The Generalist - What makes a great acquisition?

What makes a great acquisition?The common wisdom is that most M&A goes south, with reported failure rates of up to 90%. How can CEOs tip the scales in their favor?

Friends, Should Microsoft buy OpenAI? Should Amazon pick up Anthropic? Would it be in the best interests of Substack and X to merge? How about Netflix and Spotify? After missing out on Tesla back in the day, should Apple snap up Rivian and finally make a delightful iMiniVan? There are few more enjoyable business parlor games than partaking in a bout of fantasy M&A. It is, in some respects, an economically consequential version of gossip. Which companies should date, and which should get married? What might happen if they did? What strange new offspring might they be able to create? Behind the frivolity of such questions is a serious matter. Great businesses are almost never only built. They are bought, too. The greatest companies of our generation have leveraged M&A to grow their empires and stretch their borders. But though the right acquisition can unleash riches, it is tricky to get right, with failure rates of up to 90%. I’ve been thinking about the challenges of growing through purchases a great deal over the past year. In part, that’s because I expect we’ll see more acquisitions in the months and years to come as startups that raised during 2021 approach the end of the runway. Today’s piece is an attempt to better understand what a good acquisition looks like – without the benefit of hindsight. What data should the acquisitive CEO look at? What factors should be ignored or emphasized? When is the right time to strike? Let’s jump in. An ask: If you liked this piece, I’d be grateful if you’d consider tapping the ❤️ in the header above. This helps us understand which pieces you like most, and what we should do more of. Thank you! Brought to you by MasterworksThis painting sold for $8 million and everyday investors profited When the painting by master Claude Monet (you may have heard of him) was bought for $6.8 million and sold for a cool $8 million just 631 days later, investors in shares of the offering received their share of the net proceeds. All thanks to Masterworks, the award-winning platform for investing in blue-chip art. To date, every one of Masterworks’ 16 sales out of its portfolio has returned a profit to investors. With 3 recent sales, Masterworks investors realized net annualized returns of 17.6%, 21.5% and 35%. I’ve been investing with Masterworks for years and have really enjoyed using the platform. My portfolio includes shares of paintings by world renowned artists like Picasso, Ruscha, and Rothko. So how does it work? Masterworks does all of the heavy lifting like finding the painting, buying it, storing it, and eventually selling it. It files each offering with the SEC so that nearly anyone can invest in highly coveted artworks for just a fraction of the price of the entire piece. Shares of every offering are limited, but The Generalist readers can skip the waitlist with this exclusive link. Actionable insightsIf you only have a few minutes to spare, here’s what investors, operators, and founders should know about what makes a great acquisition.

