In-depth: NFT lending is on the rise Exploration and prospect of financialization

With CryptoPunks, BAYC and others out of the loop and the exploration of the metaverse on and off the field, more and more users and institutions are running into NFT. Although it is still niche, but there is no doubt that it is in a rapid development of the incremental stage. In the process of development, builder realized that the peer-to-peer trading behavior on the Marketplace severely limited the liquidity of NFT, thus giving rise to the exploration of NFT financialization, of which the representative track is NFT lending. The hard cap on the scale of NFT financialization is the total market capitalization of the NFT market, and the soft cap is the blue chip market capitalization of the NFT market. NFTGO data shows that the current total NFT market cap is $19.38 billion (mainly on the Ethereum chain), and if project market cap is used as a measure of blue chip, then the top 9 NFT projects in terms of market cap account for 34.53% of the entire NFT market cap. If start with recognition, the community-based star projects such as CryptoPunks, BAYC, MAYC, CloneX, Azuki, Doodles, etc., which are more influential in the lending market, also account for 25%-30% of the NFT market cap.

NFT+Fi, initially started from the blue chips. Commonly known as “NFT + IP + DAPP”, the head effect is obvious and high net worth position users are the main service target. For the large base group of users who do not have such strong asset strength, they were naturally rejected at the beginning, but not without opportunities for participation. As the NFT lending model and platform evolves, the governance and voting power of the platform will become more and more important as the platform’s position is able to feed the value of NFT, and the definition of “blue chip” will become broader and broader. Instead of a handful of people deciding on the “blue chip,” the decision could be made by community-based voting. In the future, it is likely to see the community or whales fighting for the governance of NFT lending platform, starting a voting power war similar to “Curve War”, so if you can hold the Token of the quality lending platform in the early stage, it may be an investment Alpha for the base users. Exploration of liquidity in NFT lending Regarding the issue of liquidity, it can be viewed in two ways: first, investors are willing to actively hold a certain NFT for a long time and will not exchange easily; second, investors have to passively hold NFT for a long time due to poor investment decisions. From the perspective of the current market environment, the former are mostly high-quality blue-chip assets, while the latter are mostly likely to be more mediocre underlying. The same holding behavior, but will bring different liquidity expansion path, NFT lending mostly for the former, to help investors release the liquidity of its holdings of high-quality assets and improve the efficiency of capital use; the latter may be fragmented through the fragmentation agreement to attract more participation in the form of Meme-like. NFT lending, is where a borrower goes to lend token by using their NFT as collateral on a platform, with the lender or platform providing liquidity to the borrower. There are currently two dominant NFT lending models: peer-to-peer and peer-to-pool, and unlike DeFi’s prevalent peer-to-peer model, both models can currently have their own audiences. The peer-to-peer model is represented by NFTfi, which mainly involves two main subjects: borrowers and lenders, while the platform only acts as a venue to broker transactions between the two parties. As a borrower, the borrower pledges a suitable NFT to lend wETH or DAI; the lender then provides liquidity to the borrower, using wETH or DAI as a loan in exchange for the borrower’s NFT, which is used as collateral in the transaction. Borrowers list their orders on the platform, and lenders can then determine the loan amount, interest rate, term, and other lending details with borrowers for their value-approved bids. Thus, the lender’s main way of earning is in two ways: first, by steadily obtaining the interest paid by the borrower provided that the borrower repays the loan normally; and second, by obtaining NFT at a substantial discount to the market price in the event that the borrower is unable to repay. The platform’s main revenue comes from the lender’s service fee: the lender is required to pay the platform 5% of the interest earned on a successfully completed loan. In case of loan default, no service fee is charged. In addition, borrowers are not required to pay a service fee to the platform at any time.

