Aziz Sunderji - Mortgage lock-ins: move it and lose it

Mortgage lock-ins: move it and lose itExisting mortgages carry a lower interest rate than new ones. Nobody wants to move, so there is nothing to buy.Hi! I’m Aziz. My newsletter contextualizes economic news using data visualization. These days I’m focusing on housing—let me know what you think by replying to this email.

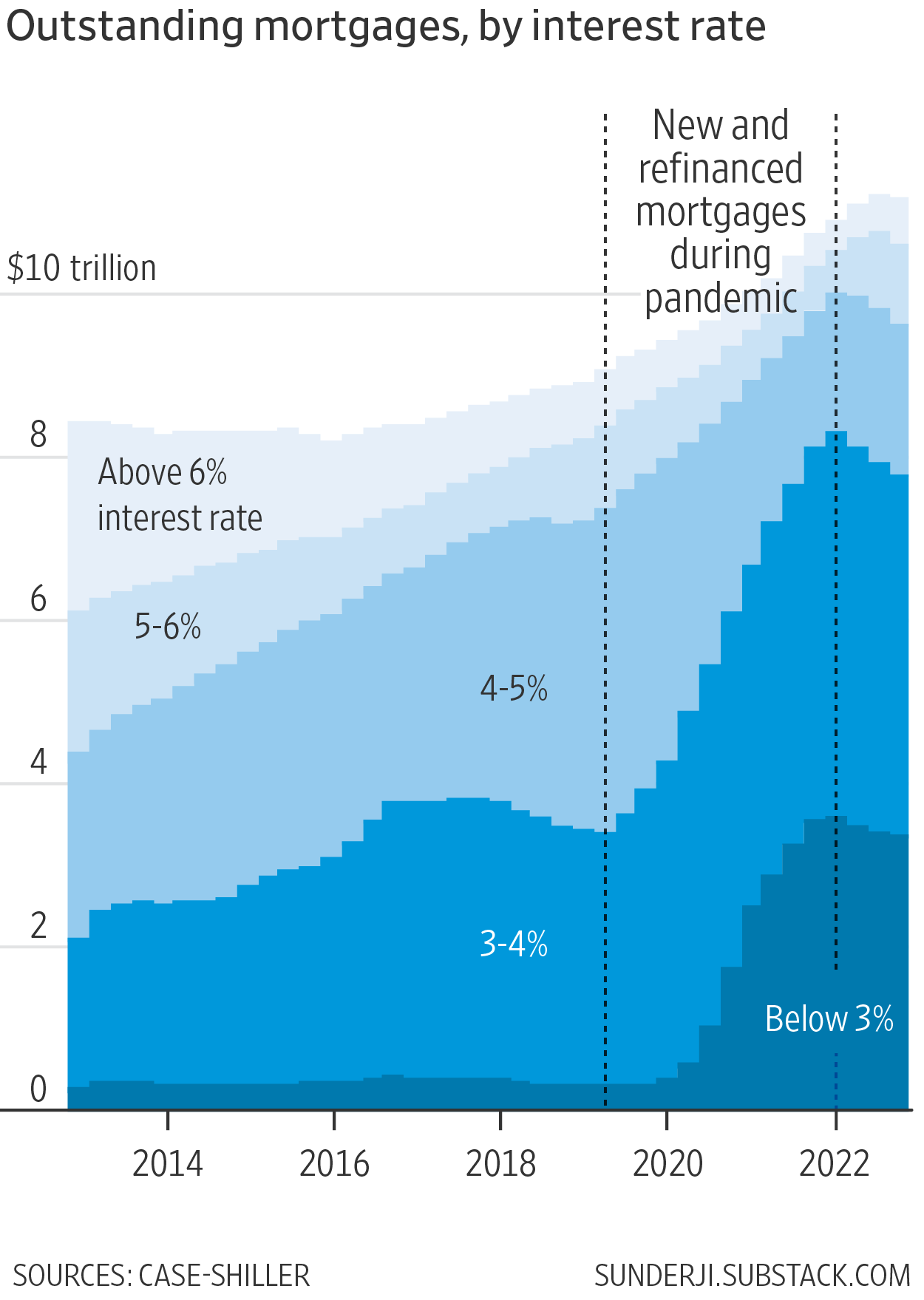

The most notable feature of today’s residential housing market is that inventory for sale is absurdly low. There are only about 600,000 homes on the market, compared to 1.5 million in 2016. This is mostly explained by what’s happening with mortgages:

I don’t have inventory data going back further than 2016, but one might imagine that this dynamic has played out before. When interest rates rise, homeowners with existing low-rate mortgages will always be reluctant to sell. But right now their reticence is especially pronounced because so many reset their mortgages recently at very low rates. This is a result of a few factors. First, the Fed’s emergency measures during the pandemic dropped mortgage rates to unprecedented lows (2.65% for a 30y mortgage in early 2021). Many took advantage. Second, we experienced a lifestyle shift: people wanted more space to work from home, or to move away from cities and work remotely. They bought new homes to suit their new realities. And it wasn’t just home buyers that reset their mortgages—about half of the new, low-rate mortgages came from people refinancing their existing homes. Third, inflation rose rapidly, forcing the Fed to embark on the most aggressive hiking cycle in decades, and pushing interest rates up by a lot, and fast. We haven’t seen a rise in interest rates of this magnitude, let alone this speed, since the early 1980s. Had rates stayed low, people would have no problem selling and snapping up another cheap mortgage—but they’re not cheap anymore. “In the end, fourteen million mortgages were refinanced during the COVID refinance boom, and these refinances will have effects on the mortgage market for years to come.” There are other potential explanations for today’s very low inventory. For example, if a large share of buyers have been first-time buyers—who acquire a home but do not supply one in the transaction—that might explain the dearth of homes for sale. But recent research from the New York Federal Reserve shows that the number of first-time buyers as a share of total buyers has been pretty steady for years. Readers have asked me how they can support my work. You are already supporting me by reading this far, but if you’d like to do more, please consider forwarding this email to your friends, family, and/or colleagues, and following me on instagram and twitter. You can also financially support my coffee and croissant addiction by becoming a paying subscriber. Thanks!

|

Older messages

After booming home prices, a small correction

Thursday, June 1, 2023

Expensive tech-centric cities that rose during the pandemic have recently fallen the most

Waiting for Home Prices to Fall? Don't Hold Your Breath

Tuesday, May 30, 2023

Nominal price drops are rare and short-lived

Inflation, How Do I Measure Thee?

Monday, May 15, 2023

Let me count the ways

Banks grow less willing to lend, boosting the odds of a recession

Monday, May 8, 2023

The Fed raised interest rates by a quarter of a percent last week. The move was widely expected. More surprising was the accompanying press release, which echoed the Fed's prior communication but

A soft landing is more likely after last week's jobs data

Monday, April 10, 2023

Lower inflation usually costs jobs. This time could be different.

You Might Also Like

6 Most Common Tax Myths, Debunked

Saturday, March 8, 2025

How to Finally Stick With a Fitness Habit. Avoid costly mistakes in the days and weeks leading up to April 15. Not displaying correctly? View this newsletter online. TODAY'S FEATURED STORY Six of

Weekend: My Partner Can’t Stand My Good Friend 😳

Saturday, March 8, 2025

— Check out what we Skimm'd for you today March 8, 2025 Subscribe Read in browser Header Image But first: this is your sign to throw away your old bras Update location or View forecast EDITOR'S

Your Body NEEDS to Cardio Row! Here Are Some Options.

Saturday, March 8, 2025

If you have trouble reading this message, view it in a browser. Men's Health The Check Out Welcome to The Check Out, our newsletter that gives you a deeper look at some of our editors' favorite

What Do You Really Need?

Saturday, March 8, 2025

Is opposing consumerism lacking gratitude? ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

“Otway” by Phoebe Cary

Saturday, March 8, 2025

Poet, whose lays our memory still / Back from the past is bringing, ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Cameron Diaz Returned To Fashion Week In A Fabulous Little Red Dress

Saturday, March 8, 2025

WOW. The Zoe Report Daily The Zoe Report 3.7.2025 Cameron Diaz's Asymmetrical Red Dress Lit Up The Stella McCartney Fall 2025 Show (Celebrity) Cameron Diaz Returned To Fashion Week In A Fabulous

5-Bullet Friday — Breaking the Sperm Bank, D-Cycloserine, Tools for Grumpy Elbows, and Wisdom from Seth Godin

Saturday, March 8, 2025

“If you're feeling creative, do the errands tomorrow. If you're fit and healthy, take a day to go surfing. When inspiration strikes, write it down." ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Inside Alex Pereira's Training for Saturday's UFC 313 Showdown

Friday, March 7, 2025

View in Browser Men's Health SHOP MVP EXCLUSIVES SUBSCRIBE Inside Alex Pereira's Training for Saturday's UFC 313 Showdown Inside Alex Pereira's Training for Saturday's UFC 313

Update Your Android Devices Now 🚨

Friday, March 7, 2025

This TikTok Cleaning Method Might Have Broken My Fan. The security update includes fixes for two zero-day exploits. Not displaying correctly? View this newsletter online. TODAY'S FEATURED STORY

EmRata's Itty-Bitty Bikini Just Brought Back This "Cheugy" 2010s Trend

Friday, March 7, 2025

Plus, everything you need to know about Venus retrograde, your daily horoscope, and more. Mar. 7, 2025 Bustle Daily New books from Emily Henry, Karen Russell, and Kate Folk are among Bustle's best