Let’s begin with a true story. We can call it A Tale of Two Acquisitions. It was the best of times, it was the worst of times. It was the year of the Eurozone crisis, it was the year of the Queen’s Diamond Jubilee, it was the epoch of Obama, it was the epoch of Putin, it was the season of Curiosity, it was the season of ignorance, it was the spring of Joseph Kony, it was the winter of Hurricane Sandy. In short, it was 2012 – a year of broad and roiling change, a year that included one of the most significant acquisitions of modern times. That spring, two CEOs cast their eyes toward the same target: Instagram. In less than two years, the photo-sharing application founded by Kevin Systrom and Mike Krieger had become a viral sensation, amassing nearly 30 million users. Its avid user base, image-centric functionality, and mobile nativeness made it an appealing target for Twitter CEO Dick Costolo and Facebook’s Mark Zuckerberg. Costolo made the first move. In March of that year, Twitter made overtures to purchase Instagram for $525 million, using a mix of cash and equity. Systrom and Krieger considered the offer – it was, after all, quite a windfall for less than 24 months’ work – before turning it down. Shortly after, Instagram raised a $50 million Series B from Sequoia Capital, valuing the business at $500 million. For a brief interlude, that looked like the end of the drama – Systrom’s startup would stay independent, using its war chest to propel its growth. Then Zuckerberg called. Just three weeks after breaking off its discussions with Twitter, Instagram announced it was joining Facebook for $1 billion. Once again, it involved a mix of cash and stock. According to reports, Costolo and company hadn’t been given a chance to counter; perhaps, if they had, they might have matched or surpassed Facebook’s three-comma concord. Later that same year, stung by Systrom’s rejection, Twitter purchased another upstart social media business. That October, Costolo’s firm paid a mere $30 million to take ownership of video platform Vine. There’s no doubt which proved better value for money. Within four years, Twitter had shuttered Vine. Meanwhile, Facebook had swelled from a $104 billion IPO-debutant to a $330 billion democracy-fraying superbeast. Such frightening, rapid growth could never have occurred without Instagram, with Zuckerberg’s $1 billion outlay looking like a rounding error. Indeed, in 2018, it was estimated that Instagram would be valued at $100 billion as a standalone company. Since that assessment, the app has doubled its monthly active users to over 2 billion. One moral of the story is this: the right acquisition can change everything. A purchaser who finds the perfect business at the ideal time can unlock new markets, establish new moats, stave off decline, and accelerate growth. Think Google snagging YouTube, eBay grabbing PayPal, or Disney devouring Marvel. Another equally true moral: picking the right acquisition is extremely difficult. It requires a mix of vision, operational acuity, financial discipline, cultural awareness, market storytelling, and timing. There’s a reason that management theorist Roger Martin referred to M&A as a “mug’s game in which 70% to 90% of acquisitions are abysmal failures.” While one might quibble with Martin’s methodology or characterization, there’s little doubt that the odds are not in your favor. So, as a CEO driven to forge a generational business, how can you tip the scales in your direction? How can you maximize the possibility of finding the next Instagram while minimizing the chances of selecting the next Vine? (This is a little harsh on Vine! Oh, well.) What should you consider or question when the M&A bankers come calling? In short, what makes a great acquisition? To answer this fundamental question, we’ve reviewed dozens of academic papers on the often murky world of dealmaking, distilling the most interesting findings. Some will confirm your beliefs, while others may defy them. While not a comprehensive literature review by any means, we hope our summations serve as compelling food for thought. Unlock The Generalist’s Premium Newsletter If you haven’t done so already, now is the perfect time to join our premium newsletter Generalist+. For just $19/month, you’ll unlock a collection of new series designed to make you a better investor and technologist. This week, we launched one of those series, “Letters to a Young Investor.” It features a correspondence between me and the legendary Reid Hoffman on the craft of investing. To hear Reid’s stories about backing Airbnb at the seed stage, missing out on Stripe, and developing a “theory of the game” for venture capital – join us today. A heads-up: early bird pricing is $19/month or $200/year. It’s ending soon, so it’s worth signing up today. Extroverted CEOsYou may not have heard of Bud Tribble, but you know his work. In 1980, Tribble joined a small upstart company called Apple Computer, jumping aboard their fledgling Macintosh development team. As well as being one of the on-the-ground architects of the personal computer revolution, Tribble is also the author of one of Silicon Valley’s favorite terms of art: the “reality distortion field” or “RDF.” Tribble coined the phrase to describe boss Steve Jobs’ startling capacity to convince others. As another early Apple employee remarked:

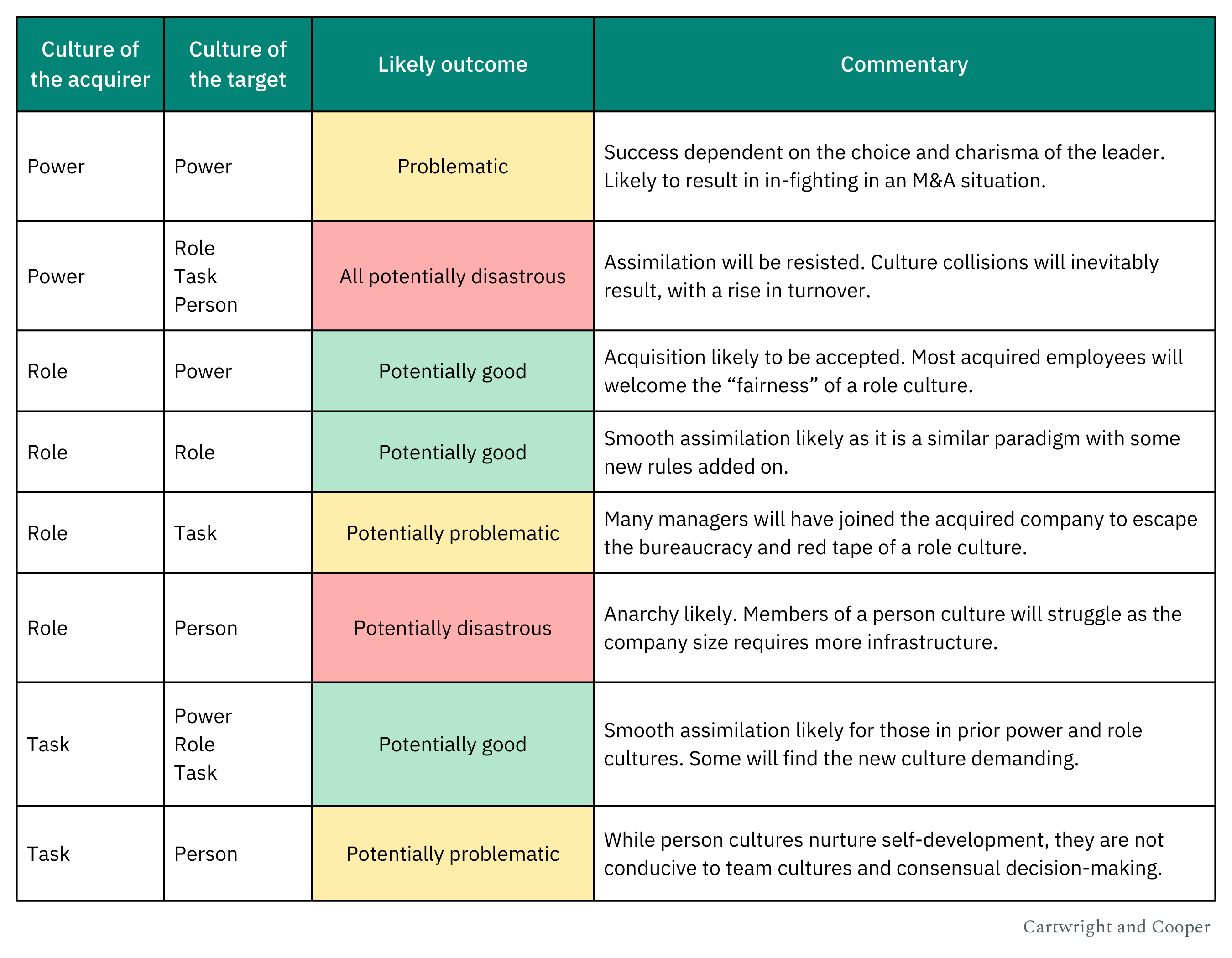

While possessing the capacity to manifest RDF is not always a good thing (See: Neumann, Adam), some of its underlying ingredients may be useful when making successful acquisitions. In 2017, academics from the University of Waterloo and Erasmus University Rotterdam set about assessing the impact of CEO personality on M&A activity. Specifically, researcher Shavin Malhotra and his colleagues studied the effect an extroverted executive had on acquisitiveness. To make this assessment, the authors set about trying to identify “extroversion.” To do so, they used specialized linguistics software to review the earnings calls of 2,381 CEOs over a ten-year period. Extroversion was determined by analyzing things like word count, word repetition, concreteness, visual language, and references to family and friends. This was subsequently compared to each firm’s M&A activity over the same period. As it turned out, extroverted CEOs acted distinctly to their less gregarious colleagues. Not only did they engage in more frequent M&A activity, they also tended to make larger acquisitions. An increase in CEO extroversion from one standard deviation below the mean to one standard deviation above the mean increases the odds of making an acquisition by 11.2%, increases the frequency of acquisitions by 13%, and increases the size of targets by 6.7%. While these statistics might suggest extroverted CEOs simply have low-impulse control, the study also indicated that more outgoing executives are more successful buyers. Namely, Malhotra et al. found a positive correlation between a CEO’s “extroversion score” and the short-term movement of the acquiring company’s stock price. (The latter is often referred to as the “cumulative abnormal return” or CAR.) More concretely, a one-standard-deviation bump in extroversion increases the abnormal stock returns upon acquisition announcements by 0.2%. Though that might not sound like much, it translated into an average gain of $14.7 million for companies in their sample. Such results beg the question: what makes extroverted CEOs better dealmakers? Is it simply a case of a reality distortion field at work? That may be part of the equation; charisma on earnings calls can certainly assist stock price performance. However, it’s not the only factor at play. Extroverted CEOs also benefit from broader social networks. For example, they are more likely to serve on the boards of other companies, giving them greater insight into adjacent industries and potential acquisition targets. Verdict: Have an extroverted CEO with a powerful public-speaking presence and a strategic smattering of board seats in other companies. 