We all live in a product led growth world! What a week this week as there have been some marquee financings from Loom, Pitch, and Dooly (a portfolio co) along with Monday filing an S-1. Bottom line, investors are throwing big 💰 at these companies because of the incredible growth and efficiency from a PLG model. Notice how all have a huge collaboration element as well, so fitting for a hybrid working world.

First up is Loom, a workplace video messaging platform, which raised a $130M round led by Andreessen Horowitz more than quadrupling its valuation from a year ago to $1.5B 🦄.

The company has achieved true viral status, a rarity in enterprise software, growing active users 900% year-over-year. It’s now used by 10+ million people across 120,000 companies and 192 countries to get work done wherever, whenever – without sacrificing creativity, productivity, or culture.

Loom grew revenue by more than 1,100% this past year, adding enterprise customers including Netflix, Atlassian, JLL, Twitter, Olympus, Procter & Gamble, and Lacoste. Spanning all geographies, departments, and titles, users rely on Loom to share updates, provide feedback, communicate with customers, and augment meetings. Its asynchronous video messages accelerate the speed of information sharing while also fostering cultures of connection and engagement.

Next up is Pitch, a collaborative presentation platform or next gen Powerpoint, raised $85M led by Tiger Global. No data or metrics shared other than plans to go enterprise with a big vision to boot.

“In our first six months since launching Pitch, we’ve primarily focused on teams of up to 200 people, primarily in small and medium-sized companies, but also larger enterprises,” Pitch cofounder and CEO Christian Reber told VentureBeat. “We aim to be fully enterprise-ready in 2022 and are already implementing improvements to support larger workspaces with significantly bigger teams, as well as meeting enterprise-grade standards.”

Finally, a huge congrats 👏🏼 🎊 to Dooly, (boldstart portfolio co) which is building a connected workspace for revenue teams and raised an $80M Series B led by Spark Capital and including Tiger Global, Greenspring and others.

Techcrunch here along with Globe and Mail with these stats:

Dooly has posted strong numbers driven by high adoption and word-of-mouth referrals. The number of organizations using Dooly has increased about 10-fold to 500 since early 2020, including Asana and BigCommerce, while the individual user count has expanded by a greater rate, 10,000-plus people. More people signed up in March than in all of 2020, Mr. Hartvigsen said. He said Dooly benefited from the pandemic as salespeople affected by budget cuts and travel restrictions flocked to online tools to increase their productivity. “Were we a beneficiary of a really rotten thing for mankind? Yes,” he said.

Other metrics have turned heads among investors. The product’s net promoter score, a measure of user recommendations, is 79, which is high. Its “net revenue retention” or the amount of recurring revenue from existing customers, is well above the norm at 162 per cent, meaning existing customers on average increase their spend on its products by 62 per cent year over year. Customers use Dooly 2.5 to five hours a day on average, Mr. Hartvigsen said.

Moving on, Monday filed its S-1 - lots of trends to watch here, concept of WorkOS, low code no code, product led growth metrics. I share some of the 🔑 nuggets on the business below.

monday.com democratizes the power of software so organizations can easily build software applications and work management tools that fit their needs. We call our platform ‘Work OS’, and we believe we are pioneering a new category of software that will change the way people work and businesses operate.

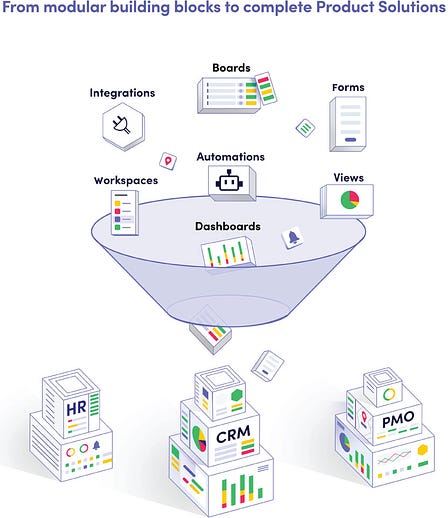

Our platform consists of modular building blocks that are simple enough for anyone to use, yet powerful enough to drive the core functionality within any organization. Our platform also integrates with other systems and applications, creating a new connective layer for organizations that links departments and bridges information silos.

