State of Stablecoins: Sector Expansion & A Changing Interest-Rate Environment

State of Stablecoins: Sector Expansion & A Changing Interest-Rate EnvironmentStablecoin growth, diversity in collateralization & implications of a changing interest-rate environment

Get the best data-driven crypto insights and analysis every week: State of Stablecoins: Sector Expansion & A Changing Interest-Rate EnvironmentBy: Tanay Ved Thanks for reading Coin Metrics' State of the Network! Subscribe for free to receive new posts and support my work. Key Takeaways:

IntroductionIn this issue of Coin Metrics’ State of the Network, we explore the diverse stablecoin landscape, focusing on peg mechanisms, approaches collateral composition, and sources of yield amid a changing interest-rate environment. Stablecoin Supply Pushes Towards New HighsAfter a period of consolidation in Q2, aggregate stablecoin supply has trended positive in August—suggesting an environment with increased liquidity and potential for capital flows into the ecosystem. This is reflected in the chart below, illustrating the monthly change in stablecoin supply.

Source: Coin Metrics Network Data Pro As a result, near 161B, the aggregate supply of stablecoins is once again approaching record-highs. Tether mantains a market share greater than 70%, with USDT on Ethereum (+28%) and Tron (+26%) growing over the year to a total supply of $119B across networks including Solana and Avalanche. Meanwhile, Circle’s USDC supply has grown to ~$34B as it proliferates across Solana and Ethereum layer-2’s like Base. While DAI has trended lower towards $3.1B, the tokenized version of DAI deposited into Maker’s Dai Savings Rate, sDAI (savings DAI), has grown to $1.34B. Newer stablecoin entrants have also gained traction: First Digital USD (FDUSD) on Ethereum grew by 56% in August to reach $3.07B, while Ethena’s USDe ($2.96B) and sUSDe ($1.16B) hit a combined total of $4.12B. Notably, PayPal’s PYUSD has seen rapid growth on Solana, surpassing its Ethereum supply of $364M to reach a $1B total.

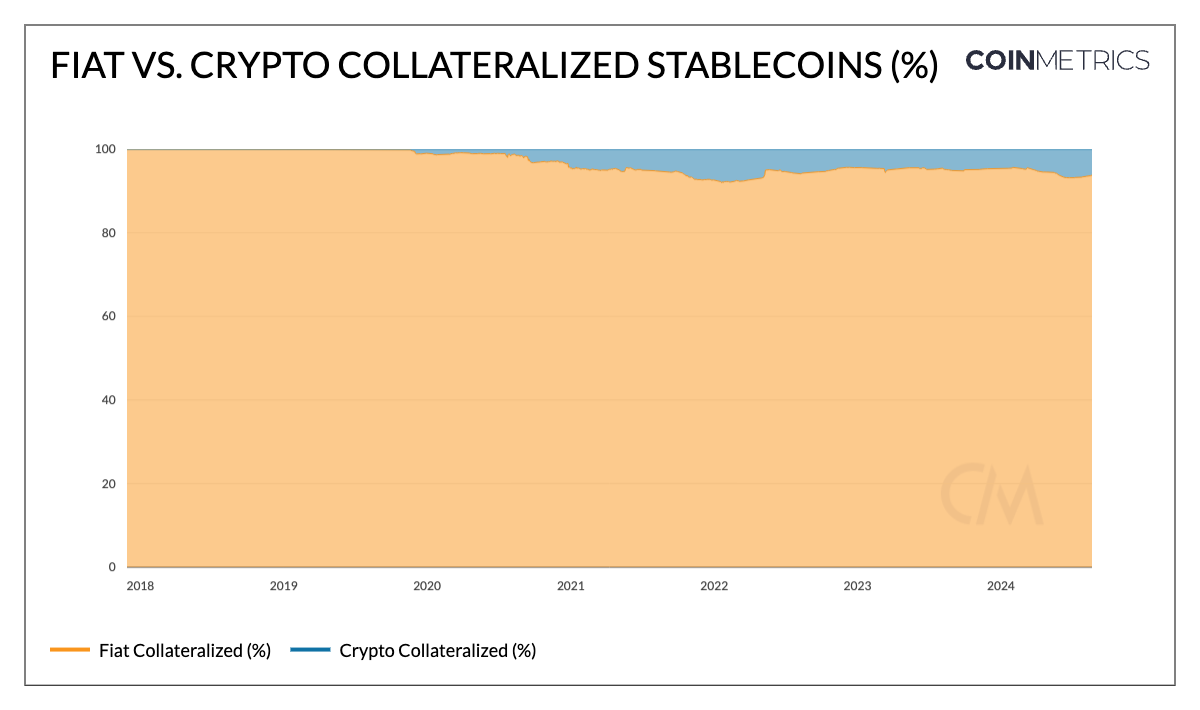

Source: Coin Metrics Network Data Pro Competing For AdoptionDiversity in CollateralizationTo improve utility as a store of value, a variety of asset composition or collateralization approaches have arisen in the stablecoin ecosystem, influencing the risk profile, operational characteristics and regulatory outlook of these products. More than 90% of outstanding stablecoin supply consists of those collateralized by fiat currencies, such as Circle’s USDC, Tether’s USDT and PayPal’s PYUSD, backed by the US Dollar and cash-equivalents assets, tying their stability to the traditional financial system. Others, like MakerDAO’s DAI and sDAI, provide an alternative to traditional units of account, backed by a portfolio of crypto-assets and real-world assets (RWAs) like private credit loans or treasuries. 45% of Dai is backed by crypto-assets, while 40% is collateralized by RWAs.

