Not Boring by Packy McCormick - Discounting Belief

Welcome to the 2,449 newly Not Boring people who have joined us since last Monday! If you haven’t subscribed, join 167,924 smart, curious folks by subscribing here: Hi friends 👋, Happy Monday! What a year the past week has been. I’m not going to write a piece on FTX today, other than to touch on it briefly, not because I don’t think it’s an important story, but because it’s been written about millions of times over the past week and I don’t have much new to add. FTX US sponsored Not Boring Founders and a couple of newsletter editions. I would never and will never work with a sponsor whose products I wouldn’t use myself. I just got FTX wrong. I was so comfortable with FTX that when they asked to deposit my payment in my FTX US account instead of my bank account, I said yes without a second thought. I never imagined they’d become insolvent, and traded/kept funds in that account for months without a worry. I only avoided getting wiped out because I got lucky: I wanted to stake the ETH and MATIC I bought there, so I moved everything on-chain a couple of weeks ago. The story is ongoing, but it looks like FTX and SBF committed fraud, deceit, theft, and misuse of customer funds, and I hope that they’re held accountable, and that customer funds can be restored, to the fullest extent possible. Mario Gabriele comes closest to my thoughts and feelings on the whole thing in his beautifully written The Casino and the Genie. I’m working on a bigger piece that in part explains why I think crypto is still valuable and inevitable for next week. Indirectly, though, this piece is about FTX, or the impact of its actions on belief. While it’s hard to measure precisely, belief is one of the most important inputs to tech and crypto valuations, even though it doesn’t show up in a DCF model. Let’s get to it. Discounting Belief

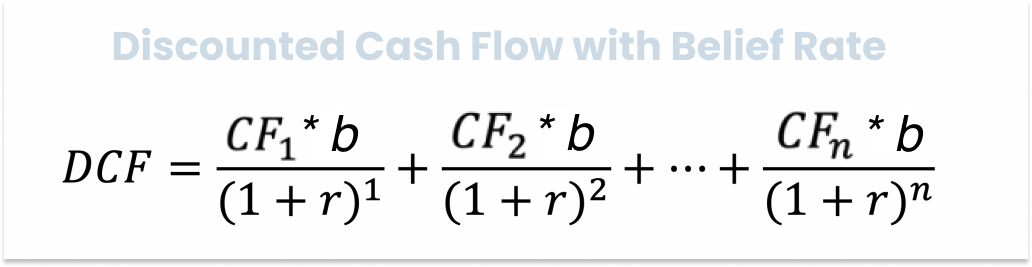

Companies are valued based on the present value of future cash flows. Investors guess how much money companies will generate in the future, and then apply some basic math to figure out what all of that money is worth today. As rates have risen, there’s been a lot of talk about the negative impact of higher interest rates on asset prices. There’s been talk about how higher rates and an impending recession will impact future earnings. There’s been less talk about what the current environment has done to belief, and about the impact of belief on asset prices. Particularly for the more speculative, future-looking companies that we talk about in Not Boring, prices are a function of the discount rate of future cash flows and investors’ belief that those future cash flows will ever materialize. We’ll call that the Belief Rate.