Notice the delineation on Net $ retention with a caveat of >10+ users to get to 121% - overall net $ retention is at 107% which makes sense given high churn of SMBs. Datadog which is best in class is still over 130% NRR.

Customers with more than 10 users are the core focus of our sales and marketing efforts; therefore, their Net Dollar Retention is a key metric we measure. We expect the percentage of ARR attributable to customers with more than 10 users and the Net Dollar Retention Rate for these customers to continue to increase. Additionally, our Net Dollar Retention rate for all of our customers was 100%, 105% and 107% for the three months ended December 31, 2019 and 2020 and March 31, 2021, respectively.

Here’s another great slide on product and growth:

Outline of Monday GTM Motion:

Sales and Marketing

We employ a hybrid approach to sales and marketing, combining an extensive self-serve funnel with direct sales from our partners and sales team.

Marketing

With our bottom-up marketing approach, we initially target customers on the team level. We cast a wide net of performance-based marketing, brand advertising and organic marketing across several digital and offline channels.

Because of this wide reach, our marketing efforts bring a variety of leads, from small businesses to Fortune 500 companies. Upon discovering our platform, customers enroll in a 14-day free trial of our Pro plan, after which they are prompted to either continue with our Free plan for small teams (limited to two users) or pay for one of our four paid subscription plans. As these customers convert and realize the benefits of our platform, they invite more teams to join. As a result, we also benefit greatly from viral, word-of-mouth marketing.

Sales

As our self-serve funnel customers grow, and as part of our flywheel sales approach, our sales teams actively monitor customers’ usage patterns and engage to help them achieve their goals and become more successful. Our sales team is comprised of account executives and account managers, who are segmented by region and customer size. Our account executives are primarily focused on acquiring new customers while our account managers are primarily focused on helping existing customers expand their usage within their organization.

Also remember PLG does not mean no sales, trick is knowing when to “assist” on an account. Monday has invested significant 💰 scaling its sales headcount. As a founder, you need to know when to lean in and invest more $$$ to scale growth.

In mid-2018, as we experienced rapid growth and demand for our platform through our self-serve funnel, we began investing in building out and scaling our sales, customer success and partners teams. We are still in the early stages of building out and scaling these teams, but we believe there is a significant expansion opportunity within our customer base to continue to grow our platform. In order to realize this opportunity, we have more than doubled our sales and customer success teams from 154 employees at the end of 2019 to 365 employees as of March 31, 2021.

