State of the Network’s 2023 Year in Review

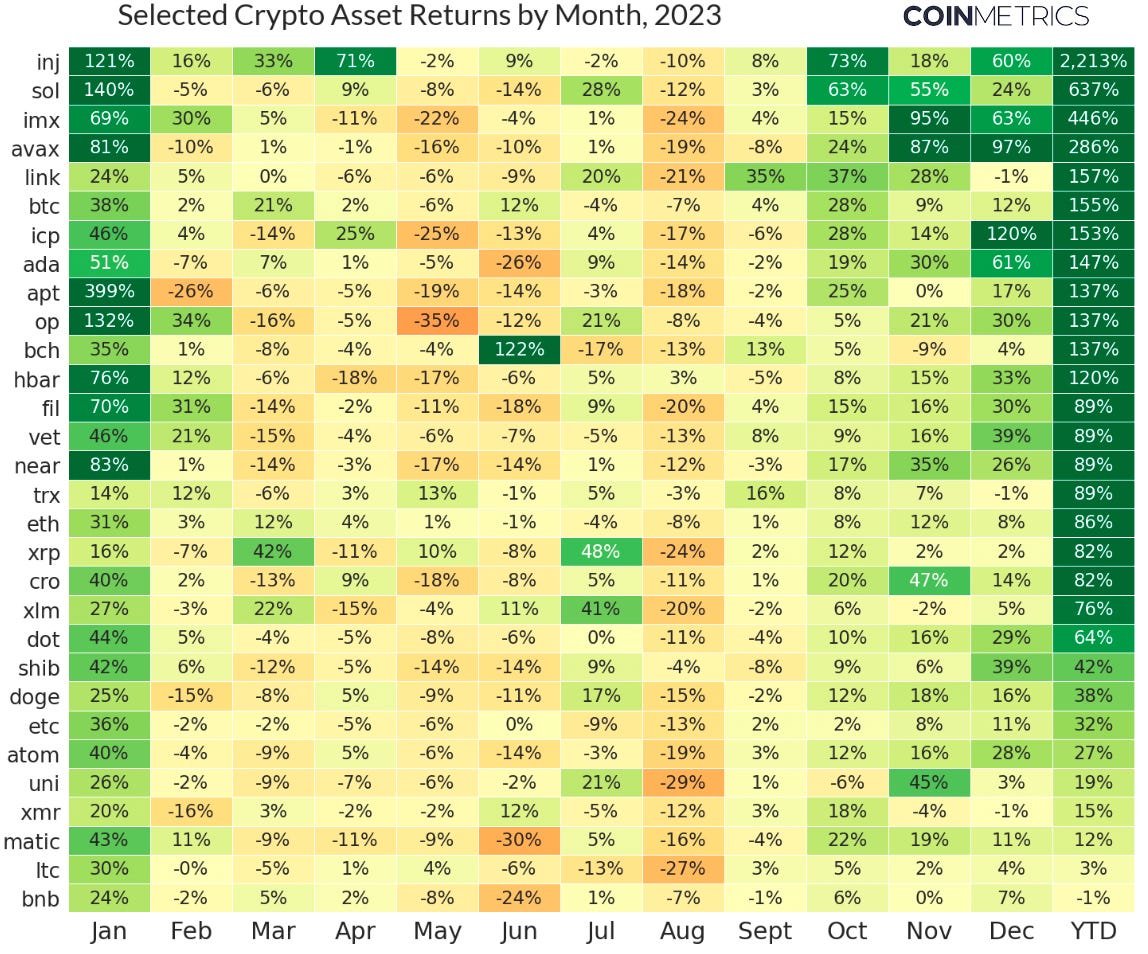

Get the best data-driven crypto insights and analysis every week: State of the Network’s 2023 Year in ReviewBy Kyle Waters & Tanay Ved In this special issue of State of the Network, we revisit the major stories that shaped the digital assets industry in 2023 through a data-driven lens. After a challenging 2022, this past year brought a number of positive developments across the ecosystem, from new institutional entrants to key technical upgrades. While the regulatory environment was arguably the most challenging it has ever been, especially in the US, the new battles should force clarity on a number of outstanding questions. With a period of monetary tightening seemingly coming to an end, both crypto and equities surged in 2023, with many digital assets posting gains above 100%, including bitcoin (BTC), which has risen 150% in 2023. The table below shows the performance of all assets in the datonomyTM universe with a market cap above $1B.