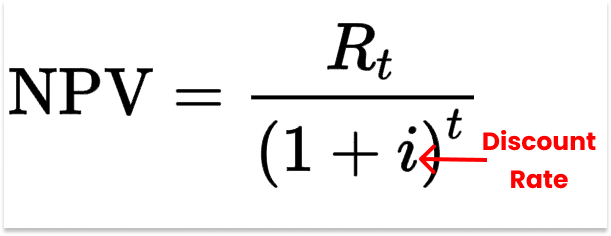

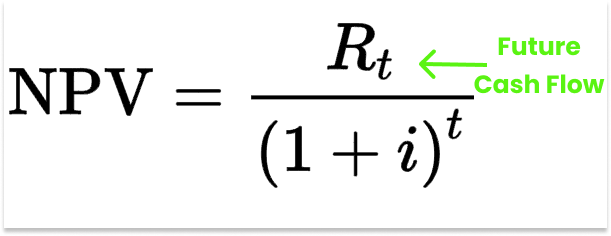

Discount rates and Belief Rates are inversely related: higher interest rates, lower belief in the future. As far as I know, there’s no formula that ties the two, but you can feel it in the sentiment shift ever since the Fed started raising rates. Things that looked promising then look stupid now. Big dreams were as good as gold then; they look like fool’s gold now. The truth is usually somewhere in between. The Belief Rate isn’t a real thing. In spreadsheets, belief manifests in lower cash flow estimates or higher discount rates. But when you separate the discount rate and the Belief Rate, things start to make more sense, and a more clear path emerges for both investors and entrepreneurs. So we’ll address each separately, and then discuss what to do in a low-belief environment. Let’s start with the basics: the discount rate. The Discount RateDespite a brief, CPI-driven respite last week, 2022 has been a brutal year. Growth stocks are down bad, crypto is down bad, and startup valuations are down bad, whether or not that’s reflected in investors’ marks yet. Turns out, a lot of the hope that people felt in 2020 and 2021 about these companies’ future prospects was really just the ultra-low discount rates talking. “Discount rate” is a financial term for the rate that investors expect to receive from an investment, or the company’s cost to borrow money. Practically, it’s used in net present value (NPV) calculations to calculate what a future cash flow is worth today.

The formula says, “Take the expected cash flow in some future year (R) and divide it by 1 + the discount rate raised to however many years in the future it is.” The NPV is essentially compounding in reverse. So if you expect to make a million dollars in ten years, the discount rate helps investors figure out what they’d be willing to buy those million dollars for today. For the first half of this piece, let’s hold that expected future cash flow constant and look at what happens when you change the discount rate. A toy model helps explain its impact.

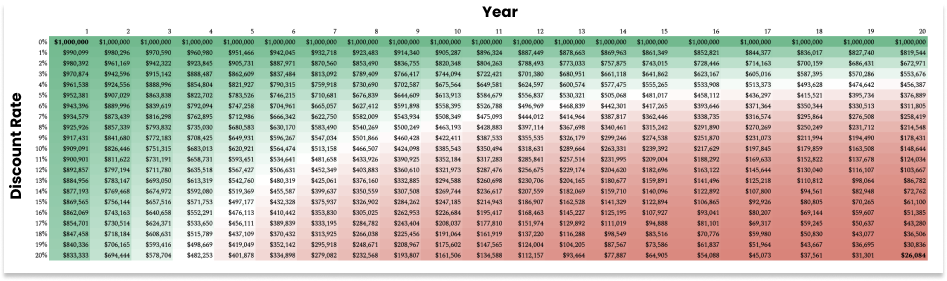

At a 0% discount rate, your $1 million future cash flow is worth exactly as much to you today as it would be ten or twenty years in the future: $1 million. If a company promises, “We’re going to make $1 million dollars in 2042,” you might say, “Cool, I will pay you $1 million right now if you give me that $1 million when you make it in 2042.” To be fair, you don’t have much of a choice. You need to put your money somewhere when keeping it in cash yields 0%. At a 5% discount rate, though, your $1 million future cash flow is worth less today. If it’s ten years in the future, it’s worth $613,913 today. If it’s twenty years in the future, it’s worth $376,889 today. The higher the discount rate goes, and the further out the cash flow, the more measly that cash flow looks today. At 20%, $1 million twenty years from now is worth only $26,084 today. The logic goes something like this: if I can get 20% on a US Treasury Bond, and I invest $26,084 in that US Treasury Bond today, it will be worth $1 million in twenty years. That money is as guaranteed as any money in the world. So I’m not willing to buy your $1 million for any more than $26,084 today when I have a safer way to get $1 million in 2042 for the same amount. Actually, that’s as rosy a scenario for the company as possible. If you can get 20% on US Treasuries, the “risk-free rate,” then the actual discount rate for the company will be higher, because it costs companies more to borrow than it costs the US Government. The difference is called the risk premium. Let’s say that your company’s risk premium is 5% and 10-year US Treasuries are paying 20% (a crazy number, but we came close in the early 1980s). That means that your discount rate is 25%, and your $1 million in 2042 dollars is only worth $11,529 today. Still with me? Why was that important? Companies are theoretically valued based on the sum of their discounted cash flows. If the company expects to generate $1 million in cash flow every year for the next twenty years, then the company is worth $20 million today at a 0% discount rate, or $3,953,883 at a 25% discount rate. The same exact business is worth one-fifth as much today if you change nothing about it except for the discount rate. Those are oversimplified numbers for illustrative purposes. They’re extreme, too. But the extremes help paint a picture of what’s going on in the markets right now. The obvious piece of what’s going on in the markets is that the Fed is aggressively hiking rates. From a low of 0.52% (or 52 bps in finance-speak) in August 2020, the 10 Year US Treasury yield has increased to 4.14%.

That’s only like 3.5%. How much could it hurt valuations?