2. Congruent culturesTen days into the new millennium, two media giants announced their merger. On January 10, 2000, AOL and Time Warner joined forces to create a new $350 billion behemoth. Within months, it was already being referred to as “the worst merger in history.” While technological shifts contributed to the ill-fated marriage of AOL-Time Warner, the firm’s differing cultures may have been even more damaging. Richard Parsons described his struggles annealing the disparate entities. “It was beyond certainly my abilities to figure out how to blend the old media and the new media culture,” the Time Warner President remarked. “They were like different species, and in fact, they were species that were inherently at war.” While AOL-Time Warner may be the canonical example of a culture clash, it's far from the only one. In their paper, “The Role of Culture Compatibility in Successful Organizational Marriage,” researchers Susan Cartwright and Cary Cooper assessed the importance of cultural fit in brokering an acquisition. To make their analysis, the authors interviewed employees at both acquired and acquiring companies over a three-year period. They gathered data via surveys. In particular, Cartwright and Cooper (a duo that sounds like they should be headlining a procedural drama on TNT) used these methods to capture measurements of organizational commitment, job satisfaction, employee stress, and mental well-being. They also examined behavioral indicators like employee turnover, sickness, and absentee data. Taken together, these findings revealed the cultural style of different organizations and their effectiveness at integrating with another firm. Before turning to Cartwright and Cooper’s findings, it’s worth discussing the point of cultural styles. They are critical to understanding the study’s results. They also happen to be fascinating. The authors divided companies into four cultural categories, borrowing terminology coined by Roger Harrison, an expert in organizational development.

