In this issue:

To Understand Jio, You Need To Understand Reliance

Earnings

Amazon Sees For the State

Gerontocracy

M&A in Kids YouTube

Monopolists Still Compete

China, Infrastructure, and Risk-On

Fintech is all about CAC, Part #1281241

Dollar Shortages, At Home And Abroad

Second Acts

To Understand Jio, You Need To Understand Reliance

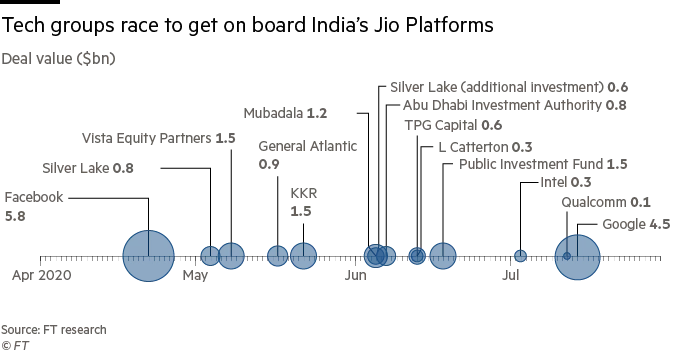

In late April, Facebook made an unusual announcement: they were investing $5.7bn in Reliance’s Jio Platforms subsidiary, an Indian telecom company with 398m subscribers. This started an awe-inspiring streak of investments:

|

(Via FT)

And that’s not all: Amazon.com is in talks to make an investment in Reliance retail.

The only remotely comparable funding streak was Uber’s 2014-16 fundraising sprint, when they got checks from Blackrock, Google, KPCB, Menlo, Sherpa, Summit, Wellington, Qatar’s sovereign wealth fund, Valiant, Lone Pine, NEA, Baidu, Goldman, Times Internet, Foundation, Microsoft, Tata, Tiger Global, T. Rowe, Saudi Arabia’s sovereign wealth fund, and Softbank. If you were in a position to write checks for $100m or more in 2014-2016, there was a good chance you wrote one to Uber. And if you could write the same kinds of checks in 2020, you probably wrote one to Jio.

Jio’s business has been covered well in a few places. There were good takes from Bens Evans and Thompson ($). The basic story is that Jio made a massive capital investment ($32bn through 2018) in a network designed for data as well as voice. They charge for data, and voice is free. A good template for understanding successful tech companies is that they spend whatever it takes to be adjacent to a significant amount of economic activity, then they identify which parts of it create the most value, and gradually take those over. American telcos took a stab at this in the early 90s, with various interactive TV ventures that didn’t pan out, and the big winners turned out to be companies that operated on the open platform of the Internet. But every situation is unique; Jio can borrow previously-vetted ideas and offer them on its platform, and—as Facebook noted in its investment press release—can connect local shoppers to merchants and instantly create one of the world’s biggest mobile payment platforms.

At the Jio level, the deal makes sense. It pattern-matches to Naspers' investment in Tencent, albeit at a later stage: owning a piece of The Everything Platform in a country with a billion people and a growing economy has, historically, been a good bet.

But there’s another reading: the deal is partly about Jio, but it’s also about Reliance. Investors bought into Jio because it has good metrics and a great story. But Reliance sold because they’d promised to reduce their debt, and a deal with Saudi Aramco didn’t work out in time ($). Reliance, as it turns out, is a fascinating company, and a great look into the way countries develop. The Jio deals reflect a very long tradition at the company, which has three comparative advantages: tolerance for risk, excellence in financial engineering, and an incredible ability to either optimize itself around regulations or optimize regulations around Reliance.

The Reliance Story

In the early 1950s, monetary authorities in Yemen noticed a concerning trend: a currency shortage. After investigating the matter, they traced it back to a young clerk in the city of Aden, who had discovered that at the prevailing exchange rate, Yemeni rials contained more silver than their face value. So he bought them for British pounds, melted them into silver, exchanged the silver for pounds, and repeated the process. That clerk, Dhirubhai Ambani, soon left Aden to return to his native India, where he founded Reliance.[1]

This is the first business anecdote related in the delightful book, The Polyester Prince, a book with enough entertaining anecdotes about Ambani’s business career that he got it banned after publication.