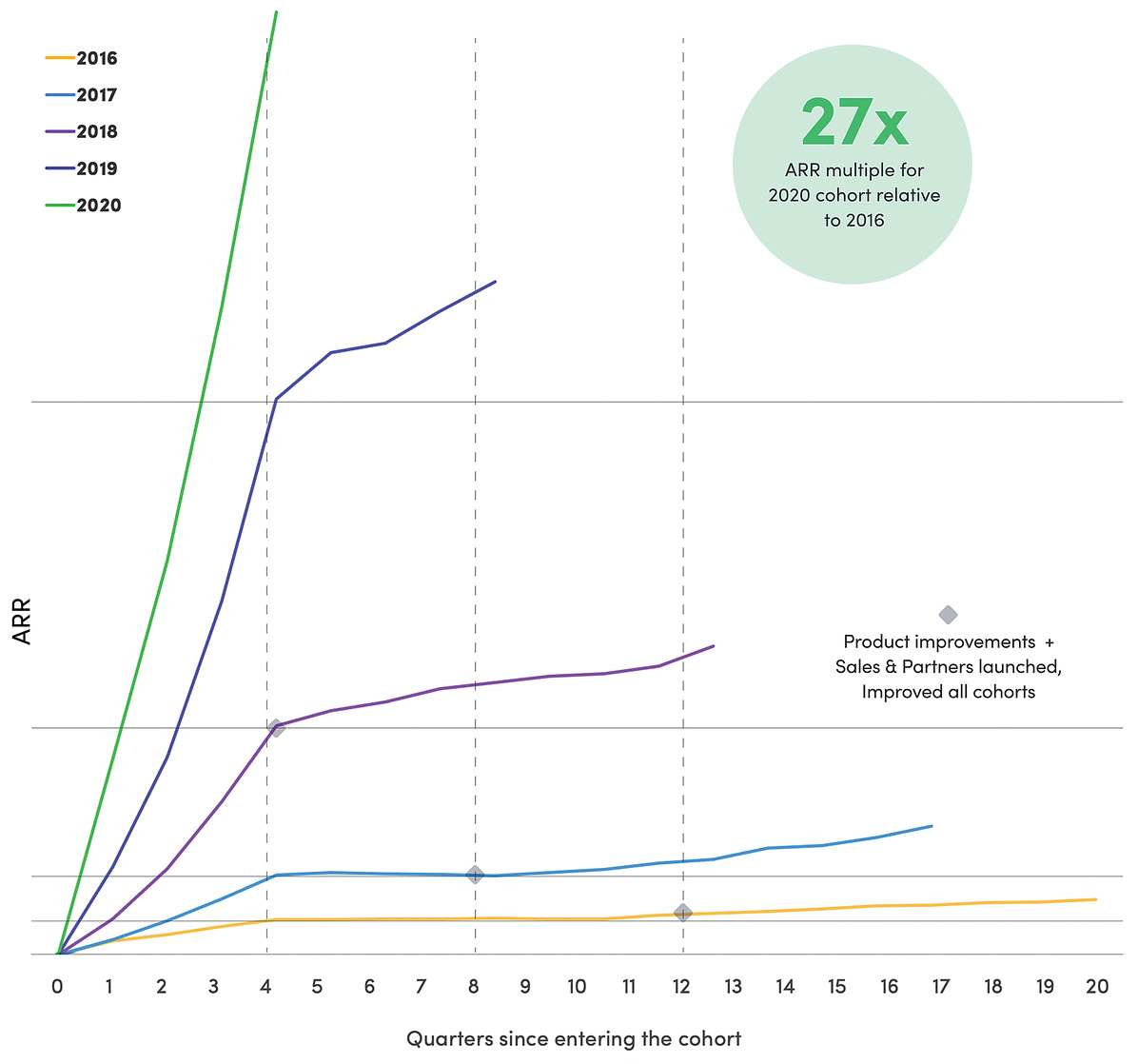

In addition, a significant investment has been made to target accounts > 10 users to start and results in higher ARR and $ net retention.

Historically, customers would adopt and expand on the platform on a self-serve basis, independent of any assistance. In addition to our self-serve funnel, as of 2018, we began to invest in our sales, customer success and partners teams to help our customers obtain more value out of the platform. As a result of the investments described above, we have seen significant growth in the customer spend from our cohorts during the first 12 months of their subscriptions to monday.com. For example, the new ARR generated from our 2018, 2019 and 2020 cohorts was higher than the new ARR generated by our 2016 cohort by 6.7x, 16.0x and 27.1x respectively. Additionally, we have also seen the rate of expansion from our 2017 and 2016 cohorts accelerate in recent years due to our sales and customer success teams helping them gain more value out of the platform. For example, our 2016 cohorts grew 21% and 29% for the years ending 2019 and 2020, respectively, while our 2017 cohorts grew 21% and 33% for the periods ending 2019 and 2020, respectively.

This also includes upselling additional products into the Monday installed base resulting in a high attach rate.

As a result, as of April 30, 2021, 96% of our enterprise customers use monday.com for at least two Product Solutions and 63% of our enterprise customers use monday.com for at least three Product Solutions.

Important to note that when it comes to PLG, analytics and understanding key metrics around the top of funnel, usage, expansion, predicting churn is a must have.

