Net Interest - The Last Challenger

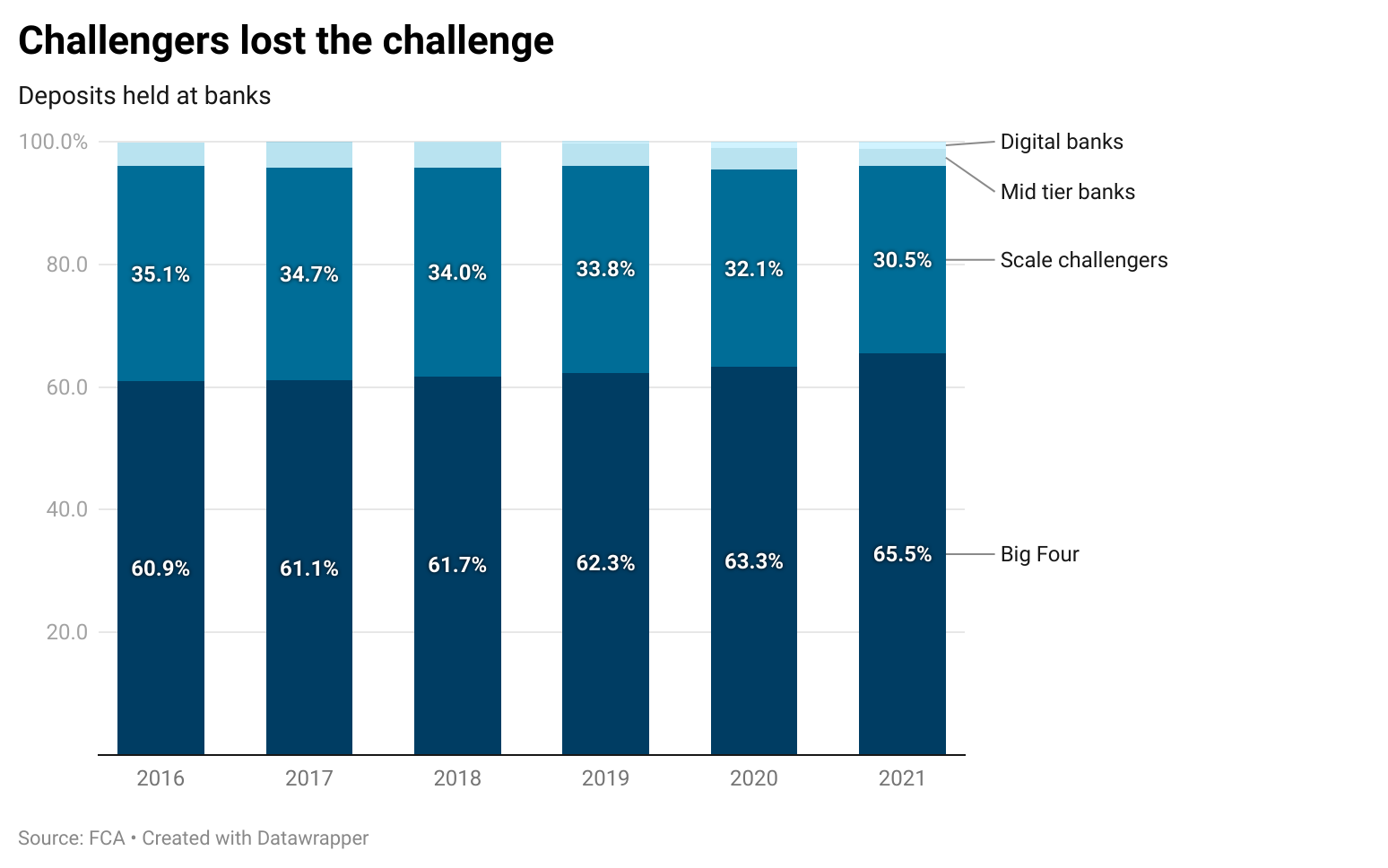

On the evening of Monday 15 September 2008, the day Lehman Brothers failed, the chairman of Citigroup hosted a dinner for fellow financiers at the end of his two-day board meeting in London. The venue was Spencer House, ancestral home of Princess Diana, “one of the finest houses ever built in London”, although few present were in the mood to enjoy its lavish surroundings. Citigroup’s stock had fallen 15% that day as repercussions from Lehman’s failure swept through markets, and bankers from other firms felt no more secure. The atmosphere was decidedly tense. One of the guests was UK Prime Minister, Gordon Brown. The event had been in his diary for months and although he didn’t stay for dinner, he was keen to canvass views and provide reassurance at the drinks reception beforehand. He also needed to deliver a message. Sir Victor Blank, chairman of Lloyds TSB, the country’s fifth largest bank, had previously briefed him on Lloyds’ ambition to merge with HBOS, the country’s fourth largest bank. On a flight they shared back to the UK in July, Sir Victor bemoaned that any referral to the competition authorities would render a deal unviable because of the delays it would create to complete. Even then, the environment was febrile – HBOS had just failed in an effort to place new shares with investors – and Sir Victor didn’t think it could survive the uncertainty of a drawn-out merger process. Gordon Brown replied that he would discuss the matter with colleagues in government. Now, with events escalating, he had his answer. “We recognise your argument that you could not go through the competitions process, particularly if there was a full review,” he told Sir Victor. “Halifax Bank of Scotland could not survive it, so if you still want to do it, you should get on with it quickly.” The Prime Minister said that he’d scheduled a meeting the next morning with the Chancellor of the Exchequer and the Governor of the Bank of England to get the process moving. After the Prime Minister left, Sir Victor caught the eye of his chief executive officer, Eric Daniels, and ushered him outside. “It’s as firm an assurance as he can give,” he told him. As Blank went back inside to dinner, Daniels rushed off to call Andy Hornby, his opposite number at HBOS, asking him to assemble his executive team for a meeting first thing in the morning. Later in the evening Blank got hold of the HBOS chairman, (Lord) Dennis Stevenson, to tell him: “Dennis, we’ve got the go-ahead from Gordon Brown on the competition issue. But we need to move fast.” Three days later, the deal was announced. The new bank would become the largest in the UK. In the personal current account market, its share would be 33%, higher than its three main rivals whose shares stood between 14% and 17%. In mortgages, its share would be 28%, again higher than the next biggest player whose share was below 20%. And in small- and medium-sized business lending (SME), its share was between 20% and 30%, reaching close to 50% in Scotland, where both banks had a strong franchise. Unsurprisingly, the UK Office of Fair Trading (OFT) took note. In a report filed in October, it wrote: “The OFT considers that there is a realistic prospect of a substantial lessening of competition in three areas: personal current