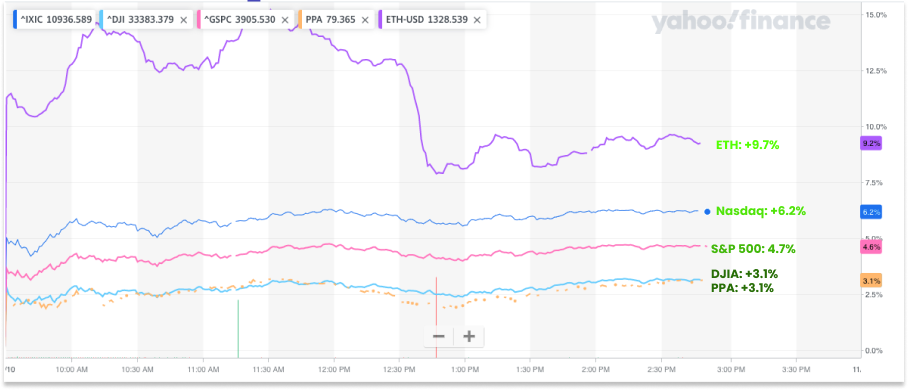

Using the 10 Year UST as the discount rate, $1 million in ten years was worth $949,457 in August 2020 and is only worth $666,537 today, a 30% decline based on nothing changing except the 10 Year UST yield! This is also why stocks and crypto skyrocketed on Thursday when Consumer Price Index (CPI) growth, which measures inflation, came in lower than expected. People expect that lower CPI growth will mean the Fed will stop raising rates as aggressively as inflation comes back to earth. Yields declined, reflecting that expectation, and with them, discount rates. This dynamic hits the types of companies we talk about in Not Boring – fast-growing technology companies, especially newer ones – harder than it hits more boring, predictable, slower-growing businesses. The simplest explanation, based on the formula we’ve been talking about, is when these companies are expected to generate most of their cash flow: in the future. While there are variations on the theme, the typical tech company model is to raise venture capital, invest a ton of money upfront in technology and customer acquisition, get super big, and then, and only then, pull back on fixed costs as a percentage of revenue and reap the benefit of low marginal costs and recurring revenue to generate absurd, high-margin cash flows. That means that they expect small or negative cash flows in the short-term, where higher discount rates have the least impact, and big cash flows in the future, where higher discount rates have the highest impact. Look at the difference between PPA, an ETF that tracks defense stocks, and the NASDAQ Composite Index, which tracks tech stocks, over the past year as rates have risen. PPA is up 2%, Nasdaq is down 33%. A lot (but not all) of this simply has to do with the time distribution of each category’s projected earnings, and the relative impact of rising rates on each.

There’s some noise in there. For example, there’s a war going on, which is presumably good for defense stocks, and tech companies’ corporate and consumer customers are more sensitive to a recession than the DoD is. A more clear picture emerges when you look at the response to Thursday’s CPI print:

The shapes of each index’s charts are nearly identical, but they’re moving on different scales, with the riskiest and growthiest Nasdaq Composite Index increasing twice as much as the more conservative, slower-growing Dow Jones Industrial Average. The discount rate impacts growth stocks more than others, in both directions, because their cash flows are further in the future.

ETH, and crypto more broadly, is even more sensitive to discount rates than the Nasdaq because its future value is so far out and speculative. Startups don’t trade in real-time, but if they did, they’d probably move somewhere in between the Nasdaq and ETH, because their future cash flows are further in the future than the average public tech company but most do have the ability to produce spreadsheets with numbers that can be used to run a traditional valuation model, even if it’s a very uncertain one. Crypto, startups, and tech stocks are also more sensitive to a more fickle input: belief. Everything we’ve talked about so far is just the math part, and far smarter people than me have weighed in on the impact of rising interest rates on valuations with more nuance. This Invest Like the Best episode on macro with Bob Elliott (which I promise I listened to after writing everything above) is a good listen on that front:

The other part of it is hand-wavier, more vibes-based. Let’s call it the Belief Rate. The Belief RateSo far, we’ve held the expected future cash flow constant and played with the discount rate. But holding that expected future cash flow constant is a big assumption, especially for technology and crypto companies whose histories are shorter and whose promised best days are far in the future. For the second half of the piece, we’ll focus on the expected future cash flows.

