Fintech Today - FTT Deep Dive: Payitoff

Hi all, Julie here.

If you Google “student loans,” you get…a lot of content. Most of it goes along the lines of “student loan crisis is about to get worse” or “crippling student loan debt hurting millennials.” It’s safe to say we all recognize that student debt is a huge problem without an end in sight. While Payitoff can’t get rid of it either, it thinks it can do a good job of helping people manage their loans and see a light at the end of the tunnel.

I was extremely fortunate and had parents that worked exceptionally hard to help me pay for college. While it wasn’t a free ride for me, as long as I stayed below a certain financial limit and had a part time job every semester, they agreed to basically pay for my degree from Michigan State. I think a lot of this was that they wanted to make sure I could go to college (neither of them were able to afford it). God bless them (and Go Green!).

|

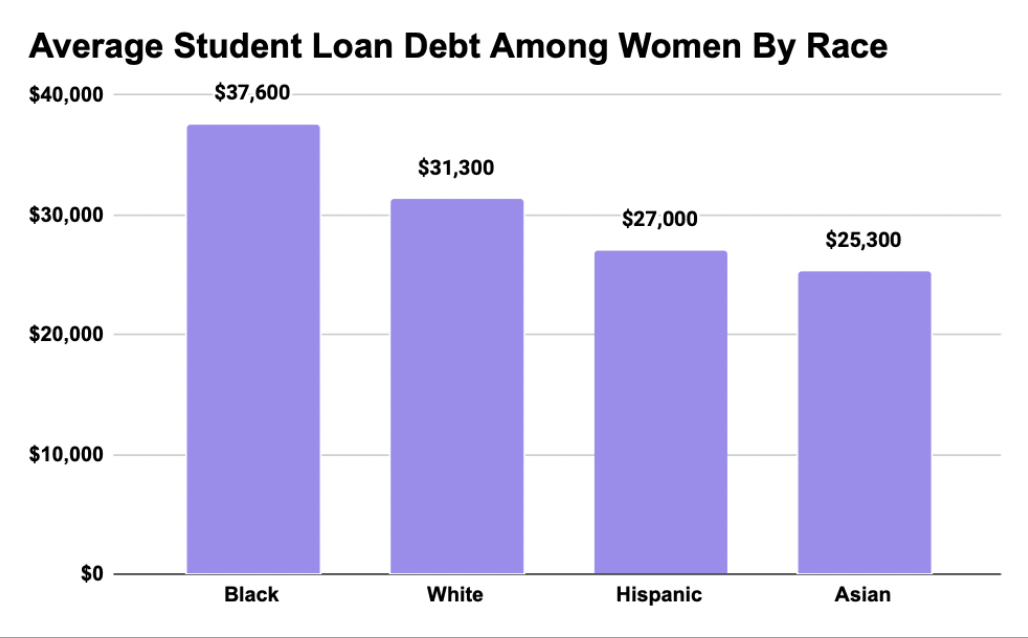

There are many of you reading this newsletter that are wishing you’d been in my situation, and even less likely to have been as lucky if you are a person of color or a female. The stats are depressing to say the least.

- 60% of still-indebted Black student loan borrowers do not have a savings account.

- 66% of Black borrowers report they regret having taken out student loans to fund their education.

- 58% of all student loan debt belongs to women.

- It takes women an average of 2 years longer to pay off their student loans despite making higher payments.

- Student borrowers who identify as LGBTQ+ have an average of $16,000 more in student loan debt than those who do not.

|

This spring, the student loan moratorium ends and many of our colleagues and peers are going to be put in tough situations. While Payitoff doesn’t work directly with customers, it works with companies that then go on to help its customers. Before I go any further, remember that Fintech Today gets paid for these deep dives, but I say no to any that I do not believe are worth my audiences’ valuable time.

Let’s dive in.

Founding Story and Background

The founder, Bobby Matson, went through the student debt nightmare himself. Ironically, he went to a rival school of mine, the University of Michigan. At least we can agree on the Big Ten being the best conference ;)

Anyways, when trying to pay off his loans, he built an algorithm to find his own best course of action. This became the foundation of Payitoff. Some customer examples are Chipper, Origin, Future Fuel.