accounts (PCAs), SME banking and mortgages. More specifically, the OFT has medium to long-term concerns (Stage II) in relation to all three product areas, and in addition short-term concerns (Stage I) in relation to PCAs and SME banking.” But true to his word, and with concerns growing around HBOS’s ability to fund itself as an independent entity, Gordon Brown intervened. A law was already in place – the 2002 Enterprise Act – that allowed a Secretary of State for Business to override competition concerns if there’s a “public interest consideration”. At the time, public interest considerations stretched to national security and certain media situations, not to financial stability. The law was duly amended and at the end of October, the Secretary of State for Business confirmed that the deal could go through without referral to the competition authorities. “The merger will result in significant benefits to the public interest as it relates to ensuring the stability of the UK financial system,” the Secretary of State wrote. “These benefits outweigh the potential for the merger to result in the anti-competitive outcomes identified by the OFT.” We’ve talked about this trade-off before, between competition and financial stability in financial services. It reared its head again in Switzerland last year. But trade-offs are rarely clean, and when the immediate peril of banking collapse receded, the UK government tried to make amends. Starting in 2010, it embraced the idea of the “challenger bank”, whose goal would be to wrestle back market share from the Big Four banks. A parliamentary inquiry into competition and choice in retail banking concluded that “further measures are required to promote competition in the retail banking sector and ensure improved outcomes for consumers.” It suggested that “poor consumer outcomes can be addressed by reducing barriers to entry and expansion – in order to promote greater competition between existing players and to encourage new entry.” That year, newcomer Metro Bank was awarded the UK’s first full banking license in over a century, with 36 more banks having been given approval since 2013. The only problem: it hasn’t really worked. Metro narrowly avoided collapse last year, and other neobanks’ ambitions have been stymied. A strategic review of retail banking business models commissioned by the Financial Conduct Authority in 2022 concluded that in the personal current account market, “challengers have struggled to grow market share.” In addition, because they compete for customers by offering higher interest rates, and lack the scale over which to spread technology costs, their returns are lower, making it more difficult for them to finance growth. Which leaves promoting greater competition between existing players as the route to improve outcomes. In the same inquiry, Virgin Money gave evidence that there “was no credible alternative to the large banks for full-service banking, except to some extent Nationwide and the UK subsidiaries of National Australia Bank.” Since then, Virgin Money has merged with the UK subsidiaries of National Australia Bank and last week, the resulting group announced a merger with Nationwide, to form the largest competitor to the Big Four. To see how tough it is to mount a challenge to the UK’s Big Four banks, through the experience of Virgin, read on.

