Why the Poor Stay Poor in America - Do We Need A Federal Usury Law?

Welcome to Crime and Punishment: Why the Poor Stay Poor in America. I’m thrilled that you signed up to read my newsletter, and I hope that together, we can make a difference. “Usury is the act of lending money at an interest rate that is considered unreasonably high or that is higher than the rate permitted by law. Usury first became common in England under King Henry VIII and originally pertained to charging any amount of interest on loaned funds. Over time it evolved to mean charging excess interest, but in some religions and parts of the world charging any interest is considered illegal.” Investopedia

I don’t think that banks or other lending institutions should be banned from charging some interest on loans, rather it is a matter of how much interest is enough for the lender, and how much is too much for the borrower. Lenders want to make the highest profit possible, so the sky’s the limit on interest rates from their perspective. Unfortunately, the borrower has no control over interest rates…unless millions rise up and demand a federal cap on lender rates, for example, and elected officials listen and respond with legislation. I don’t know if millions of low-wage or average-salaried worker have rallied for a cap, but there is currently a Senate Bill sponsored by the Chairman of the Senate Banking Committee, Ohio’s own Senator Sherrod Brown, and Senator Jack Reed, a Democrat from Rhode Island, to reintroduce the “Veterans and Consumers Fair Credit Act, legislation to extend the Military Lending Act’s 36% interest rate cap to cover veterans and all Americans.” I think this is a good idea and a good start. As of July of this year, 18 states and DC have enacted rate caps that supposedly prevent at least the exorbitant rates of payday loans, but a federal law is needed to not only provide consistency, but to close the shocking loopholes in state laws. Although California is one of the states that has capped lender interest rates, this article from the LA Times explains the need for federal legislation by highlighting the major loopholes in its own state law: according to the state’s own attorney general, all of California’s banks, savings and loan, credit unions, finance corporations or even a pawnbroker are exempt from the usury law. It makes you wonder who exactly is covered? Your Aunt Mable? When I began to get behind on my mortgage and my credit score plummeted as a result, I started to notice lots of personal loan and credit card offers arriving in the mail. I had no idea why lenders were urging me to take on more debt, when I couldn’t pay the debt I already had. This is why.

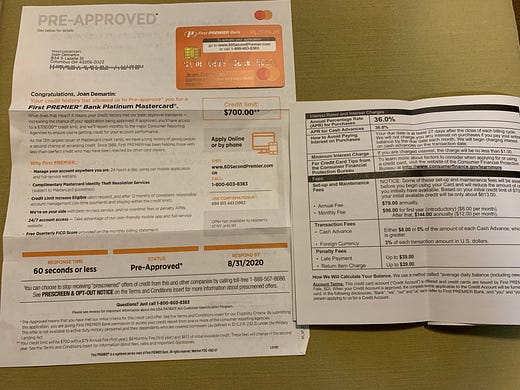

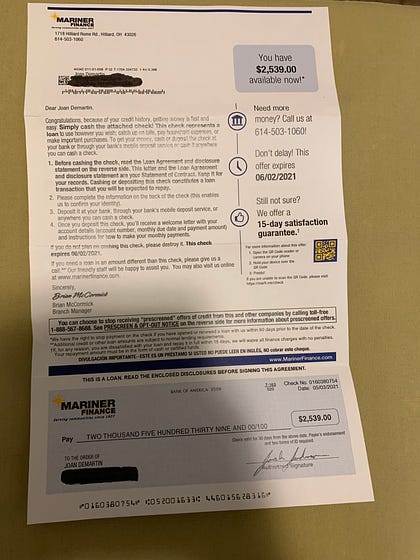

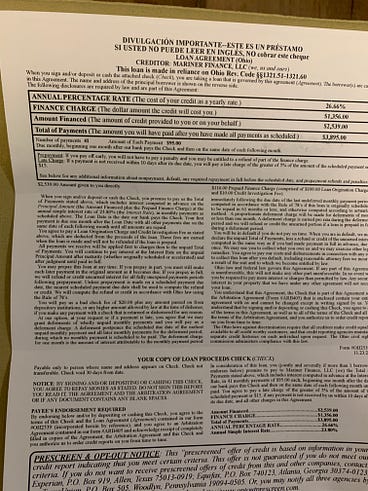

I showed you this photo in a previous post discussing the bankruptcy conundrum, and it works just as well here to illustrate what I consider to be a usury interest rate plus fees. The reason I believe 36% to be a usury rate and those on the Senate banking committee don’t, could be because of the cruel irony of our system: those who are already comfortable don’t need to borrow at all, let alone at this rate. If you have enough money to at least pay all of your bills, then you likely have a higher credit score which, in turn, earns you a much lower interest rate if you borrow at all. The banks target individuals in financial trouble because they know who are desperate for cash or credit. That’s why it’s called “predatory lending”. And by comparison to a “Pay Day” loan which can reach 300% interest or higher, this credit card offer of 36% interest plus annual fees is a bargain. In addition to credit card offers, I continue to receive offers for personal loans, but this one has a twist: it’s a real check. I also mentioned this scheme in a previous post, because I actually cashed the one I received a few years ago and paid the horrendous interest rate plus fees for well over a year before I was able to pay it off. Fortunately, I’m not desperate for cash at the moment and was able to save this recent offer just to show you a close-up of the interest rates and fees.