How It Works

Payitoff helps automate every aspect of the repayment experience. The infrastructure handles everything from syncing loans, to automating guidance and acting on that guidance. This can help enroll in programs digitally, make changes due to life events, find loan assistance and more. Matson says the product has already been exposed to millions of borrowers and that the average borrower saves $240 a month.

Similar to a lot of fintech startups, data plays a huge role in what Payitoff does. The company says that it’s returning roughly 2-3x more data per loan than what’s currently on the market. According to Matson:

“Our loan servicer connections have the best uptime in the industry. That’s always been a priority for us, because we know our partners rely on these connections in order to serve borrowers with the best data-driven recommendations for their student loans. When a borrower connects to their loan servicers, our tools (via our partners) pull significantly more data in order to deliver unmatched comprehensive guidance on a borrower’s full student loan portfolio. It all starts with first having reliable loan servicer connections. Payitoff’s initial core product has always been our loan guidance technology, and we were the first provider to power partner apps specializing in student loans. That perspective taught us to really value collecting the right data, and always deliver results in the best interest of borrowers.”

The company’s tools get borrowers better outcomes for their loan repayments and takes all of the annoying guesswork out of it. Student loans are probably the most confusing of all loans with repayment options, when you actually have to start paying, keeping track of where you took out loans from and more. Talk to anyone who’s gone through the process and I guarantee they’ll complain about the experience.

Not only does Payitoff want to help consumers save money, but it wants to make the process less burdensome (which goes hand in hand with the money saving part). If you take the guesswork out of which loan repayment plan is the right option, you can make sure you’re not paying more than you should be.

Payitoff’s algorithm identifies the programs and payments best for each borrower and then helps them select and enroll in a federal assistance program. When borrowers get approved for assistance programs, they often save money on their total loan overall, as well as earn a lower monthly payment. Other times, they’re able to lower their monthly payment, re-adjust their loan plan to fit their needs, or take other advantageous actions.

Everything from financial situations to changes in government policies to financial planning is taken into account. On top of that, borrowers can then enroll in money-saving federal programs or get assistance online. This makes it easier and much faster than doing things by paper, mail, and/or phone. Not only does this help the borrower, but it helps the companies using it create customer loyalty and satisfaction rates.

Why B2B and Not B2C?

While Payitoff started as B2C, it pivoted rather quickly. The team says that the key reason it sells to businesses rather than directly to consumers is that this is the easiest way for them to ensure that the borrowers are getting what’s best for them. The real issue in the debt ecosystem is that no company or institution had the tools to help borrowers with student loan management in the first place. So businesses have customers (about 43M student loan borrowers) with a real need for student loan guidance, and no way to deliver on that. While it might take longer to sign a business than an individual, each new partnership comes with thousands of new borrowers gaining access to these tools.

Industry Landscape and Competitors

The future of the industry has a lot of moving parts. The biggest is the future of student loan forgiveness. President Biden promised student loan forgiveness during his campaign. Though as many of us know, campaign promises are made to be broken. So let’s make the assumption that student loans are not going away. The change is then happening on what type of payment plans are offered, how companies are helping employees manage their student debt, and how the loans are structured to begin with. For instance, there are some “income share agreements” that universities can offer where investors pay for tuition upfront for a share of the student’s income post-graduation. This moves the risk from the student to the investor, but it has its downsides as well (unregulated debt). There’s also employee benefit programs that are becoming more popular. It’s been fairly common for doctors and other long, expensive degree programs to have some sort of deal with the hospital network they end up going to work for, but other degrees are getting into this as well. Payitoff could play a role in any of these scenarios.

But, so could other fintech companies. Payitoff’s competitors aren’t SoFi, CommonBond and Earnest that fintech nerds like ourselves would first think about when we think of student debt. It’s more like companies like Plaid and Rightfoot that also have APIs that are focused on lowering consumer debt burdens and managing consumer finances.

Rightfoot in particular is the closest example I’ve found. Much like Matson, Rightfoot was founded by someone that struggled with student debt. The company is also a student debt repayment API platform that works with companies rather than directly with consumers. However, there are still some key differences.

