Hi y’all —

I’m back from Ohio, where I helped Money launch its brand-new list of the Best Financial Planners (hold for applause). But let me tell you a secret: The whole time I was exploring Columbus, tracking the Fed decision and shaking hands with CFPs, I was actually thinking about credit card fees.

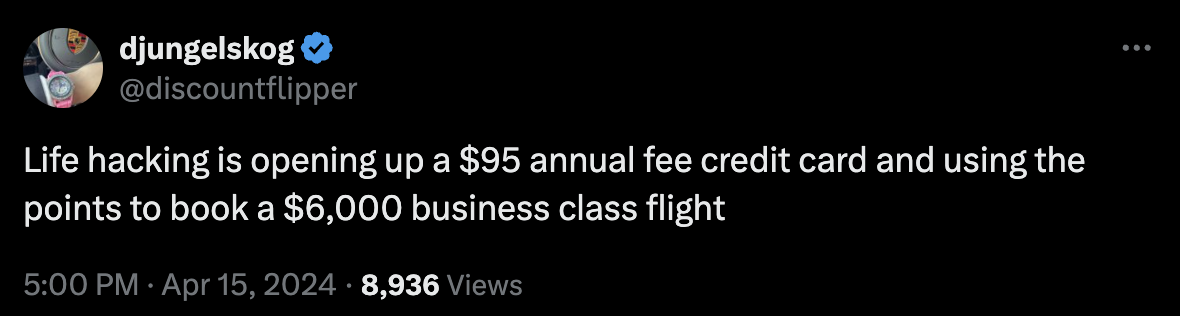

In last week’s issue of Dollar Scholar, I learned that credit card companies make a whole bunch of revenue off me in various ways (largely through interchange fees and interest). Not all credit cards have annual fees, of course, but I’m fixated on the ones that do. It seems ridiculous that I have to pay several hundred dollars just so I can spend my own money.

I’m skeptical that the beloved benefits of a high-annual-fee card can actually be THAT great. I gotta get some answers so I can mentally move on.

How can I tell whether a credit card annual fee is worth it?

Dave Grossman, credit card expert and founder of Your Best Credit Cards, says high annual fees help cover the costs of the exclusive perks I get for being a customer. Depending on what those perks are, he says they can vastly outweigh the fee.

“I pay thousands of dollars in annual fees every year, and I calculated that I come out ahead on every single one of them,” Grossman adds.

Despite inflation, he says, most cards’ annual fees have hovered around $95 for years because $100 is a psychological barrier many issuers don’t want to cross. Some of the most popular entry-level rewards credit cards, including the Chase Sapphire Preferred, Capital One Venture Rewards and American Express Blue Cash Preferred cards, all come with a $95 annual fee.

The next stop on the annual-fee train is $150 — this is what the American Express Green Card costs — followed by luxury rewards cards. Grossman says these fees tend to hover around $450, $550 (Chase Sapphire Reserve) and $695 (American Express Platinum) a year.

Those costs may sound hefty, but I can typically get my money back in three ways: issuer-funded benefits, network-funded benefits and points schemes, says Vrinda Gupta, CEO and co-founder of Sequin, a woman-focused debit card.

Issuer-funded benefits include things like Priority Pass membership, which gives me access to over 1,600 airport lounges with food, drinks, free WiFi and spa treatments. (To enroll in Priority Pass without a travel credit card costs $99 a year plus $35 every time I want to visit a lounge; with a Chase Sapphire Reserve, it’s free.) Another example is Uber Cash, of which American Express Platinum members get $15 a month, plus $20 in December.

Then there are network-funded benefits, which Gupta says are paid for by a credit card network like Visa or Mastercard. These often include rental car insurance or trip protection that can cover me if I have a cancellation, delay or lost baggage.

Sweetening the deal are statement credits, like how the Capital One Venture Rewards card gives customers a credit of up to $120 for Global Entry or TSA PreCheck, and, finally, programs where I rack up points that I can later redeem points for cash back, free flights and comped hotel stays.