The Belief Rate is something like a conversion rate between a company’s projections and the future cash flow number that shows up in investors’ models. In practice, companies don’t provide guidance far into the future. It’s up to analysts to take everything the company has done in the past and said about the future and build models that turn all of that into numbers. And those analysts’ cash flow projections come with their own belief on the company’s future prospects baked in. No one is building models that calculate Rt*b, they’re just putting in an Rt for each future cash flow that implicitly accounts for their own belief and analysis. If anything, they’re backing into something similar by adjusting the risk premium reflected in the discount rate. But I think it’s worth breaking out the Belief Rate as a separate thing to understand what happens when belief, in the market, an industry, or a specific asset, changes. (Interestingly, in a 2012 report, McKinsey said that project analysts too often increase the risk premium in their discount rate due to uncertainty about their cash flow projections, and recommends that they should instead keep the discount rate at the actual cost of capital and use a weighted average multiple cash flow projections instead… kind of like an internal Belief Rate.) The Belief Rate is connected to the discount rate – when rates are low, people have to put their cash somewhere, and they want to believe – but it’s also tied to more nebulous general sentiment. That piece is harder to describe, but if you’ve spent time on tech Twitter, crypto Twitter, or fintwit, or just read tech press, over the past couple of years, you’ve felt it. The souring market – plus a war, crypto blowups, politics, and a general hangover from the past few years of excess – precipitated a Vibe Shift. The Vibe Shift hit the Belief Rate hard.

Just as Treasury yields impact every company’s discount rate, the Vibe hits every company’s Belief Rate. In a bear market, belief in everything suffers. And just as the discount rates hit companies with a higher percentage of their cash flows further in the future harder, the Belief Rate hits companies making bigger, more speculative future-looking bets harder, too. For the past few years, while rates were low and growth was king, the Belief Rate for bold tech companies was close to 100%. If a company said they were going to build AI-Operated Space Zoos and planned to generate $100 million of cash flow by 2028, investors responded, “Only $100 million? Y’know, a lot of people undershot Uber’s TAM. Let’s say $200 million, and here’s $50 million to help you get there faster.”

Everyone, me included, was a little drunk on a cocktail of cheap money and easy demand. Rising interest rates and a (looming?) recession closed the open bar. Investors are sobering up. And when they look at that “$1 million of cash flows in ten years” projection, all of a sudden, they’re going:

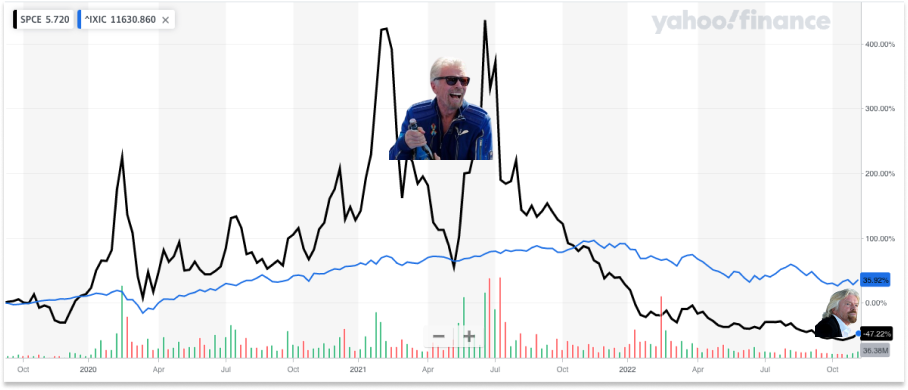

The degree to which investors don’t believe you depends on a bunch of things, like how good a job you’ve done doing what you said you were going to do, how crazy the assumptions baked into your projections are, and how far in the future your projected cash flow is. If Lockheed Martin says they’re going to generate $6.5 billion in Free Cash Flow next year, you can take that to the bank (plus or minus a few percentage points). The Belief Rate is like 98%. If my AI-Operated Space Zoo company, which currently operates zero space zoos, promises to generate $100 million in free cash flow by 2028, investors will apply a very skeptical Belief Rate, somewhere in the 0.5% range. That, plus the higher discount rate, will give my AI-Operated Space Zoo company so low a valuation that it will be hard for me to find investors willing to pay anything close to what I think the company’s worth based on conversations I had in 2021. That seems like an extreme example, and it is. My Space Zoo might have a hard time getting funded in any market. But Virgin Galactic, which offers 90 minute flights to space for $450,000, went public via a SPAC with Chamath in 2019, and its chart illustrates the point.