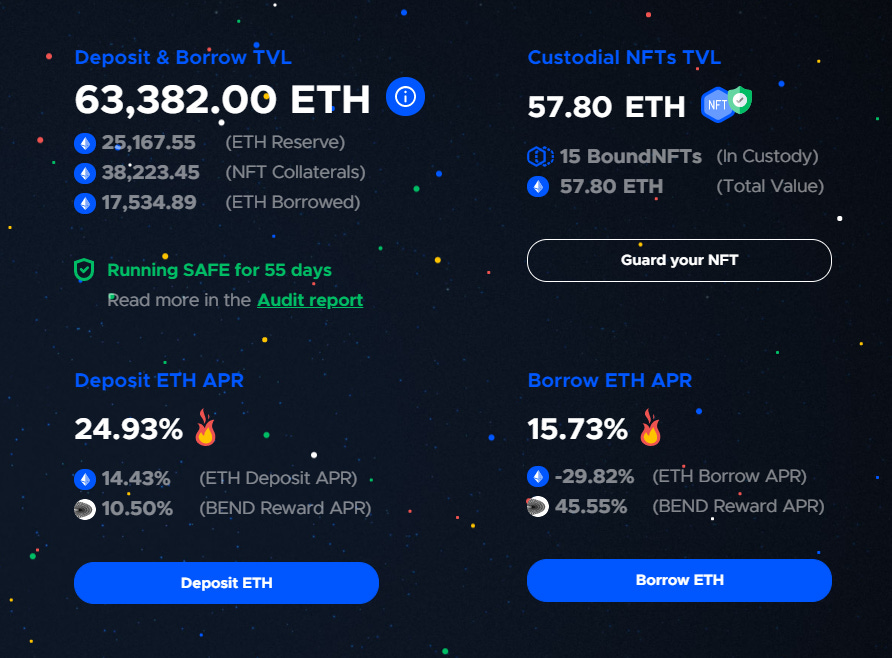

The peer-to-peer pool model is represented by BendDAO, where three main entities exist: the borrower, the platform and the lender. The platform acts as the lending reservoir and the counterparty of borrower and lender. As a borrower, the platform bundles suitable NFTs into a unique NFT: boundNFT as a single unit of collateral (which cannot be used for any interaction), and subsequently lends ETH from the lending pool based on the floor price of the underlying on OpenSea and the collateral ratio specified by the platform; the lender provides liquidity by depositing ETH into the lending pool to earn ETH APR and platform token BEND rewards. The platform’s revenue is mainly derived from the spread between deposits and loans, i.e. the management fee of the lending pool.

When the health factor of the borrower’s NFT-backed loan falls below 1 due to a significant drop in the floor price of the underlying, 48-hour liquidation protection is triggered and the NFT goes to auction simultaneously. If the borrower can repay within the 48-hour liquidation protection period, the NFT backed by the collateral will not face liquidation, but the borrower will still have to pay a default fee (1% of the defaulted debt). In addition, even if the NFT floor price returns to the liquidation-proof price after entering liquidation protection, the borrower must repay a portion of the loan debt and pay a default fee. In addition, building on the BEND, BendDAO mimics Curve’s veToken model by introducing veBEND. veBEND holders receive revenue from the platform and a governance vote on BendDAO to vote on which NFTs can be used as collateral to borrow ETH and provide liquidity on BendDAO. The pros and cons of the NFT lending model: peer-to-peer vs. peer-to-peer pool As representatives of peer-to-peer and peer-to-pool models respectively, NFTfi and BendDAO are used as examples for comparison. In terms of the underlying base, peer-to-peer mode platform as the direct participants of borrowing, and the value of the underlying is mainly derived from the direct collision between the lending and borrowing parties’ perception of the market. Compared to the peer-to-pool model, which is a direct counterparty to both lenders and requires strict control of lending risk, the peer-to-peer model has a more generous list of NFT assets, so the number of supported varieties will be higher, but the trading volume is still mainly concentrated in the head blue chips. In terms of lending amount, under the value of the two agreed and negotiated, the lender in the peer-to-peer model can provide higher liquidity for the borrower, suitable for an NFT series with rare attributes of the subject; the peer-to-pool model is uniform to OpenSea floor price as the premise of lending, can not reflect the different values of the same NFT series subject, more suitable for the sticker floor subject. In terms of repayment, the peer-to-peer model is often agreed upon time and interest, and the borrower will pay the principal and interest and get back the NFT upon maturity, without fear of unexpected events during the period, with a higher risk resistance; the peer-to-pool model is instant repayment, which will be more flexible. In terms of clearing, the platform does not have a clearing function under the peer-to-peer model. If the borrower defaults, the lender will receive the collateral NFT at a discount; in the peer-to-pool model, the platform will auction off the collateral and anyone can participate. BendDAO introduces a 48-hour protection period in the regular auction liquidation, which is equivalent to adding an extra protection for borrowers. The Future Vision of NFT Lending ①Lending demand for head NFT assets replaces trading demand. As head NFT floor prices continue to rise and asset values become more and more prominent, holders are reluctant to give up future appreciation space and sell now. Then its trade volume and liquidity on Marketplace will gradually become thin, on the contrary, the demand for lending trades that release the liquidity of assets will become more and more robust. ② Start a voting rights war on the lending platform. With the majority approval of those first few blue chip NFT holders, if a lending platform can rely on rapid word-of-mouth accumulation in the early stages and gradually grow, and as the lending platform continues to grow and gradually has the ability to feed the value of NFT, then the governance Token representing the platform will become very important. NFT community will be proud of this platform, because it is equivalent to the market recognition, the future has the opportunity to become a new blue chip; on the other hand, there may be a community or whales by holding a large number of platform governance Token to do evil, to vote to amend the rules or strong shelves a NFT project, set off a “Curve War” war in the field of NFT. Follow us If you liked this post from Wu Blockchain, why not share it? © 2022 Colin Wu Unsubscribe

|

Older messages

TSE Sponsored :Global Crypto Mining News (May 16 to May 22)