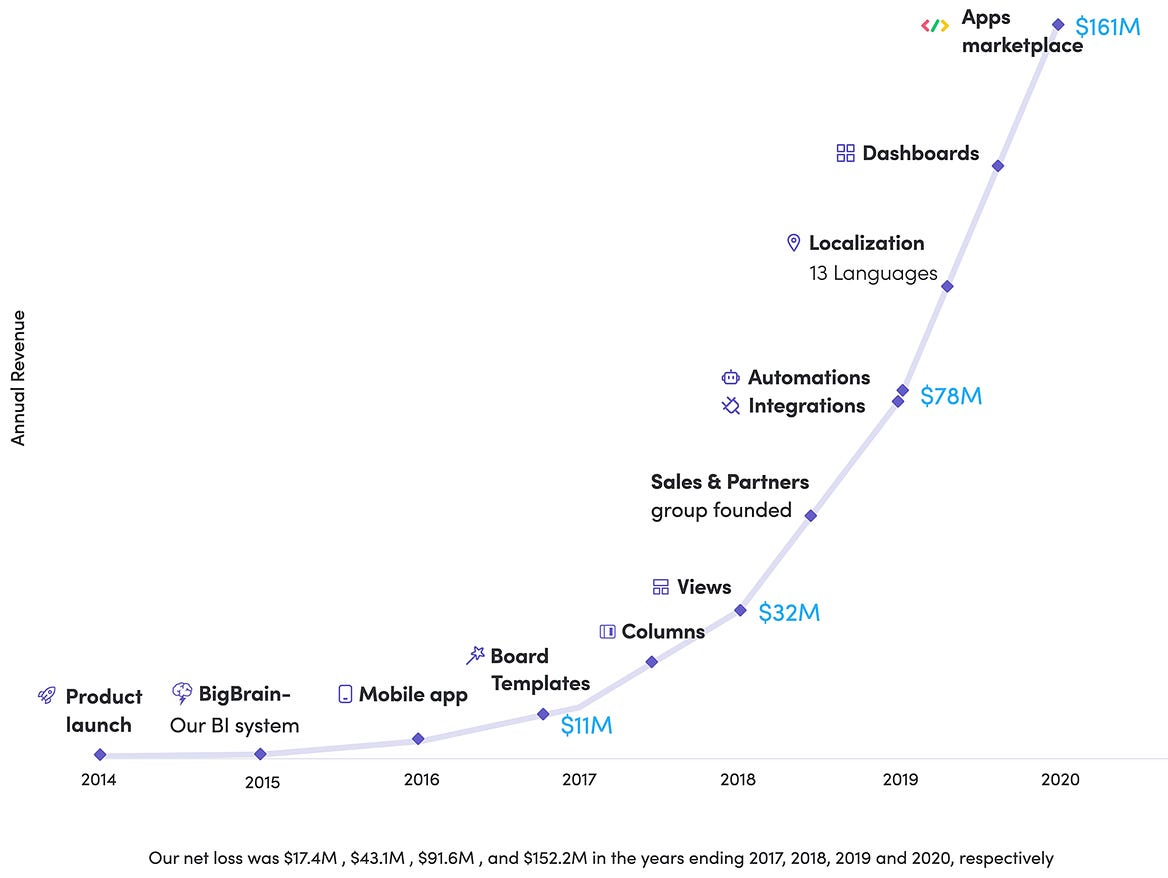

Our in-house business intelligence tool, BigBrain, supports our data-driven culture by providing every monday.com employee easy access to all of the Company’s core data that is required for their job. We believe this allows our employees to work efficiently and provides them the ability to do their job the best way possible.

BigBrain collects and processes data from over 200 million events per weekday from multiple separate sources and aggregates it into one place that every employee can access. This enables our team to analyze and make informed decisions based on transparent data, in real time. BigBrain includes various tools such as a landing page generator, an AB test tool and media buying statistics tracking, all of which were built by our in-house team. BigBrain also aligns our team around key performance indicators (“KPIs”) and metrics. We proactively connect employees to the business status by sending a daily SMS with high-level KPIs and strategically distributed data dashboards powered by BigBrain throughout our offices.