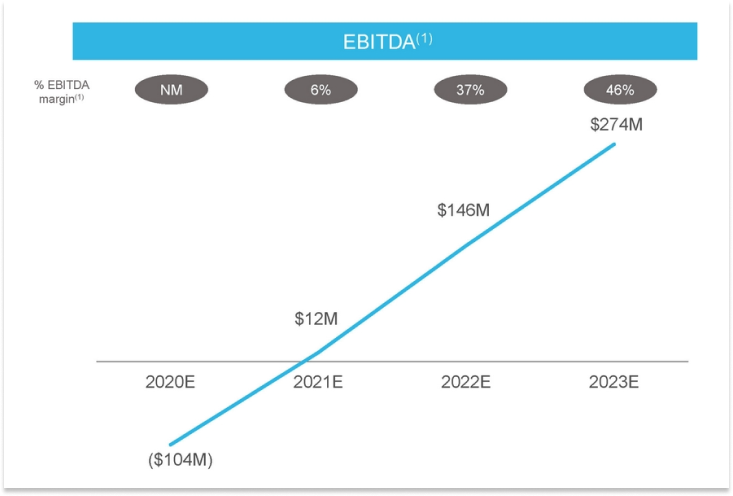

Virgin Galactic (SPCE) strongly outperformed the Nasdaq Composite for most of its life as a public company, spiking up more than 400% in the summer of 2021 in the middle of SPAC-mania, but right around the time that the Nasdaq peaked, it dipped lower and has dramatically underperformed against the index since. From September 2019 to now, the Nasdaq is up 36% while SPCE is down 47%. Part of this underperformance can be explained by the discount rate. Virgin Galactic is losing a lot of money today (-$235 million in free cash flow in 2021), and presumably the bulk of its cash flow, if it comes, will come far in the future (when it gets to eating that $900 billion commercial aviation market). Its SPAC presentation projected $274 million in EBITDA by 2023, with an EBITDA line going practically straight up, leaving the investor to imagine what that number might look like by 2033. Discounting that far out EBITDA by 5% leads to a much different present value than discounting it by 10%.

Running super super rough back of the envelope math – growing that $274 million in EBITDA out ten years at the same 87% growth rate from 2022 to 2023 and applying a 5% discount rate – gets you a $16.4 billion net present value, not far from SPCE’s peak market cap of $15.7 billion. Upping that discount rate to 10% takes the NPV down to $10.9 billion, a big drop but nowhere near the $1.5 billion market cap the company sports today. You’d have to apply a 39% discount rate to get you to $1.5 billion, and rates haven’t gone up that much. Something else is happening. Quite clearly, investors are no longer giving Virgin Galactic the benefit of doubt that it will be able to generate $11.9 billion of EBITDA in 2030. They’re applying a much lower Belief Rate. If you go with my made up numbers and sloppy toy model (the one with 87% EBITDA growth), if investors were applying a 5% discount rate and 96% belief rate to get to the $15.7 billion valuation in summer 2021, they’re applying a 10% discount rate and a 14% belief rate to get to a $1.5 billion valuation today. One quick thing to point out here: some of the belief is direct, and some of it is reflexive. That is, while I can make the numbers tell a certain story, the reality is that in the case of SPCE, and risk assets more generally, a lot of the price action is based on a belief about what other people will believe. I would wager that many SPCE investors weren’t running DCFs and coming up with a fair value for the stock. They were betting that other people would be willing to pay more than they were. When easy money and belief exit the market, that reflexive belief unwinds quickly. Caveating once again that these numbers are all made up, that I’m not running a full DCF model, and that I’m using a Belief Rate on old numbers as a catch-all for belief, adjusted projections, and a very real hit to the number of customers willing to pay $450k to fly to space in this economy, I think it’s a useful way to look at what’s happening. Future luxury space travel is a near-perfect vessel for belief – there’s not much else to go on at this point – and when people’s belief falters in a bad market, it’s retrospectively very obvious that future luxury space travel was going to be hit a lot harder than the broader market. I say “near-perfect,” because there is a perfect vessel for belief: crypto. While there’s a growing body of work on how to value various types of tokens, crypto’s valuation methodologies aren’t as standardized and broadly accepted as equities’. If you asked ten people how to value bitcoin, for example, you’d get answers ranging from something about “the cost of energy required to mine a block” to “the market cap of gold” to some log-scale rainbow chart to “lol” to a straight up admission that the price depends on how many other people believe in it given its limited supply. Governance tokens? Something something ability to direct the use of funds in the treasury something something. ETH is more clear, but still less clear than equities: because it generates fees which go to people who’ve staked tokens, you can model out something like cash flows. That said, given the decentralized nature of the ecosystem being built on top, competition from other chains, and the potential impact of L2s on volume, anyone who tells you they have a precise expectation of cash flows is full of shit. The more uncertainty there is around cash flows and valuation methodologies, the more sensitive an asset should be to changes in the macro Belief Rate. That, I think, is the main reason crypto prices jumped so high during the 2020-2021 bull run and why they’ve tanked so hard in this bear market. But the micro Belief Rate – the Belief Rate tied to a particular category or asset – can decouple from the macro Belief Rate given good reason. The past week provided as clear an example of that as possible. Earlier, we saw that the price of ETH jumped more on the CPI print than the Nasdaq did, largely based on sensitivity to the discount rate. But if you zoom out five days, ETH dramatically underperformed the Nasdaq last week.