Most of the stories in the book are like this. Ambani identified a discrepancy between the model of reality implied by government regulations, and the actual state of the world. He turned it into an arbitrage. And he exploited it.

For example, in the 50s and 60s Reliance made a market in an interesting asset class: import permits. At the time, India’s protectionist policy only allowed companies to import raw materials in proportion to their exports, but not every exporter needed their quota. So Ambani cornered the market in yarn import permits—which gave him not just an asset, but the power to turn supply off and on at will. Monopolizing a commodity is always nice, but monopolizing an essential input that’s consumed by manufacturers with high fixed costs is better still; Reliance’s addressable market wasn’t just determined by the price a monopolist could charge, but by what factory owners would pay to avoid existential uncertainty.

Later, Reliance profited from other parts of India’s protectionist regime. Their synthetic fiber arbitrage worked like this: to make manufacturers self-sufficient, the Indian government allowed them to import raw materials only in proportion to the goods they exported. Ambani persuaded the government to let him import polyester filament yarn in proportion to the nylon goods he exported. Nylon was available cheaply in India, polyester filament was 600% more expensive when locally sourced in India than its cost when imported. So Ambani set up a closed loop: make nylon clothes from locally-sourced materials; sell them abroad; use the import quota to import polyester filament; sell it at home. And, just to be safe, he took care of the demand side, too: at least according to The Polyester Prince, Ambani sent money abroad to buy his own products at duty-free ports, and then sold them for cheap, gave them away, or even dumped them in the ocean.

The entire business was ontological arbitrage: “nylon” and “polyester filament yarn” were synonyms as far as the law was concerned, but distinct in price, and Ambani made money closing the gap.

Reliance’s timing was uncanny: when tariffs went up, Reliance happened to have stockpiled the goods in question; when their inventories ran down, tariffs dropped. It’s unclear when the system switched from Reliance knowing what the government would do to Reliance deciding what the government would do, but clearly at the peak of their power they were able to call the shots.

Reliance’s diversification shows the path businesses have to take in an over-regulated and corrupt economy. The company started out in the capital-light business of importing and exporting, then expanded into producing synthetic fibers, clothing retail, and oil refining. When they didn’t have much political pull, they couldn’t risk buying fixed assets; as they got more influence, they had a comparative advantage in taking that kind of risk. (It helped that the company’s underlying risk tolerance was, at times, flamboyantly high: Reliance once smuggled an entire factory into India, one piece at a time.) In a low-trust country, vertical integration makes sense: it’s better to control an entire supply chain than to run the risk that a competing oligarch will monopolize a key industry.

India’s economy reformed, first gradually, then in 1991 quite suddenly. And Reliance, too, reformed, in a very interesting way: they went public, and acquired a massive investor base. From 1980 to 1985, the number of equity investors in India rose from 1m to 5m, and by 1985 1 million of them owned shares of Reliance. Since equity investors are likely to be middle class and above, this gave Reliance a broader political constituency: instead of buying individual regulators with bribes, they nudged the electorate with dividends.

As a public company, Reliance engaged in some novel financial engineering—issuing convertible bonds with ambiguous conversion terms, exploiting those terms to get cash when necessary, and at one point cornering the market in their own stock. Perhaps the high point of Reliance’s financial engineering was in 1986, when the company publicly stated that earnings would rise, then found that earnings weren’t rising after all. The solution: an 18-month fiscal year. Record profits secured.

Reliance today is not the swashbuckling company it used to be. It’s now run by Dhirubhai’s son, Mukesh Ambani. It remains massive and influential. Last year, the group’s total revenues were $87bn, or 2.6% of India’s GDP. Reliance generates 9% of India’s exports. It’s the #2 energy company in the world, operates almost 12,000 retail outlets, and, of course, sells mobile phone service.