Source: Coin Metrics DatonomyTM and Reference Rates (as of December 17th, 21:00 UTC) Q1: Choke PointThe start of 2023, still shadowed by the FTX collapse, saw a swift turnaround in digital asset markets, with BTC climbing from $16K to $23K in January—a rise that would set the pace for the whole year. A growing sentiment started to emerge that the worst was over, and that FTX's downfall, as a centralized entity, did not tarnish the core principles and potential of public blockchain technology. However, events early in the year also introduced a recurring theme for 2023: escalating regulatory pressure in the United States. A series of enforcement actions in Q1 demanded the digital assets industry's attention, including the SEC's Wells notice to stablecoin operator Paxos over Binance’s stablecoin BUSD, leading to the halting of BUSD issuance. BUSD's supply plummeted from a peak of $16B to $1B over the year, dropping $4B in the week after the notice. The BUSD enforcement marked the beginning of a broader effort from US regulators to rein in offshore exchange giant Binance, the largest exchange by spot volume. In March, the US Commodities Futures Trading Commission (CFTC) unveiled a civil enforcement against Binance and its founder Changpeng Zhao (“CZ”) for numerous alleged regulatory violations. Onshore operators were also subject to new regulatory scrutiny. Many started to face intensifying pressure in Q1, with bank regulators publishing informal guidance documents singling out cryptocurrency and cryptocurrency customers as a risk to the banking system, leading some in the industry to go as far as dubbing the actions “Operation Choke Point 2.0”—an alleged coordinated, government-led campaign to stymie the digital assets industry in the US. Zooming out to the macroeconomic environment, banks began to face a mundane, but troubling situation of devaluing treasury securities amid a rapid increase in interest rates, most notably impacting the tech-friendly Silicon Valley Bank (SVB). SVB’s collapse in March, following a bank run, not only raised concerns about the health of the US banking sector, but also tested the stability of the USDC stablecoin, as Circle had $3.3B of its reserves held at SVB. USDC's price briefly dipped before recovering back to the $1 peg following federal assurances which guaranteed all deposits. The turmoil led to a reshuffling of the $100B+ stablecoin market, with a notable shift from USDC to offshore-issued Tether (USDT). It also marked a growing divergence between Tether and USDC, a trend that would continue in 2023. The banking crisis further impacted crypto asset liquidity by disrupting real-time payment systems like the Silvergate Exchange Network and Signature Bank's Signet, after the two crypto-friendly banks were also shuttered.

Source: Coin Metrics Network Data Pro Despite the challenges, BTC and ETH experienced a rally in the immediate aftermath of the SVB crisis. The core features of digital bearer assets like bitcoin—ease of self-custody, lack of intermediation, and on-chain transparency—became more pronounced than ever, resonating with the original sentiment that led the pseudonymous Satoshi Nakamoto to introduce Bitcoin during the Great Financial Crisis in October 2008. This momentum would carry over to Q2, striking a chord with institutions that began to express greater appreciation for Bitcoin's unique qualities. Q2: The Nine Trillion Dollar ArrivalThe quest for a spot bitcoin ETF in the US has been ongoing since 2013, with the US Securities and Exchange Commission (SEC) consistently rejecting proposals to introduce a spot ETF product to American financial markets. The significance of a spot ETF lies in its potential to offer investors a familiar and potentially more tax-efficient way to include BTC in their brokerage accounts and portfolios. The impact of the first gold ETFs in the early 2000s, like the well-known GLD, is a prime example of what many hope to see with the launch of a bitcoin spot ETF. Despite the SEC's green light for futures-backed bitcoin ETFs in 2021, these products are not ideal for holding long-term due to significant tracking errors to the spot price over time, alongside high expense fees and taxable distributions. But things quickly changed in June of this year when BlackRock, the world's largest asset manager with over $9 trillion in assets under management, filed for the iShares Bitcoin Trust on June 15th. This move instantly injected a renewed legitimacy into the ETF effort, with BlackRock's CEO Larry Fink recognizing bitcoin as a global asset that could “transcend any one currency.” Following BlackRock's bold step, previous applicants, including Fidelity, WisdomTree, Bitwise, VanEck, Invesco, Valkyrie, and ARK, re-entered the race, reigniting the push for a spot bitcoin ETF and signaling a growing institutional appetite for bitcoin and a recognition of its potential role in a diversified portfolio. While Coinbase secured a significant partnership with BlackRock, becoming a key crypto-native ally as BlackRock's chosen custodian in the ETF application, the month of June also saw the SEC launch a landmark case against the leading US exchange. The SEC accused Coinbase of operating as an unregistered securities exchange and labeled various assets, including SOL, MATIC, and ADA, as alleged securities. This action brought the long-standing industry debate about the distinction between crypto securities and commodities into sharp focus. In response, Coinbase swiftly moved to counter the allegations, and the broader industry is now bracing for an outcome that could significantly influence the future trajectory of the digital assets industry in the US. Despite a series of external events both positive and negative, the industry continued to push ahead this year, advancing with key planned upgrades. In April, Ethereum completed its ‘Shapella’ hard fork, which activated withdrawals of staked ether (ETH) and validators’ accumulated staking rewards. The success of the upgrade eliminated previous liquidity risks associated with staking, and immediately enticed a new surge of staking deposits, a trend that would continue throughout most of 2023. Even as the staking APR currently hovers around 4%, staked ETH has hit 28M, or just under one quarter of the entire ETH supply. The upgrade brought much-needed assurances to Ethereum validators staking their ETH, as the last leg of a years-long process to move Ethereum from a proof-of-work to proof-of-stake system, mostly accomplished via The Merge, was completed without issue. With issuance falling 90% after The Merge, 2023 also marked the first full year in which Ethereum’s supply declined, after taking into account fee burning.