Continue reading this post for free, courtesy of Marc Rubinstein.A subscription gets you:

|

Older messages

Big in Japan

Friday, March 8, 2024

The Rise and Fall and Rise of Nomura ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Tony Robbins’ Favorite Asset Class

Friday, March 1, 2024

Inside the “GP Stakes” Business ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The Third Network

Friday, February 23, 2024

Capital One's Pursuit of the Holy Grail ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The Ackman Discount

Monday, February 19, 2024

Inside Bill Ackman's Listed Hedge Fund Complex ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Funding Mr Bates

Friday, February 9, 2024

Litigation Finance: The Rise of an Asset Class

You Might Also Like

Longreads + Open Thread

Saturday, March 8, 2025

Personal Essays, Lies, Popes, GPT-4.5, Banks, Buy-and-Hold, Advanced Portfolio Management, Trade, Karp Longreads + Open Thread By Byrne Hobart • 8 Mar 2025 View in browser View in browser Longreads

💸 A $24 billion grocery haul

Friday, March 7, 2025

Walgreens landed in a shopping basket, crypto investors felt pranked by the president, and a burger made of skin | Finimize Hi Reader, here's what you need to know for March 8th in 3:11 minutes.

The financial toll of a divorce can be devastating

Friday, March 7, 2025

Here are some options to get back on track ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Too Big To Fail?

Friday, March 7, 2025

Revisiting Millennium and Multi-Manager Hedge Funds ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The tell-tale signs the crash of a lifetime is near

Friday, March 7, 2025

Message from Harry Dent ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

👀 DeepSeek 2.0

Thursday, March 6, 2025

Alibaba's AI competitor, Europe's rate cut, and loads of instant noodles | Finimize TOGETHER WITH Hi Reader, here's what you need to know for March 7th in 3:07 minutes. Investors rewarded

Crypto Politics: Strategy or Play? - Issue #515

Thursday, March 6, 2025

FTW Crypto: Trump's crypto plan fuels market surges—is it real policy or just strategy? Decentralization may be the only way forward. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

What can 40 years of data on vacancy advertising costs tell us about labour market equilibrium?

Thursday, March 6, 2025

Michal Stelmach, James Kensett and Philip Schnattinger Economists frequently use the vacancies to unemployment (V/U) ratio to measure labour market tightness. Analysis of the labour market during the

🇺🇸 Make America rich again

Wednesday, March 5, 2025

The US president stood by tariffs, China revealed ambitious plans, and the startup fighting fast fashion's ugly side | Finimize TOGETHER WITH Hi Reader, here's what you need to know for March

Are you prepared for Social Security’s uncertain future?

Wednesday, March 5, 2025

Investing in gold with AHG could help stabilize your retirement ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