Hi y’all, Cokie here.

My brain has been all over the place in the last few days: I’ve learned about innovative funding strategies in e-commerce, started a piece of research on the financial journey for immigrants, and gotten the lowdown on how to *do product* from a career standpoint. In classic style, I’ve decided to write about none of these, instead opting to dig into a personal finance question I posited on twitter.

To clarify the question, I asked my followers to tell me what dollar amount of cash they need in their checking account to feel like they’re “not broke.” Broke obviously means different things to different people.

I only started to actively engage with this number recently, but realize as I look back, I have always had some weird hang up. When I was a fresh grad, making $45k, that number was $1,000. Now, at *age undisclosed because of a weirdly long game decision to keep Ian confused*, that number is now $3,000.

I’ve determined that there are a number of factors that must be considered when we think about why people settle on the numbers they do. The obvious are:

Salary

Fixed costs - rent, mortgage, bills, car, whatever

Debt - credit card

Student loans

Savings

Investments (of your own - inclusive of 401k, not inclusive of a trust fund)

The not so obvious are:

Background - ethnic and racial

Privilege - did your family come from money?

Gender

Age

We’ll use me as an example, because I write this newsletter (if we haven’t met, I’m Cokie, follow me on twitter to improve my self-worth!). I come from privilege but have also experienced debilitating debt. I have only been serious about saving money recently, because I’m finally debt free (huge achievement for me). And the second I paid off that debt, the $3,000 number stuck in my head. Because it was what I had left in my account the day my debt was paid.

I’m interested to see how you think about that number and how you got there. Take a look at the replies to the above tweet and let me know!

Due to the request of one loyal reader, I decided to make a playlist for this week's newsletter.

Chaos reigns, baby. Welcome to Funtech Friday.

The news by Cokie Hasiotis and Parker Jay-Pachirat

On Monday, Google announced plans for expansion into digital banking services, offering digital checking and savings accounts to users through the Google Pay app. 8 US banks are partnering with Google to provide users with digital-first bank accounts directly through the Google Pay app. The front-end UX UI will be managed by Google, and the financial backend managed by each respective bank. According to BMO, one of the banks partnering with Google, the Google Pay app will offer exclusive financial insights and built-in budgeting tools.

By working with a range of autonomous partners--from larger global banks to small credit unions, Google Pay increases market penetration by reaching customers they never had on their radar before. As consumer demand to manage money online increases, companies are expanding their financial services to follow suit. This past year, Apple launched it’s co-branded Apple Card with Goldman Sachs, but it has yet to offer a full banking system, just Apple Cash. Google’s plans are more extensive than what Apple has done so far. The accounts are expected to launch in 2021.

I am extremely bullish on community banks and credit unions and here’s why. Consider, for a moment, what made Uber so beloved? Yes, your drunk ass got a ride home from B Bar, but Uber is beloved because they literally *knew* that your drunk ass NEEDED a ride home from B Bar. They were obsessed with their customer from day one. Uber created a community of affinity with their product.

Community banks and credit unions are the old fashioned version of that. Through communities of geography, your banker was likely your neighbor or your friend. And they knew you really really well.

Now combine the two: a community of affinity + the personal relationship with your banker = exactly what Google has done here. Seems they may have found their way into the notes section of my phone, where I have a really long essay on why community banks are the future of financial services.