Source: Coin Metrics Labs Q3: Order in the CourtsThe second half of 2023 brought a reinforcing shift, with significant legal victories and the re-engagement of institutions providing a counterbalance to the regulatory pressures of earlier months. Notably, Ripple’s triumph in its protracted legal battle against the SEC marked a cornerstone event. The US District Court issued a partial summary judgment on July 13th , establishing that secondary sales of XRP on exchanges did not constitute securities transactions. This ruling not only vindicated Ripple but also set a precedent that challenged the SEC’s approach in classifying digital assets, reverberating across the industry and influencing the regulatory treatment for other digital assets alleged as securities under the regulators purview.

Source: Coin Metrics Institutional Metrics Parallel to this legal watershed, Grayscale’s win against the SEC marked another important turning point. The case centered around Grayscale’s bid to convert its Bitcoin Trust (GBTC) into a spot bitcoin ETF, which the SEC initially rejected. However, on August 29th, the Court of Appeals overturned this decision, deeming that its denial was “arbitrary and capricious” highlighting the SEC’s inconsistent treatment of similar products, especially given the existence of Bitcoin futures ETFs. This victory significantly fueled market-wide anticipation around the launch of bitcoin spot ETFs, a sentiment reflected in the narrowing of GBTC’s discount to its net asset value (NAV) from -40% to -10%. These regulatory milestones hinted at a moderation to this SEC administration's approach to crypto regulation, paving the way for broader access and a phase of maturation for the asset class. Concurrently, this shift emphasized the need for clearer regulations, especially as more dynamic regulatory environments offshore spurred activity in markets like the UAE, Hong Kong, EU, and UK.