We all know what happened. FTX was one of the largest and most trusted names in crypto… until it wasn’t. When other centralized financial (CeFi) institutions crumbled in the spring, there was FTX to bail them out. The company was worth $32 billion, and backed by many of the best venture capitalists. SBF was on the cover of magazines. The Miami Heat played in FTX Arena, and Lewis Hamilton rocked the FTX logo on his Mercedes. While some people were vocally wary of the relationship between Alameda and FTX, I didn’t encounter anyone who thought that FTX could actually fail. And then it did. FTX’s downfall tanked belief in crypto more than any event I’ve experienced. While ETH wasn’t directly impacted – meaning, ETH didn’t lose funds in the bankruptcy or something – the chart above shows the impact of damaged belief in real-time. The price of ETH can roughly be viewed as a bet on the future growth of web3, and the chart shows that the FTX crash led investors to apply a lower Belief Rate to the whole ecosystem. While the Nasdaq was up over 6% on the week, ETH fell more than 19%. The majority of that 25% delta can be explained by the lower Belief Rate. That’s an extreme example that highlights the point, but there are less extreme examples everywhere you look in tech. One of the most obvious is Meta’s bet on the Metaverse. The Company Formerly Known as Facebook announced its rebrand and Metaverse plans at a keynote on October 28, 2021, just three weeks before the Nasdaq peaked. Three months later, in February, it announced that Facebook lost daily users for the first time. After trading roughly in line with, if below, the Nasdaq Composite over the past five years, Meta’s stock tanked and decoupled from the index with that news.

While the company has other issues – bloat, Apple kneecapping its ad business, TikTok, slowing user growth – spending ~$10 billion per year on VR and AR in an attempt to own the next platform is clearly something that plays better in a low rate, high belief environment. I don’t think we’d be seeing letters like the one that Altimeter’s Brad Gerstner sent Zuck – Time to Get Fit – in mid-2021. Loss of belief compounds – there’s less macro belief, then you add on challenges in the core business, and by the time you add something so speculative and capital intensive to the mix, investors are looking for reasons to not believe. I think that a big part of Meta’s underperformance can be explained by investors applying a much lower Belief Rate to the company’s Metaverse play than Zuck would have expected when he planned it during the bull market. Whether he’s lucratively right or very expensively wrong remains to be seen many years in the future, but if you think he’s right, you’re getting a pretty steep Belief Discount right now. A related example is Snap, a company whose whole history can be viewed as a series of crises of belief. In June 2020, in the midst of a post-COVID-crash belief rebound (and lower rate environment), I wrote a piece titled Oh Snap! laying out my view that Snap was building the most compelling Augmented Reality (AR) platform out there. Combined with the strong growth and engagement of young American users and an improving ads business, I thought that Snap was undervalued. For a while, I looked smart.