Monday, May 23, 2022

1. BitFarms announces that it mined 961 Bitcoin in Q1 2022 at an average cost of $8700/Bitcoin and revenues improved to $40 million in Q1 2022, up 42% from $28 million in Q1 2021. Bitfarms presented a

WuBlockchain Weekly:Terra2.0 Summary, FASB, Tether new report and Top10 News

Saturday, May 21, 2022

1、Create a new Terra chain & Regulatory pressure link Do Kwon proposed to create a new Terra chain without the algorithmic stablecoin and distribute the new coins among eco-stakeholders. In

吴说每周精选:新闻Top10与热门文章 Terra2.0专题(0517-0521)

Saturday, May 21, 2022

每周行业十大新闻 1、Terra生态系统复兴计划提案 2.0 进行了修订 目前社区对 Terra 的未来规划是分叉成一条没有算法稳定币的新链,并将新币在生态利益相关者之间进行空投分配。另外,此次暴雷,不管是对于 Do Kwon 本人还是加密货币行业来说,都将引来更多的监管压力。 2、美国财会准则委员会或将加密货币纳入财报标准 2022 年 5 月 15 日,MicroStrategy CEO

Analysis: The Terra Incident Could Trigger a Global Crypto Regulatory Storm

Friday, May 20, 2022

Terra and UST plummeted to zero in an instant, wiping out tens of billions of dollars in market cap, and a large number of investors who suffered losses began to launch lawsuits. Many key industry

Global Crypto Mining News (May 9 to May 15)

Monday, May 16, 2022

1. BTC.com shows that current bitcoin mining difficulty is at a record high of 31.25 T, an upward revision of 4.89%. But as bitcoin falls to $30000, more miners will be nearing shutdown coin prices. 2.

You Might Also Like

Texas doubles down on crypto with new $250 million Bitcoin reserve bill

Tuesday, March 11, 2025

Texas' second crypto bill seeks to enhance state and local government participation in digital asset investments. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

How-ey Can Get Out of Here

Tuesday, March 11, 2025

How On-Chain Data Can Clarify the Regulation of Cryptoassets ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

February CEX Data Report: Significant Decline in Trading Volume Across Major CEXs - Spot Down 21%, Derivatives Dow…

Tuesday, March 11, 2025

In February 2025, the spot trading volume of major CEXs decreased by 21% compared to January. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

El Salvador defies IMF, continues Bitcoin purchases amid market downtrend

Monday, March 10, 2025

El Salvador's Bitcoin holdings grow to $504 million, challenging IMF directives amid sharp price declines. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

🖊️ Trump signed an Executive Order for a US Strategic Bitcoin Reserve; Cronos proposed to reissue 70 billion CRO …

Monday, March 10, 2025

Trump signed an Executive Order for a US Strategic Bitcoin Reserve; Cronos proposed to reissue 70 billion CRO for a Cronos Strategic Reserve; Texas's Senate passed bitcoin reserve bill SB-21 ͏ ͏ ͏

Vitalik TAKO AMA: ETH Positioning, Sequencer Centralization, L1 vs L2, Governance, and Success Metrics

Monday, March 10, 2025

On the evening of February 19th at 12 PM UTC and lasting until 12 PM UTC on February 20th, Vitalik Buterin, the founder of Ethereum, was invited to participate in a flash text interview on Tako (a

Donald Trump Creates U.S. Bitcoin Reserve

Monday, March 10, 2025

March 10th, 2025 Sign Up Your Weekly Update On All Things Crypto TL;DR Donald Trump Creates US Bitcoin Reserve Diddy Shows 'Kindness' To Sam Bankman-Fried Robinhood Conducts $1M Crypto Trivia

Bitcoin’s realized volatility surges in as traders face extreme price swings

Sunday, March 9, 2025

Volatility clustering in Bitcoin reveals the impact of turbulent rallies and sharp pullbacks. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Asia's weekly TOP10 crypto news (Mar 3 to Mar 9)

Sunday, March 9, 2025

Ms. Sun Xueling, Minister of State, Ministry of Home Affairs of Singapore, said that cryptocurrency fraud cases accounted for a quarter of the total loss amount involved in fraud last year. ͏ ͏ ͏ ͏ ͏ ͏

Trump declares end to ‘war on crypto,’ vows to propel America to Bitcoin supremacy

Saturday, March 8, 2025

Trump brands the Biden era as a crypto setback, .President Trump vows to make America the Bitcoin leader, ending Operation Chokepoint 2.0 and bolstering crypto strategies. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