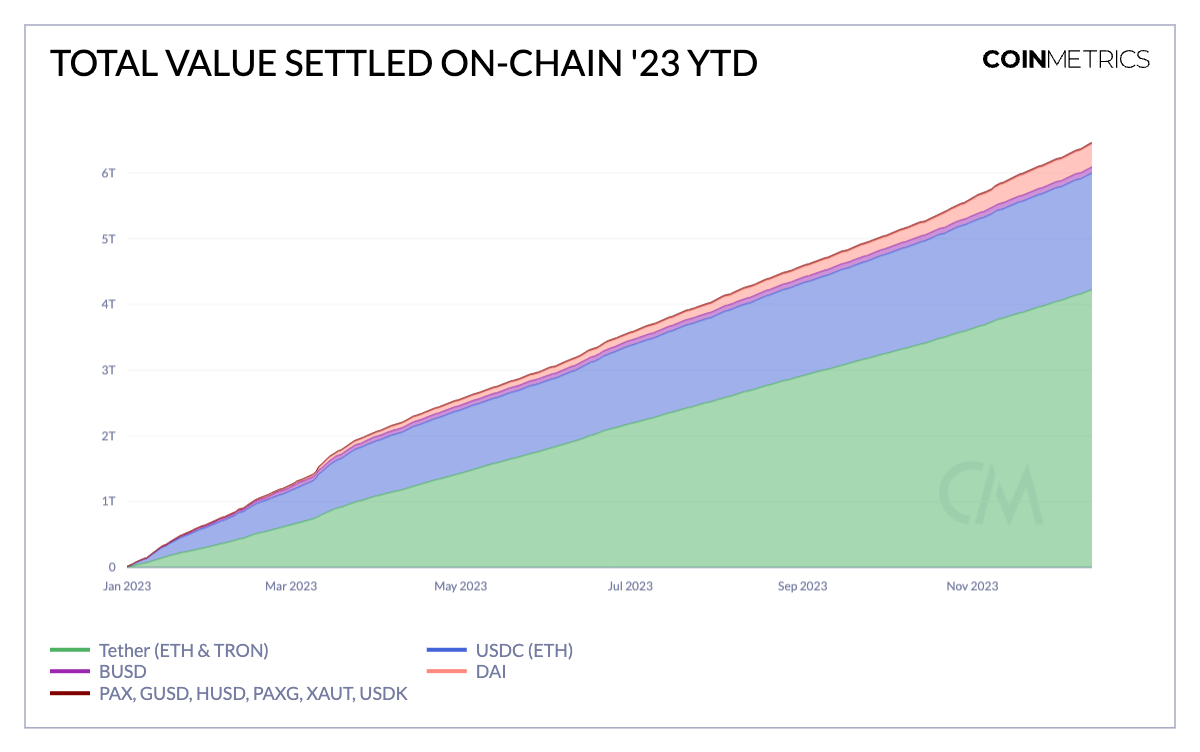

Source: Coin Metrics Network Data Pro New product launches also added to the excitement, particularly invigorating discussions about stablecoins, a key theme throughout 2023. Payments giants like PayPal and Visa entered the fray with the former launching PayPal USD (PYUSD) on the Ethereum blockchain and the latter ramping up stablecoin settlement initiatives. The launch of the Federal Reserve's instant payments system, FedNow, also re-ignited the discourse around its potential impact on the current stablecoin landscape, and the direction of the central bank’s digital currency initiatives. However, FedNow’s domestic reach emphasizes the value proposition of stablecoins, which serve as a global medium of exchange, facilitating cross-border payments and bridging the on-chain and off-chain economy. This tangible impact is evident in the chart above, with the largest fiat-backed stablecoins USDT and USDC settling $4.2 trillion and $1.7 trillion respectively. These developments, along with new entrants such as protocol-native stablecoins and interest-bearing stablecoins portray the growing diversity and evolving role of stablecoins in the broader financial ecosystem. Outside of the stablecoin landscape the launch of Coinbase’s layer-2 network, Base, garnered significant attention and sparked a wave of activity on emerging applications on the platform. This marked a pivotal step in the proliferation of layer-2 solutions, especially in the context of Ethereum’s upcoming EIP-4844 upgrade, aimed at enhancing network scalability. Despite broader challenges from a tightened financial environment and sector specific events like smart contract exploits as experienced by Curve Finance, the quarter presented a significant foundation for future growth. Q4: De-iced and Ready for TakeoffA revitalization in digital asset markets unfolded in Q4 as BTC surged over 50%, marking a resurgence in market sentiment and valuations. This rebound was driven by heightened institutional interest, as reflected in the near-record levels (over $5 billion) in BTC futures open interest on the Chicago Mercantile Exchange (CME), a venue preferred by institutional participants. This offered clearer evidence of Bitcoin’s evolving market structure, as investors actively positioned themselves in anticipation of a spot bitcoin ETF and the next Bitcoin halving. Accompanying this surge in derivatives market activity, spot volumes escalated to yearly highs. Supply trends also reinforced a bullish outlook, with free float supply hitting the lowest levels since March 2017, and only 30% of BTC moving in the past year, indicating a strong holder base. The rally broadened beyond Bitcoin in a cyclical fashion, buoying other sectors of the crypto ecosystem. Grayscale’s Trust products saw a significant reduction in discounts and, in some cases, achieved impressive premiums with the likes of GSOL and GLINK trading at premiums of 869% and 250% respectively in November. Alternative layer-1 blockchains also experienced a robust recovery, with Solana (SOL) emerging as a standout as it dissociated from prior FTX related affiliations. An engaged community, growing ecosystem of applications and infrastructure on the network reinforced Solana’s credibility as a layer-1 platform and ignited conversations around the proliferation of monolithic blockchains amid a growing sea of modular blockchains and layer-2 networks. The surge was not only contained to valuations. On-chain activity also rebounded with a heightened fee market on both the Bitcoin and Ethereum networks, while stablecoin supply turned positive after a period of decline, pointing to signs of returning liquidity. Building on the thread of prior affiliations, the trial culminating in the conviction of Sam Bankman Fried (SBF), brought a definitive end to the industry’s most tumultuous episodes with FTX’s downfall. Simultaneously, Binance’s settlement, involving a $4 billion fine and the stepping down of Changpeng Zhao (CZ), resolved long-standing allegations surrounding the largest exchange. Another announcement of significance which went under the radar was the Financial Accounting Standard Board’s (FASB) changes to crypto accounting standards. This update will allow corporations that hold digital assets on their balance sheet to recognize assets at “fair value” rather than treating them as intangibles, reducing the frictions faced by such firms currently, while incentivizing more ownership. For example, this will enable Microstrategy (MSTR), a public company holding over 17,500 BTC, to realize profits or losses on their balance sheet in accordance with the measurement period. These developments collectively closed a chapter of uncertainty that clouded the industry, paving the way for a more mature and optimistic future for the asset class.