We believe BigBrain supports our core product by paving the way for quick-to-market, efficient and high-quality execution. It also aligns with our values of transparency and trust within the monday.com culture.

Monday also has made a significant investment in brand, advertising and marketing. PLG does not happen just by word of mouth and when companies scale they need to keep reaching more users.

Sales and marketing expenses were $191.4 million for the year ended December 31, 2020, an increase of $72.9 million, or 61%, compared to $118.5 million for the year ended December 31, 2019. This increase was primarily driven by an increase of $30.8 million in marketing, advertising and brand costs

Just for comparison’s sake, here Asana spent $106M in Sales and Marketing in its prior YE, having doubled its investment.

Sales and marketing expenses increased $53.7 million, or 103%, for fiscal 2020 compared to fiscal 2019. The increase was primarily due to an increase of $26.1 million in personnel-related expenses as a result of higher headcount and sales commissions for our sales personnel and $7.0 million in higher tender offer-related stock-based compensation expense, an increase of $13.7 million in advertising expenses for our marketing programs, an increase of $7.2 million in fees to marketing vendors, and an increase of $3.6 million in allocated overhead costs as a result of increased overall costs to support the growth of our business and related infrastructure.

More on the PLG motion and need to invest in growth.

Self-Serve Funnel Complimented by Expanding Sales-Led Motions

Our focus on seamless adoption of our platform starts with ensuring that customers can easily and independently get up and running on our Work OS. This is accomplished through a self-serve funnel where virtually any user can sign up and immediately gain value, regardless of their technical skills.

Once customers adopt the platform and realize its value, their usage often grows organically, expanding across use cases and departments. As this expansion takes place virally, it is also accelerated through our sales-assisted motions and our partners network. Our customer success teams engage with our customers in an effort to help them grow and achieve their business objectives through our platform. This has created a successful growth cycle: the more value customers gain from our platform, the more new users and use cases are added by such customers, which in turn adds even more value to our customers.

Get users in with an app, get them to stay with the platform, custom building blocks, etc for stickiness.

Spells out massive TAM

Competition:

The markets in which we operate are extremely competitive, fragmented and subject to rapidly changing technology, shifting user and customer needs, new market entrants and frequent introductions of new products and services. Moreover, we expect competition to increase in the future both from our existing competitors and from new market entrants, including established technology companies who have not previously entered the market. Our competitors include the following:

companies that primarily offer project and work management solutions, including application of processes, methods, skills and knowledge to achieve specific objectives. This includes companies such as Asana, Inc., Wrike Inc., SmartSheet Inc., Notion, Inc., Citrix Systems, Inc., Zendesk, Inc. and Freshworks Inc.; and

companies that offer Product Solutions across other use cases we serve, such as customer relationship management solutions, software development tools and marketing campaign management. This includes companies such as SugarCRM, Pipedrive, Zoho, Inc., Atlassian Corporation PLC (Jira), Procore Technologies, Workday, Inc., BombooHR, LLC., Hootsuite Media Inc. and Adobe Experience Cloud.

As always, 🙏🏼 for reading and please share with your friends and colleagues.

Share What's Hot in Enterprise IT/VC

Scaling Startups

All about the product culture at Stripe from deep thinking on long form documents (same as Hashicorp) to “product shaping” - great 🧵

👇🏼 Leading indicators of success from day one, product velocity (Paul Graham) and my #1a, hiring quality + velocity

Before you take that big 💰 - read 🧵

💯

Enterprise Tech

KubeCon Europe 2021 Wrapup from Daniel Bryant, Ambassador Labs (h/t Gareth Rushgrove) - great to see user experience for developers matters and emphasized this year.