If you read the fine print, and you should, you'll see you will owe $95/month for 41 months— that’s three years and five months you will pay just about $100 every month for $2,500 cash now, and you will pay nearly one half of the loan amount in interest and fees. And although there is no penalty for an early payoff of the loan, the fine print states that if you pay off the loan early, “you may be entitled to a refund of part of the finance charge.” (emphasis added). I guarantee that if you asked the lender what it meant by this statement, you would hear crickets. And because it uses the word “may” and has no additional explanation, it is most likely legally meaningless. In other words, don’t expect a refund. The bank makes sure it gets it’s full finance charge amount, regardless of when you pay off the loan. In fact, it really doesn’t matter to the lender if you default. According the the National Consumer Law Center,

Do you think we need a federal usury law that caps lender rates? Should this cap be 36% as proposed in the current Senate bill or even lower? Please share your thoughts in the comment section below. If you like this post, why not share it with your friends and family? And please consider a free or paid subscription and here’s why: You’re on the free list for Crime and Punishment: Why the Poor Stay Poor In America. All posts are free for now, but if you’d like to get ahead of the crowd, feel free to support my work by becoming a paid subscriber. © 2021 Joan DeMartin Unsubscribe

|

Older messages

Sunday Evening Reads

Friday, December 24, 2021

The Power of Lobbyists

Credit Scores:

Friday, December 24, 2021

Listen now (11 min) | Does This Almighty Three-Digit Number "Level the Playing Field" Or Punish The Poor?

You Might Also Like

The Best Thing: March 4, 2025

Wednesday, March 5, 2025

The Best Thing is our weekly discussion thread where we share the one thing that we read, listened to, watched, did, or otherwise enjoyed recent… ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Miley Cyrus Ditched Her Bombshell Waves For A New Haircut At The Oscars After-Party

Wednesday, March 5, 2025

Love an impulsive hair moment. The Zoe Report Beauty The Zoe Report 3.4.2025 (Beauty) Miley Cyrus 2025 Oscars (Celebrity) Miley Cyrus Ditched Her Bombshell Waves For A New Haircut At The Oscars After-

Organic farmers expose RFK Jr.'s delusion

Tuesday, March 4, 2025

Turns out you can't "Make America Healthy Again" when the fossil fuel industry calls the shots. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Build Muscle and Burn Fat by Fixing These 4 Workout Mistakes

Tuesday, March 4, 2025

View in Browser Men's Health SHOP MVP EXCLUSIVES SUBSCRIBE Build Muscle and Burn Fat by Fixing These 4 Workout Mistakes Build Muscle and Burn Fat by Fixing These 4 Workout Mistakes You can achieve

New from Tim — "Dr. Keith Baar, UC Davis — Simple Exercises That Can Repair Tendons"

Tuesday, March 4, 2025

The latest from author and investor Tim Ferriss ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

5 Easy Ways to Make Your Old Car Look New(er) 🚗

Tuesday, March 4, 2025

Use TikTok's 'Rage Cleaning' Trend to Get Your Place Spotless. Your car has served you reliably for years—and it looks it. Here's how to roll back the clock and make it look new. Not

Sydney Sweeney Debuted A New “Light Suede” Hair Color At The Oscars After-Party

Tuesday, March 4, 2025

Plus, your March astrological forecast, your daily horoscope, and more. Mar. 4, 2025 Bustle Daily Idina Menzel on her new Broadway show. EXCLUSIVE Idina Menzel's New Broadway Show Has One Big

How Worried Should We Be About These Measles Outbreaks?

Tuesday, March 4, 2025

Today in style, self, culture, and power. The Cut March 4, 2025 HEALTH How Worried Should We Be About These Measles Outbreaks? Cases have been popping up across the country. We asked a pediatrician to

Starting Next Week: A New Course on Wordsworth

Tuesday, March 4, 2025

Class starts March 13. Enroll today. Upcoming Literary Seminar: Timothy Donnelly on William Wordsworth Dive into the work of one of England's most influential poets. In this three-session seminar

An update on how Trump’s proposed tariffs could raise food costs

Tuesday, March 4, 2025

A Michelin-starred chef backpedals after disparaging retweets