With our categories set, let’s turn to the results. What did Cartwright and Cooper discover? As you might expect, our crime-fighting duo discovered that culture mattered a great deal in the success of a merger or acquisition. While every marriage is unique, Cartwright and Cooper argue that some cultural combinations are likelier to work out than others. For example, a buyer with an Apollo or “role-based” culture may have success integrating an acquisition operating under a Zeus or “power-based” culture. While incoming employees may experience a culture shock, they will likely appreciate the perceived “fairness” of their new home. The reverse composition has a much bleaker outlook – when a “power-based” culture takes over a “role-based” business (or indeed, any of the other categories), the results are “potentially disastrous,” according to the authors. Incoming employees may react poorly to their new strictures, resulting in increased turnover and “culture collisions.” The cost of these collisions can be extremely high, reducing the performance of the acquired company by 25-30%.

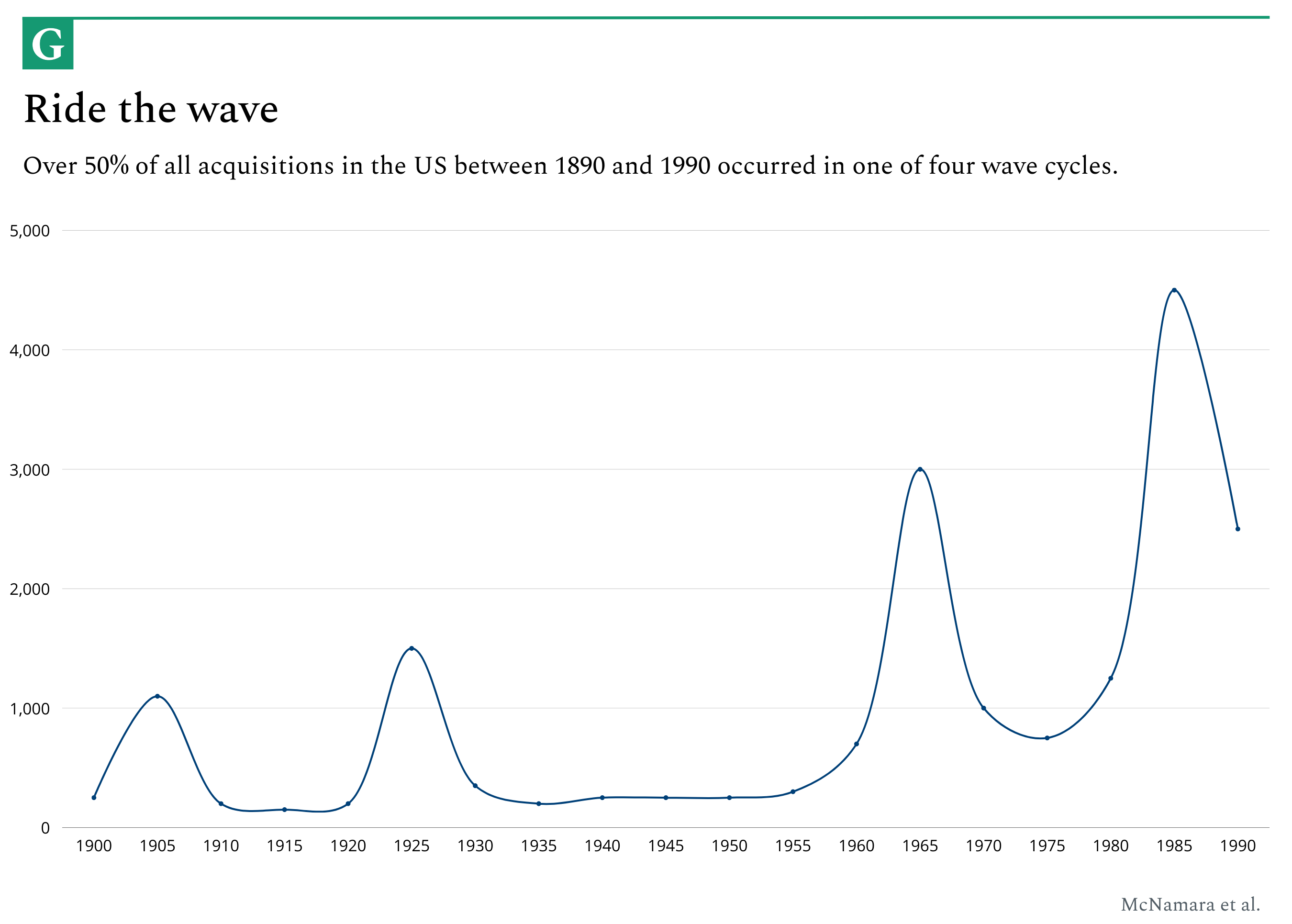

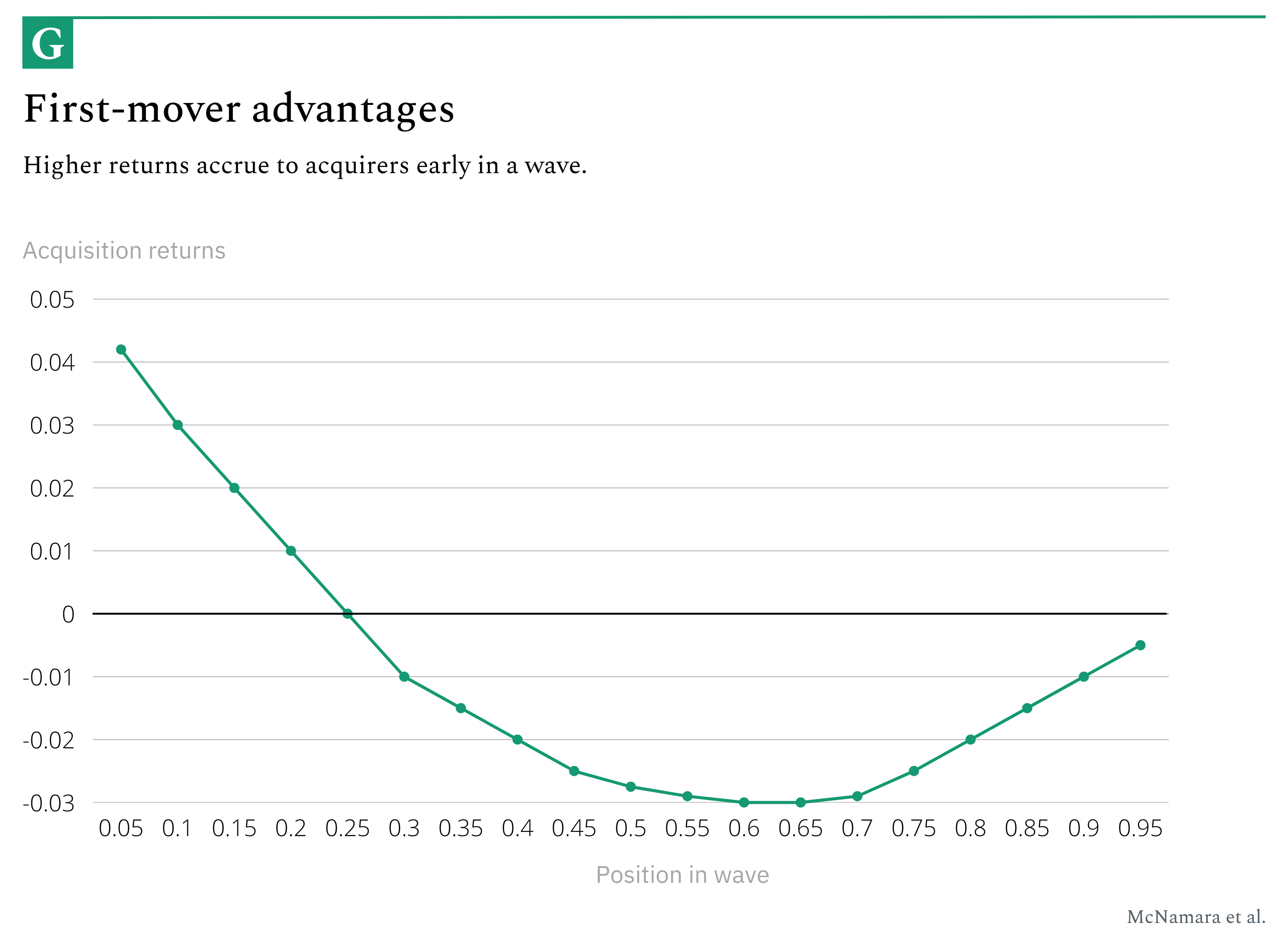

Verdict: A task-based culture of the acquirer – in which there’s an emphasis on team commitment and a belief in the mission, where tasks are assigned based on its requirements rather than politicking or favors – is most likely to result in a smooth acquisition of the acquired company. 3. Moving first“The first mover advantage is a myth,” the organizational psychologist Adam Grant once proclaimed in a TED talk. To back up his position, he drew on data that showed 47% of “first mover” companies failed in their early years compared to just 8% of late-arriving “improvers.” While the Think Again author may have a point when it comes to building a business, it doesn’t apply to the buying process. A 2008 paper published in The Academy of Management Journal outlines this dynamic. Authors Gerry McNamara, Jerayr Haleblian, and Bernadine Johnson Dykes begin by describing the cyclical nature of M&A activity. Between 1890 and 1990, the US witnessed four distinct waves that accounted for 50% of all acquisitions. These periods of frenzy saw thousands of companies snapped up over a matter of years, followed by a steep decline.

By studying 3,194 acquisitions across a twenty-year period, the researchers noted an intriguing relationship: acquirers that moved early in a market cycle found greater success than firms that jumped on the M&A bandwagon later. As shown in the chart below, companies that move in the first 5% of a new wave see positive abnormal returns of 4.2%. By contrast, those who make an acquisition at the height of a wave (roughly 65% through) see an abnormal return of -3%. As a wave heads towards its culmination, returns gradually improve, charting a U-shaped curve.