Here are our key takeaways from KubeCon EU 2021:

Developers, and developer experience, within cloud is a big deal

End users are making a big impact in the cloud native world right now

Networking in the cloud (and K8s) is still evolving

Open standards are providing key abstractions, extensibility, and innovation

Control planes are where the most end user value is being created

Anyone can (and should) contribute to the community: Docs are a great place to start

Cybersecurity spend is at an all time high yet…”On average, 64% of CISOs surveyed said they felt like their organization is at risk of suffering from a material cyberattack in the next 12 months, with more than 65% of CISOs from the U.S., France, UAE, Australia, Sweden, Germany, U.K. expressing this fear.” (Proofpoint survey)

Scale Ventures Cybersecurity Perspectives 2021 Report along with 🔑 findings:

Security budgets and staff rose during the pandemic and will grow after SolarWinds - think 3rd party risk and vendor software supply chain

The rush to remote work increased security risk

The chain of command matters for security

Automation can’t come soon enough

Data privacy remains an investment priority

😲 No wonder why cybersecurity market is on 🔥 with $40M ransomware payments

And more from Nikesh Arora, CEO of Palo Alto Networks, on the rise of ransomware from the earnings transcript this past week:

After the December SolarStorm attack, we saw an acceleration in attacks throughout our third quarter and after the quarter closed.

These range from software supply chain attacks like SolarWinds and to run somewhere attacks like on your pipeline. Ransomware especially has been in a spotlight recently. And data from our own Unit 42 shows that the average ransom paid in 2020 tripled from 2019. And in 2021, it's more than doubled again.

The highest demand we've seen is $50 million, up from $30 million in 2020, with organized groups with near nation-state discipline perpetrating coordinated attacks. The targets are not only corporations, with healthcare and pharma is a focus with the pandemic, but also government organization and shared infrastructure. The reason for this vulnerability is deep-seated. Organizations run their operations on technology that is decades old, sometimes predating the Internet.

What’s 🔥 from RSA - Top 5 Most Innovative Cybersecurity Startups (CRN) - great to have BigID, Snyk, and Hypr (3 portfolio cos) along with Orca and BitSight

RPA space continues to be hot but expect a wave of consolidation - latest on Google Cloud - don’t be surprised if they enter with a big acquisition one of these days - from Thomas Kurian

The first step is to use data to understand what the most valuable processes might be to automate. This may be driven by cost reduction or seeking competitive advantage by speeding up, for example, the process of originating a loan compared to competitors.

The second step lies in finding the best way to automate the business process. Process mining and process discovery can find ways to reduce certain steps from the process. These can be implemented with RPA and low-code tools.

What is VMware’s new CEO Raghu Raghuram plans as a standalone company? (Business Insider) - multicloud, more focus on developers, and more M&A

VMware's top goal is to become a leader in multi-cloud, Raghuram said, where customers can easily use its software to run their applications on any (and as many) clouds as they want. The firm will "build aggressively" to get there, he added, and expects the journey to span years

VMware plans to continue building on some strategies it's already laid in place. It recently started a business unit called the Modern Applications Platform Business Unit to build cloud and developer applications that help customers update their technology. This business unit has seen "tremendous" growth, Raghuram said.

VMware may also do some M&A in the coming years, Raghuram said. It's looking for companies that could help its customers build modern applications and run them on the cloud – which would complement VMware's home-grown technology, Raghuram said.

Did someone say hybrid work? Super cool on what’s coming from Microsoft Teams…

Markets

This too shall last longer as hedge funds are continuing to go earlier and earlier and invest more 💰 in private companies (from the WSJ)

Lone Pine is increasing to 15% from 5% the amount its hedge fund and long-only fund can invest in private companies, with investors opting into the increased exposure. Flight Deck Capital LP, a San Francisco fund started by Jay Kahn, launched May 1 with $250 million and the ability to invest a quarter of its assets under management in private companies. Mr. Kahn previously led or co-led most of the private investments at Light Street Capital Management and also invested in public companies.

Private investments have gained in popularity as several hedge-fund firms with significant private-investing efforts have posted some of the best returns in the industry. Tiger Global Management LLC, a pioneer in the hybrid approach that began investing in private companies in 2003, Coatue Management LLC and D1 Capital Partners LP have all boosted their returns by investing in private companies.

To the above point: Growth Firms, Not VCs, Are The Most Active Investors In New Unicorns This Year, And They’re Doubling Down (Crunchbase News)