- Rightfoot is powered by Plaid, while Payitoff says it has its own unique data stream to servicers.

- Plaid doesn’t yet pull the same amount of data required to deliver the level of comprehensive guidance Payitoff does. Unclear how much effort it would take to change that and if it’s in the roadmap for Plaid.

- As of now, Payitoff is the only API first company that offers digital enrollment features.

Conclusion

Even with competition, it’s pretty safe to say that the student loan problem is big enough for more than one company to have a large impact and be successful. And I for one would love it if all three of these names could make a dent in making the cost of education less of a burden.

Julie VerHage-Greenberg is the co-founder of Fintech Today, where she focuses on editorial content and brand. Prior to joining, she was Bloomberg’s first fintech reporter, covering Robinhood from before it was a billion dollar company, breaking the news that Plaid was acquiring Quovo, and interviewing executives on Bloomberg TV and at several large conferences.

Older messages

FTT Update: The Crypto Heist and A $500 Walmart Gift Card

Wednesday, February 16, 2022

Hi all, Julie here. For those that don't know, Jordan and I recently began trying to start a family. So when Justin Overdorff of Lightspeed posted this fundraiser that's near and dear to

FTT Guest Post: How to De-Risk Lending (pt.2)

Tuesday, February 15, 2022

Hello FTT faithful, I'm Ryan. Long time reader, first second time guest poster. I'm excited to dive into the second half of this guest post and spill the beans on some very achievable

FTT Update: Roses Are Red...

Monday, February 14, 2022

Hi all, Julie here. Hope everyone had a great weekend! Ian got to go to the big game in LA (as did some of my friends at SoFi) and it's safe to say I am INCREDIBLY jealous lol. I was rooting

FTT Update: Affirm Can't Keep A Secret

Friday, February 11, 2022

Hi all, Julie here. Happy Friday everyone! Keeping my intro short today and just gonna recommend that you check out this new Bessemer post on NFT 101 and send it to any friends you have that keep

FTT+: Are We At A Crypto Top?

Thursday, February 10, 2022

Hi all, Julie here. It's almost time for Super Bowl Sunday. I remember back in 2016 when an editor of mine asked me to write about SoFi airing an ad during the big game and whether it was

You Might Also Like

My secret 15-minute video sharing my triple digit options strategy

Friday, February 28, 2025

Free training + book ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

👋 Bye bye, bitcoin

Thursday, February 27, 2025

Bitcoin's biggest one-day blow, Trump's latest tariff threat, and robots playing soccer | Finimize TOGETHER WITH Hi Reader, here's what you need to know for February 28th in 3:12 minutes.

Don't Overlook this Sector Billionaires are Quietly Investing In

Thursday, February 27, 2025

The Billionaires' Energy Secret (You Can Get In) ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Giveaway: Set Sail on Your Next Adventure 🚢

Thursday, February 27, 2025

Enter to win a chance to win a free trip from Virgin Voyages. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

🤖 OpenAI's ex is doing just fine

Thursday, February 27, 2025

Intel looks to be falling apart, a humanoid company 15-timesed its valuation in one year, and what the DeepSeek shakeup actually means | Finimize TOGETHER WITH Hi Reader, here's what you need to

"Impoundment," explained

Thursday, February 27, 2025

Congress's power of the purse vs. presidential power View this email online Planet Money A Constitutional Conflict Over “Impoundment” by Greg Rosalsky A constitutional conflict is brewing over

The New Nuclear Weapon - Issue #510

Thursday, February 27, 2025

FTW: AI is no longer just a tool—it's the new battleground for global power. The Geopolitical AI War is here. Who will push the button? ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The Annoying Path to Privacy Herd Immunity

Thursday, February 27, 2025

Plus! Robots; Competition; Model Moderation; Eggs; Sentiment The Annoying Path to Privacy Herd Immunity By Byrne Hobart • 18 Feb 2025 View in browser View in browser In this issue: The Annoying Path to

Social Security COLA Estimates Tick Higher

Thursday, February 27, 2025

Sticky inflation could give retirees a raise ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Are you 62+ and in need of cash?

Thursday, February 27, 2025

A reverse mortgage may be just the thing ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