositors,” he writes, adding that “the central bank could set a maximum margin as a condition.” Even better would be measures helping individual depositors access the same government-provided interest rates that commercial banks already enjoy. Right now, the Federal Reserve says it “provide(s) financial services to banks and governmental entities only [and] individuals cannot, by law, have accounts.” This means Americans get doubly screwed: While the Fed’s higher interest rates jack up borrowers’ loan costs, savers cannot access the high deposit interest rates that the Fed pays to banks. That law, though, can change via the Roosevelt Institute’s proposal to create so-called FedAccounts, in which every American could open their own Fed account that “would pay the same interest rate that commercial banks receive on their balances.” In effect, savers would be able access the government-guaranteed interest rate that private banks right now exclusively enjoy, rather than being bilked by private profit-skimming banks offering far lower interest payments to the public. There is also Hockett’s proposal to expand the existing TreasuryDirect program, which already lets Americans set up accounts to buy savings bonds and T-bills. Hockett says that existing law allows the Biden administration to use executive action to quickly turn these into full-fledged bank accounts with digital wallets and transaction capabilities. “Banks’ profits derive from the ‘spread’ between low-interest borrowings — that is, client deposits and higher-yield investments (such as) Treasuries,” he recently wrote in The Financial Times. “Thanks to cutting out the middlemen, these digital Treasury bank accounts, provided they are held to maturity, would pay far more interest than ordinary bank accounts do.” Those middlemen, though, are among the most powerful forces in Washington. For years, bank lobbyists have successfully blocked even the most modest proposals for public banking options, and the industry’s spending in elections is designed to deter lawmakers from any serious reform efforts. No doubt, any legislation designed to protect savers would prompt bank CEOs to quickly funnel some of their skyrocketing net interest income into a well-funded opposition campaign. Those bankers understand the truism best summarized in the television show Mr. Robot: “Give a man a gun and he can rob a bank. Give a man a bank and he can rob the world.” But with such a huge gap between deposit and loan interest rates, the question now is: How much robbery is the world willing to tolerate?

|