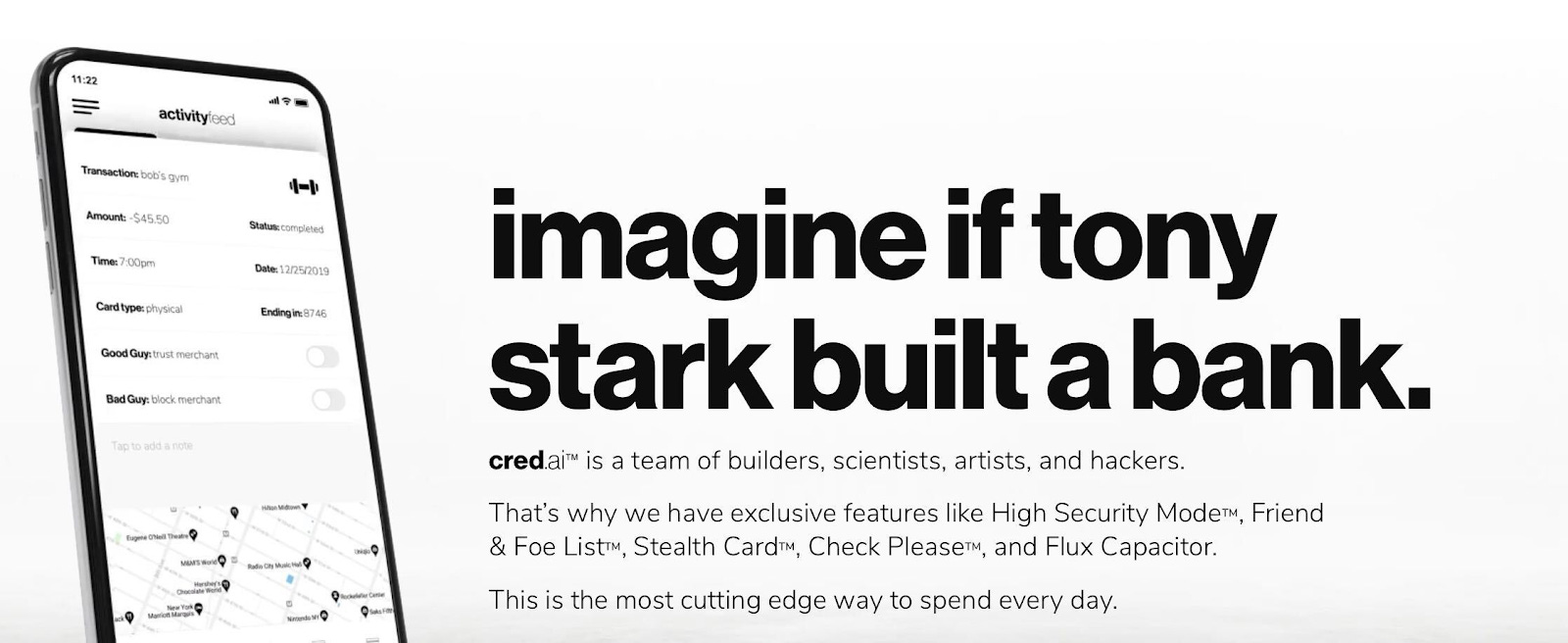

Cred.ai has come out of stealth after building for the last three years, offering a smarter credit card. No fees to the consumer ever… if you buy into their entire ethos. Using AI, Cred offers users with a more complete picture of their financial health. After calculating regular expenditure (rent, bills), Cred gives you a picture of what you can safely afford to spend. And, here’s the kicker, if you spend outside of that, they cancel the transaction. Make sure that you know your number before you impulse purchase four seasons of Gilmore Girls. It pays off your debt little by little, so that you’re not hit with a huge bill at the end of the month and improves your credit score along the way. I, for one, am into this whole thing and wish them success. Americans need to change the way we think about credit and debt, and Cred seems to be pointing us in the right direction. That said, their advertising leaves a lot to be desired for me. See what I mean?

|

Payment firm Paya, owned by private-equity firm GTCR, is nearing a merging deal with acquisition shell FinTech Acquisition Corp III. According to those familiar with the matter, this could bring Paya to a valuation of $1.3 billion (including debt). A deal could be announced early next week, though there is still room for change. Paya, FinTech Acquisition Corp III, and GTCR declined to comment. FinTech Acquisition Corp III is Daniel Cohen’s third blank-check firm, raising $345m in its 2018 IPO.

The route of going public via SPAC mergers has emerged popular during the pandemic, providing for companies an opportunity to secure a firm valuation when unsure about how their IPO would perform. If Paya is listed on the stock market, it will succeed other payment companies that have gone public in the past year- like Shift4Payments FOUR.N and Repay Holdings- who have been performing well since their share.

Fundraising news

I love news like this. Thursday morning, I was fortunate enough to receive one of the best emails you can get in my job - “we have launched!” This one is gonna be a little touchy feely because I am a huge fan of Founder & CEO Stephany Kirkpatrick (literally, ask her how many times I email her for no reason a month). Orum raised a $5.2M seed round that was massively oversubscribed… DURING A PANDEMIC.

The idea is simple - Orum wants to make moving money in real time easier and more natural. Using machine learning and data science, Orum’s debut product, Foresight, is an automated programming interface aimed at enabling financial institutions to move money in real time. Kirkpatrick told Crunchbase News, “We’ve become an instant economy everywhere else but in the banking industry, where you can’t invest your money immediately. It’s a vicious cycle for access to your money.”

Tweets of the week

Cultural change is extremely hard to do right, and it is my opinion that to get it right, it has to start from the very beginning.

In that same vein, given the state of the world, it has never been easier to hire diversely, especially with many roles going 100% remote. Look outside of your network,