The Jio Investments, In Context

Jio is a beautiful case study in catch-up growth. This is how it’s supposed to work: a technology gets tested in rich countries, which spend more on R&D and have a large, free-spending middle class. Then, the technology gets ported to a poorer country, where a low-cost/low-margin version achieves widespread distribution. It happened incredibly fast; Jio launched in 2016, and today it has 398m subscribers. And much of this was driven by pricing. The Information says that before Jio, “Many mobile users would turn off their data plans when leaving the house to avoid running up high bills accidentally.” And now Jio’s users are consuming 12GB of data a month at an average monthly cost of $1.82.

Jio’s fundraise was opportunistic in two directions: Reliance wanted to delever, and outside investors wanted access to India’s market. It’s not a coincidence that this fundraising occurred at the same time that tensions with China erupted; a country that can ban TikTok and restrict Chinese investments can do the same to other countries, too. And, of course, it helps that Jio is getting more liquidity at the same time that its competitors mysteriously found themselves on the hook for giant fines.

And Jio is a bet on technological nationalism in another direction, too: at Reliance’s annual meeting, Mukesh Ambani promised:

That JIO has designed and developed a complete 5G solution from scratch. This will enable us to launch a world-class 5G service in India… using 100% home grown technologies and solutions. This Made-in-India 5G solution will be ready for trials as soon as 5G spectrum is available… and can be ready for field deployment next year.

This is not just a business decision. Suspicions about Huawei have turned 5G into a matter of national pride, like having a navy, a flag carrier, or a premium exported beer. Once again, Jio is going full-stack—and once again, Reliance is building something that foreign competitors will have legal difficulty competing against.

As Vedica Kant has pointed out, Mukesh Ambani used the “data is the new oil” line to talk about Jio. As the CEO of a company that actually owns oil refineries and a data-centric mobile operator, he is perhaps the only person in the world qualified to make the comparison with a straight face. But the lived experience of oil industry participants depends a whole lot on how expensive their oil is to extract, and how dicey their ownership is. Perhaps a more apt comparison is: Jio is the new Ghawar, an immensely valuable, low-marginal-cost data business whose economic owner exercises substantial control over the government.

The Jio story is really one more chapter in Reliance’s long history of coopetition with India’s government. As the game changed, Reliance remained an adaptable player: when the economy was tightly regulated and run by unaccountable bureaucrats, they played the bureaucratic game; when regulations loosened and the government got more responsive to the popular will, Reliance ensured that the populace owned plenty of their stock; and now, as more commerce and government is mediated by smartphones, they moved quickly to dominate that, too. You can even make a reasonable analogy to the early days of yarn trading: India once restricted synthetic fiber imports, and now it restricts imports of American capital. Once again, Reliance is in the middle, ready to build a business and capture an enormous markup.

[1] His founding team is a good case study in my business mafia hypothesis, that good business mafias form when there’s a group of people who all have to quit their job for reasons that are exogenous to their performance. In the case of Paypal, it was an acquisition; at Tiger Management, a few years of underperformance; at Drexel Burnham Lambert, an indictment. In Reliance’s case, the core group of early employees fled the port of Aden due to unrest and the withdrawal of the British.

Elsewhere

I did an interview on careers, education, and kids. Very fun. And in Marker, I have a piece on Uber’s Postmates acquisition and what it implies about the delivery business. There are two business models for food delivery: an asset-light model that focuses on matching buyers and sellers, and an assets- and operations-intense one. The asset-light model is a much better business at scale, but the looming question is whether there’s any way to scale without running a driver network. And I’m very happy to be a member of the new cohort of Substack fellows.

Earnings

Facebook, Amazon (disclosure: long), Apple, and Alphabet reported earnings yesterday. It was a very profitable day for companies that have recently been hauled before Congress to explain why they’re so profitable. Q2, like Q1, is a quarter where the numbers are volatile but the signal is weak: every company cautioned that the trends they’ve benefited from are not necessarily going to last forever (and Google noted that their underperformance was tied to categories like travel, which they’re more exposed to than other online advertisers).