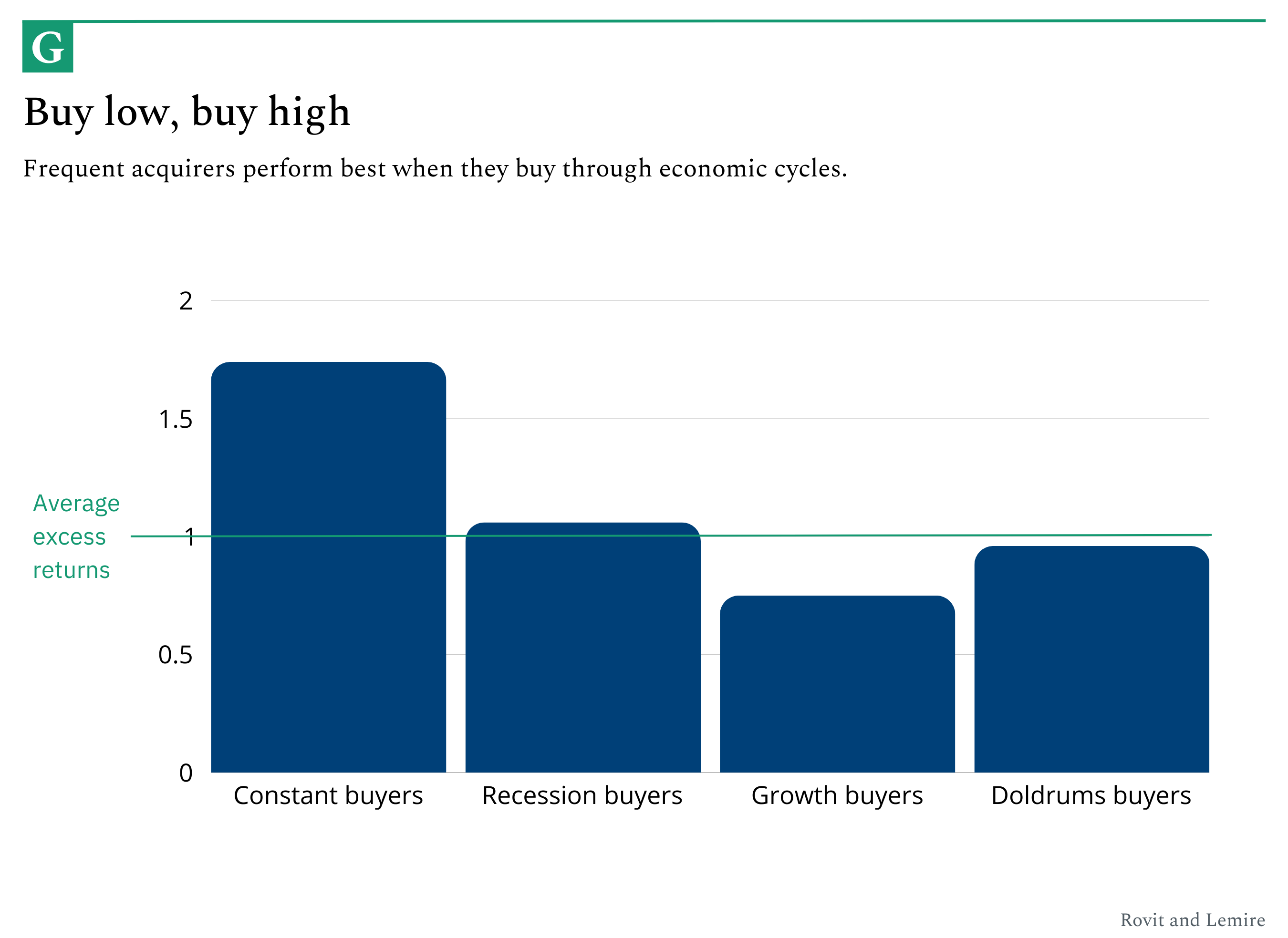

What explains this pattern? Why do first-movers see positive returns, but those in the middle of the pack don’t? A few dynamics are at play. For one thing, first movers may be acting on asymmetric information – they know something that the rest of the market doesn’t yet. Because of this, they may be able to secure a deal at a reasonable price compared to those that follow. Additionally, they have their pick of available firms with little to no competition. As more companies begin to partake in M&A, the environment shifts. Now, potential acquirers face significant competition, driving up prices, limiting selection, and forcing fast decision-making. The result is a string of hasty, costly, and ill-conceived marriages that only let up when the market cools. Verdict: If you possess asymmetric information indicative of a technological or market trend, you should move early. If you don’t, hold off – and be careful not to copy a competitor blindly. 4. Practice makes perfectOver their lifetimes, Apple, Amazon, and Facebook have all made more than 100 acquisitions each. Google has made more than 250. Such volume is no accident. The best companies understand that to find game-changing deals, you have to make M&A a habit. Research from Sam Rovit and Catherine Lemire bolsters this position. The duo analyzed 725 American companies with revenues over $500 million. In looking at this sample, the authors focused on the 7,475 acquisitions made between 1986 and 2001 and the excess returns they delivered to shareholders. The authors defined “excess returns” as “the total return to shareholders, including dividends, minus the cost of equity, or the investor’s expected return.” They then set the average excess returns at 1. Rovit and Lemire split the frequent buyers into four groups:

As it happened, “constant buyers” proved the most successful by some distance. Not only did they outperform “doldrums buyers” by 1.8x, they surpassed “growth buyers” by 2.3x. “Recession buyers” had the second-best results, outperforming their growth-focused counterparts by 1.4x. The authors subsequently honed in on what they termed “frequent buyers” – companies from any of the four categories that had completed more than 20 deals over the fifteen-year period studied. In simple terms, the authors effectively found that the more deals a company made, the more value it could deliver to shareholders. “Frequent buyers” delivered 2x excess returns compared to “nonbuyers” – companies that made no purchases during that stint.