Snap was the perfect stock for a low-rate, high-belief environment. Its expected cash flows are further out in the future than the average Nasdaq stock, it was a comeback story, brand marketers were feeling spendy (in part because they could spend brand marketing dollars today for cash flows far in the future), and it had a big, audacious AR bet for people to believe in. At one point, right before the Nasdaq peaked, it was up over 400% from the beginning of 2020. Then, it crashed. It missed revenue estimates in its October 2021 earnings thanks to Apple’s privacy changes and fell 22% the next day. It’s been pretty much down-only since then. A few weeks ago, it crashed 25% when it missed earnings again. Like Meta, there are many factors – Apple, decimated brand marketing spend, and rising rates chief among them – but like Meta, I think that a big factor is Belief Rate compression. “Cool AR thing you have there in 2030,” investors seem to be saying, “We believe that will have a material impact on the business like 1%.” If you have a differentiated belief there, you can pick up SNAP at 2019 prices. If you have a differentiated belief to the downside on its core business, of course, you can try to short it back to 2018 levels. I hadn’t put it into words until writing this piece, but I think my biggest lesson from investing – public, private, and crypto – over the past couple of years is to be more aware of the Belief Rate that I, and especially others, are applying to companies. I’m great at buying when I sense that my Belief Rate is higher than others’, but not so good at selling when everyone’s Belief Rates are as high as, or higher than, mine. You need to do both to make money. Now, we’re clearly in a low-belief environment. ETH, Meta, and Snap are just three examples of the many I could choose from the smorgasbord. So what’s a company to do in a high-discount rate, low-belief rate environment? What to Do When Belief Dries UpWriting all of this out has given me a new perspective on all of the cost cutting measures and pivots to profitability in the tech and startup ecosystem. On the surface, they look like survival tactics – keep burn low so you don’t run out of money while funding is harder to come by, get to profitability so you control your own destiny – and they are, but they’re more than that. They’re the rational moves. In this environment, cash flows next year are worth a lot more relative to cash flows in ten years than they were just a year ago. Cutting costs and making moves to get profitable sooner, even at the expense of long-term cash flows, makes sense. I said earlier that everyone was drunk on low rates last year, but hiring more people to work on moonshot projects that might pay off in five years may have actually made sober sense when the Belief Rate was higher and the discount rate was lower. Now that the Belief Rate is lower, focusing on shorter-term wins that don’t require much investor belief can make sense. Some of the biggest, most impactful ideas just won’t be able to get profitable in the near future. There’s new tech to develop, supply chains to set up, and long sales cycles to contend with. If you still have the urge to go big, and I hope that many of you do, you need to provide as much concrete evidence that you’re making progress towards your huge, crazy vision as possible. Hit milestones, be explicit about every step of the plan, hire brilliantly, be hawkish about unit economics. Make investors apply a higher Belief Rate to your company than they’re applying to the market through your actions. But for the average company, the one with a product in market and customers paying, it’s rational to tighten your belt in this environment, dilute yourself as little as possible, bank belief, and preserve optionality in order to accelerate when discount rates come back down and Belief Rates shoot up again. That said, there are pockets in which the Belief Rate is still high. Generative AI is the obvious example here. In October, Stability AI, the company behind Stable Diffusion, raised a round at a $1 billion valuation. The same week, AI content platform Jasper announced a $125 million Series A at a $1.5 billion valuation. Presumably, most of Stability and Jaspers’ cash flow will come very far in the future, but investors were willing to apply a high Belief Rate to each. Why? I’m not exactly sure, but my best guess is that there are a couple of factors. First, this generative AI boom was born in the bear market and wasn’t tainted by overhype in the bull market. It’s shiny and new when so much looks beaten down. Second, as belief in incumbents tumbles, it looks like there’s a real opportunity (and appetite) for a new paradigm, and a consensus forming that the next Google and Facebook will be built AI-native. Third, the size of the opportunity is so large that it’s possible to arrive at a billion-dollar valuation even with a lower Belief Rate; it’s easy to imagine these valuations would have been even higher in mid-2021. Fourth, the technology is mind-blowingly cool, and it makes people want to believe. And finally, even in a bear market, people want to believe in something. More broadly, while venture funding has cooled significantly, and prices for deals that do get done have come down, this isn’t the end of tech. Massive companies will very likely be built during this bear market. With layoffs and hiring freezes at big tech companies, startups will have the chance to build all-star teams at affordable prices. Huge categories are being transformed. Cost curves are coming down. Founders are still dreaming big. And some companies still deserve a high Belief Rate. Some companies will do exactly what they say they’re going to do. Some companies will even exceed their own optimistic projections. In 2020 and 2021, high Belief Rates were applied uniformly to anything in tech with a little growth, and anything that touched web3. In a market like that, it was rational for founders to paint the grandest picture they could for investors, knowing that investors would give them credit for most of it. That meant a lot of companies got funded at prices that look silly today, and it means that most companies that got funded then are overvalued. In this market, prices have come down uniformly due to a combination of higher discount rates and lower Belief Rates across the board. That should mean opportunity for those who can find mispricings in belief. Some companies that get funded today will be deeply undervalued. That said: beware. If this bear market has re-taught us anything, it’s that the macro trumps everything. That’s true for the discount rate, and it’s true for the Belief Rate. Even if you believe in a particular company, the macro Belief Rate can keep it down longer than you can stay solvent. Just like SPACs, startup investing requires more than your own belief; it requires an educated assessment of the beliefs of the funds who will need to lead a company’s next round. I have no differentiated view on the macro, and if I did, you shouldn’t trust it. People have spent their whole careers thinking about macro and still get it wrong, and I have not spent my whole career thinking about macro. I have no idea what the discount rate will be in a week, a year, or a decade. If interest rates continue to rise, higher discount rates will continue to create a drag on valuations across the board, and especially on growth assets. But there will be opportunities in the micro, in companies that you believe in more than anyone else does, in ideas that seem crazy to pursue when everyone is focusing on the short-term. Legends will be made in this downturn. Some of them will be the ones who take the practical advice from a few paragraphs ago, cut costs, get profitable, survive, and come out swinging in the next bull market. Others will be those who, despite what’s rational, continue to think and act long-term, even when long-term trades at a discount. Whether in a year or a decade, valuations will rise, big companies will be created, and belief will be restored. For whenever that happens, note to self: Don’t Stop Believing is a better song than it is a trading strategy. Thanks to Dan and Puja for editing! That’s all for today. We’ll see you on Friday for the Weekly Dose of Optimism, and next Monday for an essay I’m very excited about (if I can wrangle it into form). Thanks for reading, Packy © 2022 Packy McCormick