Right before Amazon’s Q1 earnings, I wrote Amazon Sees Like a State, which still sums up my view of the company: they have so much exposure to the upside of economic growth in the US that mildly altruistic behavior—or at least behavior that generates positive GDP externalities—is to their benefit. This quarter, they tried to spend their entire operating profit on coping with Covid, and they did spend the profit they guided to, but they sold a lot more than they expected. Which adds another way that they see like a state: Amazon ran a loose fiscal policy, ramping up hiring and wages in the face of a recession. And partly as a result, the economy did a bit better than they expected, and the deficit wasn’t as big as a first-order analysis would have implied.

Amazon Sees For the State

Another part of the “tech sees like a state” thesis is that tech companies are more efficient at performing some of the services states usually provide—creating rules, adjudicating disputes, collecting taxes, etc. One other thing they’re good at is investigating crimes: the number of law enforcement requests to Amazon is up 23% Y/Y so far this year.

Gerontocracy

This is an older post, but one I’ve been thinking about a lot: in 2005, the average newly-hired CEO of a Fortune 500 or S&P 500 company was born in 1959. In 2019, the average newly-hired CEO of one of these companies was born in… 1960. I can’t help but think that there’s a parallel to the decline in real rates over the last few decades: when productivity drops and the population ages, there’s a savings glut that pushes up the price of financial assets. This redistributes money to the people who bought those assets early. Something similar might be happening with reputational and political capital: when the world doesn’t change fast enough, the people with political capital accumulate more. And one consequence of that is that both Presidential candidates today are older than the winner of the 1992 election.

This story has a happy ending, though: people with a vast amount of accumulated political capital will be very risk-averse, which is another way to say that they’ll be very conformist. So any sweeping change in the country’s political views will wipe out the older generation’s influence.

M&A in Kids YouTube

A London-based company has raised $120m to consolidate kids' YouTube channels, and has now acquired channels with 235m subscribers and 7bn monthly views. Kids' YouTube is a fever dream of surreal, relentlessly A/B-tested content: CG animals, hyperkinetic entertainers, royalty-free sound effects, keyword-stuffed headlines, and talking trucks. Monetization is trickier; one of the first computer skills children learn is to hit “skip ad”. So it’s hard to be optimistic about this deal.

It is an interesting signal, though, since it’s yet another example of companies rolling up participants on a big tech platform. 101 Commerce and Perch are doing it on Amazon, and there’s a whole ecosystem of companies that buy out SEO-driven sites. Building a business on a platform is risky, because the uncontrollable risk is that the platform will change its rules and eliminate the business (as has happened to many companies that depended on YouTube, Amazon, or Google). Which gives large-scale buyers some diversification: as long as platform randomness is truly random, they get diversification. But, like any diversified investor, the asset class they choose is a bet, too.

Monopolists Still Compete

My framework for understanding monopolistic tech companies is that at any point in time, they do have monopolistic economics, but preserving them is a relentless struggle. There’s a high-level selection for CEOs who are good at planning very far ahead—it’s been observed that tech companies look unbeatable right before they start losing share, but it’s also true that there are relatively few recent examples. Still, it’s useful to watch that process play out:

Walmart wants remote control manufacturers to remove the Amazon Prime button: when an e-commerce retailer competes by offering cheap TV shows, it means brick-and-mortar retailers can retaliate by leaning on the manufacturers of TVs.

TikTok allocated $200m to fund creators a few days ago. After Instagram started poaching some of their stars, they upped the fund to $2bn.

Fred Wilson says big tech should be opened up, not broken up. But this has a disparate impact: the companies that win from better distribution will lose in a more open environment; Microsoft earns billions of dollars from the fact that .xlsx is the lingua franca for financial models, for example. But companies that win because they keep costs low and sell literally everything would clean up in a more open world, so Wilson’s policy proposal would end up being a massive benefit to Amazon. I’ve argued before that Amazon could and should preemptively spin off AWS as an independent company; they already ostensibly operate as if it is. Amazon already functions as a sort of privately-held zaibatsu, offering financial and cultural capital to independent subsidiaries that all happen to have the same economic owner. But their corporate structure makes common ownership less strategic than it is for other tech companies.