Source: Coin Metrics Reference Rates, Indexes & Google Finance (Click for larger view) Amid a backdrop of decade-high inflation, financial tightening and rising geopolitical tensions, digital asset markets have grappled with significant macroeconomic challenges. However, stakeholders have navigated these complexities adeptly, leading to growth in new sectors such as tokenized treasuries and real-world assets (RWA’s). The strength in digital assets is evident when we look back at returns by major asset classes in the investable universe over 2023. The outperformance of crypto-related equities and digital assets shines through, with Coinbase (COIN) a major beneficiary of the market rebound. As macroeconomic tides potentially undergo a shift over the coming months, the digital asset industry is primed for a phase of maturation and expansion. Coin Metrics Research in 2023We released a number of special reports in 2023, be sure to find them all here: https://coinmetrics.io/insights/special-insights/

Also be sure to check out our 150th issue of State of the Market, where we provide an overview of crypto market activity from December 7th - December 13th, 2023. As always, if you have any feedback or requests please let us know here. Subscribe and Past IssuesCoin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data. If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here. © 2023 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is” and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.

|

Older messages

State of the Network’s Q4 2023 Mining Data Special

Tuesday, December 12, 2023

Coin Metrics' State of the Network: Issue 237

State of Stablecoins: Signs of Returning Liquidity

Tuesday, December 5, 2023

Coin Metrics' State of the Network: Issue 236

Dollar-Cost Averaging Portfolio

Tuesday, November 28, 2023

Coin Metrics' State of the Network: Issue 235

Checking On-Chain Indicators for Green Shoots in the Digital Assets Market

Tuesday, November 21, 2023

Coin Metrics' State of the Network: Issue 234

Coin Metrics’ State of the Network: Issue 233

Tuesday, November 14, 2023

November Rally Reaches New Corners of the Digital Asset Market

You Might Also Like

Central African Republic’s CAR memecoin raises scrutiny

Friday, February 14, 2025

Allegations of deepfake videos and opaque token distribution cast doubts on CAR's ambitious memecoin project. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

January CEX Data Report: Significant Declines in Trading Volume Across Major CEXs, Spot Down 25%, Derivatives Down…

Friday, February 14, 2025

According to data collected by the WuBlockchain team, spot trading volume on major central exchanges in January 2025 decreased by 25% compared to December 2024. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Previewing Coinbase Q4 2024 Earnings

Friday, February 14, 2025

Estimating Coinbase's Transaction and Subscriptions & Services Revenue in Q4 2024 ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

ADA outperforms Bitcoin as Grayscale seeks approval for first US Cardano ETF in SEC filing

Friday, February 14, 2025

Grayscale's Cardano ETF filing could reshape ADA's market position amid regulatory uncertainty ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

AI project trading tips: investment targets and position management

Friday, February 14, 2025

This interview delves into the investment trends, market landscape, and future opportunities within AI Agent projects. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

DeFi & L1L2 Weekly — 📈 Polymarket recorded a new high of 462.6k active users in Jan despite volume dip; Holesky a…

Friday, February 14, 2025

Polymarket recorded a new high of 462600 active users in January despite volume dip; Holesky and Sepolia testnets are scheduled to fork in Feb and Mar for Ethereum's Pectra upgrade. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

DeFi & L1L2 Weekly — 📈 Polymarket recorded a new high of 462.6k active users in Jan despite volume dip; Holesky a…

Friday, February 14, 2025

Polymarket recorded a new high of 462600 active users in January despite volume dip; Holesky and Sepolia testnets are scheduled to fork in Feb and Mar for Ethereum's Pectra upgrade. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Donald Trump taps crypto advocate a16z’s Brian Quintenz for CFTC leadership

Friday, February 14, 2025

Industry leaders back Brian Quintenz's nomination, highlighting his past efforts at the CFTC and potential to revamp crypto oversight. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

⚡10 Tips to Make a Living Selling Info Products

Friday, February 14, 2025

PLUS: the best links, events, and jokes of the week → ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Interview with CryptoD: How He Made $17 Million Profit on TRUMP Coin

Friday, February 14, 2025

Author | WUblockchain, Foresight News ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