|

Older messages

Weekly Dose of Optimism #20

Friday, November 11, 2022

UN Poverty Report, Abundance Recommendations, Blended Meat, Binge Eating, and Thought-to-Speech Interfaces, Anton Teaches Packy AI

Atoms Are Local

Monday, November 7, 2022

Elliot on the biologization of industry, PLUS Anton Teaches Packy AI

Weekly Dose of Optimism #19

Friday, November 4, 2022

Meta's Protein, It's Time to Space, Nuclear Brief, RSV Vaccine, Stripe Layoffs, AI Portraits

Capital & Taste

Monday, October 31, 2022

Meet the Company Formerly Known as Party Round

Weekly Dose of Optimism #18

Friday, October 28, 2022

The Crypto Story, IEA Calling Top, Data Lasers, Schumpeter's Workout Plan, ML-Powered Drug Discovery, Bleeding Edge AI

You Might Also Like

Discover a preview of the content keeping Digiday+ members ahead

Thursday, February 27, 2025

Digiday+ members have more ways than ever to stay ahead of the news and trends transforming media and marketing. Explore premium content from our editors below, including weekly briefings, research and

See you in Boston?

Thursday, February 27, 2025

...back in person for the first time since 2019! Exploding Topics Logo Presented by: Semrush Logo You follow Exploding Topics because you want to get an edge on your competition. Now take that

Why I'm doubling down on my community in 2025... (free bonus)

Thursday, February 27, 2025

Hi there 2025 is chugging along (it's almost March!) – and there's a ton going on right now. But there's something that hasn't changed. Your agency still needs a constant stream of new

Programmer Weekly - Issue 243

Thursday, February 27, 2025

February 27, 2025 | Read Online Programmer Weekly (Issue 243 February 27 2025) Welcome to issue 243 of Programmer Weekly. Let's get straight to the links this week. Streamline IT management with

🎙️ New Episode of The Dime China Tariffs & The Next Era of Vapes: Impact on Supply Chains & Brands ft. Nick Kovacevich

Thursday, February 27, 2025

Want to be featured on The Dime Podcast? Scroll to the end of this email to find out how. Listen here 🎙️ China Tariffs & The Next Era of Vapes: Impact on Supply Chains & Brands ft. Nick

80% less time on social reporting sound good?

Thursday, February 27, 2025

Get Forrester's Total Economic Impact™ of Sprout. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Social proof in email marketing, National Toast Day, and the art of CTAs

Thursday, February 27, 2025

The latest email resources from the Litmus blog and a few of our favorite things from around the web last week. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Python Weekly - Issue 688

Thursday, February 27, 2025

February 27, 2025 | Read Online Python Weekly (Issue 688 February 27 2025) Welcome to issue 688 of Python Weekly. We have a packed issue this week. Enjoy it! The #1 AI Meeting Assistant Summarize 1-

Free download: 5 ways to improve your proposals

Thursday, February 27, 2025

A free resource for you ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

From living in a car to $1.4M in 5 months

Thursday, February 27, 2025

I love that you're part of my network. Let's make 2025 epic!! I appreciate you :) Today's hack From living in a car to $1.4M in 5 months Taro Fukuyama and 2 of his friends from Tokyo