China, Infrastructure, and Risk-On

During the great financial crisis, basically every asset was either a bet on an economic rebound or a bet on a continued depression. There wasn’t a good case for thinking that real estate would recover but autos and copper prices wouldn’t. So investors learned to think in terms of risk-on and risk-off trades, which all moved roughly in tandem. That may be a bad habit. China is fighting the global economic slowdown through infrastructure spending, but unlike 2008, they don’t have a lot of low-hanging fruit in that department. Relative to GDP, China’s road and rail investment is basically in line with the US’s. Of course, since exports are at rich world consumers' discretion and construction is up to the Party, China can certainly hit GDP targets by building more stuff. But it changes the nature of some trades: now, iron and copper prices are the risk-off trade, the bet that the economy will slow and China will be forced to build more to compensate.

Fintech is all about CAC, Part #1281241

A frequent Diff theme is that there are all sorts of clever ideas for structuring loans, redesigning insurance, incentivizing people to invest prudently (via robo-advisors) or to be degenerate gamblers (Robinhood), but that the only thing that determines success in fintech is the cost of getting new customers. As evidence, I present Affirm, which is allegedly planning an IPO at a valuation of up to $10bn. Affirm’s clever financial product is selling goods on credit, which has existed for generations. But their clever CAC-minimization trick is to offer it at the point of sale, where the cost of getting the customer is minimal.

Dollar Shortages, At Home And Abroad

The dollar has been weak lately. There are two theories:

The very reasonable one, that Europe will grow faster than the US in the near future, and the interest rate differential has collapsed, so savers no longer have an incentive to shift from Euros to dollars.

The more entertaining one, that the dollar will stop being a reserve currency.

I’m skeptical of the latter, to say the least. Reserve currencies are incredibly durable; Britain had to fight two costly wars, lose an empire, and then wait a decade before the pound lost its reserve status. And that was in the comparatively un-globalized and un-financialized 1950s. Today, dollar debts are ubiquitous, and have to be serviced in dollars—so the global commodities trade is priced in dollars, which reinforces the utility of dollar debt.

In emerging markets, The Economist writes that there are epidemic costs over the next decade, which will shrink economies relative to their dollar debts. And domestically, Congress has procrastinated past the point of no return on a revised stimulus bill. While a student loan payments pause might be continued past September, expanded unemployment benefits will suffer a hiccup at minimum and perhaps an extended break: the debate is between a small unemployment boost or a large one, but the interim compromise is zero. Right now, the estimated cost of a cut in unemployment benefits is between 1m and 5m jobs by year-end. When developing market exporters borrow in dollars, the Fed can address a dollar shortage through their countries’ banking systems. But when American borrowers owe dollars, it’s much harder for the Fed to provide direct assistance.

Second Acts

I’ve always had a soft spot for Business Insider. Scrappy tabloids are fun, journalists who break news are fun, and clickbait factories are pretty easy to scroll past. Another thing I like about them is that their founder has a great dramatic arc, as exemplified in this profile: he was a star analyst, he got a little too cocky (depending on who you ask he either lied about the companies he covered or made some ill-advised jokes over email—I lean towards the latter), got banned for life from his chosen industry, launched his journalistic career by covering somebody else’s stock-related trial, and then found his true calling.

It’s also a story that illustrates an important perceptual gap. If you surveyed Americans and asked which was the more important institution, journalism or equity research, I assume the vast majority of respondents would say that journalism is more important. But in equity research, you can get in trouble for being wrong, and if you’re wrong in a way that appears malicious rather than just inept, you can literally be forbidden from working in the job, forever! Socially, we think journalism is very important, but the regulatory state treats stock picking as a sacred public trust that can’t be sullied by the appearance of impropriety.