Are Rovit and Lemire’s results an invitation to spray and pray? Should every company stampede to their nearest investment banker’s office? Not quite. As it turns out, the most successful “frequent buyers” tended to follow a set of implicit guidelines:

Verdict: Buying at the right price is an essential factor when reviewing a singular acquisition. Over time, however, if a company is making many acquisitions, a dollar-cost average approach will work better than trying to time the market. 5. True synergyFew words evoke as disgusted a reaction as “synergy.” It is among the most-hated business buzzwords on the planet – a synecdoche for corporate mundanity, fluorescent meeting rooms, and brainless PowerPoint presentations. Yet, in its truest sense (liberated from its cultural baggage), it is the ultimate M&A achievement. How can one achieve it? And what does synergy actually look like? The great Clayton Christensen offers a persuasive depiction. In his paper, “The New M&A Playbook,” the late Harvard theoretician posits that, for a great acquisition, the acquirer needs to look at the critical acquired resources, as well as customer behavior. In a word, synergy. Christensen and his co-authors provide a charming, seasonal example to illustrate the point:

Compare that with a situation where the retailer purchased a similar firm in a different city. In that case, the purchased company would replicate the parent’s cost position in a new geographic area rather than reducing it. There might be some overhead efficiencies, but the acquirer would save less money as the oil retailer would need the acquired company’s trucks to service its new customers. Another temptation would be to try and cross-sell the oil retailer’s customers. They already buy oil from us, so why not sell them something else? Christensen warns that acquisitions whose rationale is to sell a variety of products to new customers will only succeed if customers need to buy those products simultaneously and in the same place. Again, “The New M&A Playbook” elegantly lays out its argument:

Verdict: Consider acquisitions that contain critical acquired resources (trucks in the neighborhood) or true customer behavior (crossover in purchasing patterns.) Ideally, both! PuzzlerRespond to this email for a hint.

Well played to this week’s winners circle: Shashwat N, Wojtek W, Greg K, Frank B, Anmol T, John G, Nathan M, Emerson K, Michael O, Krishna N, Brendan E, and Claire G. All found the answer to our previous puzzler:

The answer? A ruler. Other clever responses include a bed and a mountain. Until next time, Mario __ Investing involves risk and past performance is not indicative of future returns. See important Reg A disclosures and aggregate advisory performance masterworks.com/cd You're currently a free subscriber to The Generalist. For the full experience, upgrade your subscription.

|

Older messages

Letters to a Young Investor with Reid Hoffman

Tuesday, October 31, 2023

The legendary investor shares stories on Airbnb, Stripe, avoiding mistakes, and developing a “theory of the game.”

Become a better investor – one email at a time.

Sunday, October 29, 2023

An investment memo for Generalist+.

Capital: Zavain Dar, GP at Dimension

Thursday, October 26, 2023

Investing at the bleeding edge of technology and life sciences.

Big news: Introducing Generalist+

Thursday, October 19, 2023

Today, we're unveiling our newest premium newsletter designed to make you a better investor.

What do venture capitalists do?

Thursday, October 5, 2023

A study from 1984 outlines the habits of Silicon Valley's capital class. How have they changed?

You Might Also Like

🚀 Ready to scale? Apply now for the TinySeed SaaS Accelerator

Friday, February 14, 2025

What could $120K+ in funding do for your business?

📂 How to find a technical cofounder

Friday, February 14, 2025

If you're a marketer looking to become a founder, this newsletter is for you. Starting a startup alone is hard. Very hard. Even as someone who learned to code, I still believe that the

AI Impact Curves

Friday, February 14, 2025

Tomasz Tunguz Venture Capitalist If you were forwarded this newsletter, and you'd like to receive it in the future, subscribe here. AI Impact Curves What is the impact of AI across different

15 Silicon Valley Startups Raised $302 Million - Week of February 10, 2025

Friday, February 14, 2025

💕 AI's Power Couple 💰 How Stablecoins Could Drive the Dollar 🚚 USPS Halts China Inbound Packages for 12 Hours 💲 No One Knows How to Price AI Tools 💰 Blackrock & G42 on Financing AI

The Rewrite and Hybrid Favoritism 🤫

Friday, February 14, 2025

Dogs, Yay. Humans, Nay͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

🦄 AI product creation marketplace

Friday, February 14, 2025

Arcade is an AI-powered platform and marketplace that lets you design and create custom products, like jewelry.

Crazy week

Friday, February 14, 2025

Crazy week. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

join me: 6 trends shaping the AI landscape in 2025

Friday, February 14, 2025

this is tomorrow Hi there, Isabelle here, Senior Editor & Analyst at CB Insights. Tomorrow, I'll be breaking down the biggest shifts in AI – from the M&A surge to the deals fueling the

Six Startups to Watch

Friday, February 14, 2025

AI wrappers, DNA sequencing, fintech super-apps, and more. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

How Will AI-Native Games Work? Well, Now We Know.

Friday, February 14, 2025

A Deep Dive Into Simcluster ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