Source: Coin Metrics Network Data Pro Alternative Units of AccountAs a result of the US Dollar’s status as the global reserve currency and ubiquitous demand in emerging markets, the supply of USD-pegged stablecoins far exceeds alternative units of account. However, not all stablecoins are pegged to the U.S. dollar. With the European Union’s progress on regulating digital assets through Markets in Cryptoassets (MiCA) Regulations, Euro-backed stablecoins have seen a boost in adoption. With a current supply of ~40M, Circle’s EURC is the only Euro-pegged stablecoin compliant to MiCA regulations. As more institutions deploy alternative pegged assets such as Société Générale’s EURCV wholesale stablecoin, alternative pegs may enable forex markets to expand leveraging on-chain infrastructure. As different jurisdictions develop their regulatory frameworks for digital assets, stablecoins pegged to local currencies can facilitate transactions for individuals and businesses within and across regional economies, while complying with regulatory requirements.

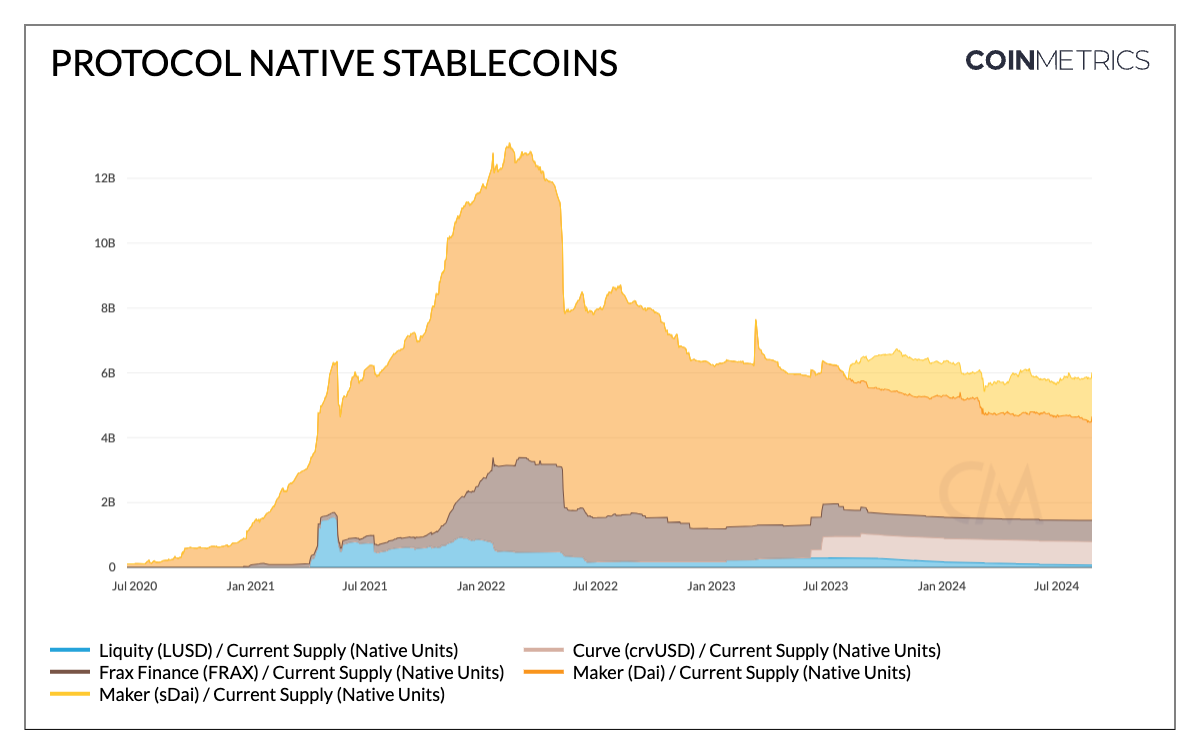

Source: Coin Metrics Network Data Pro Decentralized Finance (DeFi) Utility & ExpansionStablecoins have become synergistic to the business models and functionality of decentralized finance (DeFi) protocols. Following Maker's success with DAI, many DeFi protocols have launched their own native stablecoins tailored to their ecosystems. Money market protocols like Aave (GHO), DEXs like Curve Finance (crvUSD) and collateralized-debt protocols (CDPs) like Maker & SparkLend (DAI) and Liquity (LUSD) feature native stablecoins, with mechanisms for maintaining price stability and aiding operations within their respective ecosystems. They facilitate a wide range of financial services like payments, borrowing, trading, liquidity provision and yield strategies. A significant portion of traditional stablecoin supply also resides in Ethereum smart contracts: 27% of USDC, 20% of USDT, and notably, over 50% of PYUSD —serving as stable collateral on lending protocols and quote pairs on decentralized exchanges (DEXs). Furthermore, with the proliferation of tokenized treasuries and real-world assets (RWAs) like BlackRock’s BUIDL and Mountain Protocols USDM, DeFi protocols are beginning to incorporate traditional financial assets into their ecosystems, bridging the gap between DeFi and TradFi.

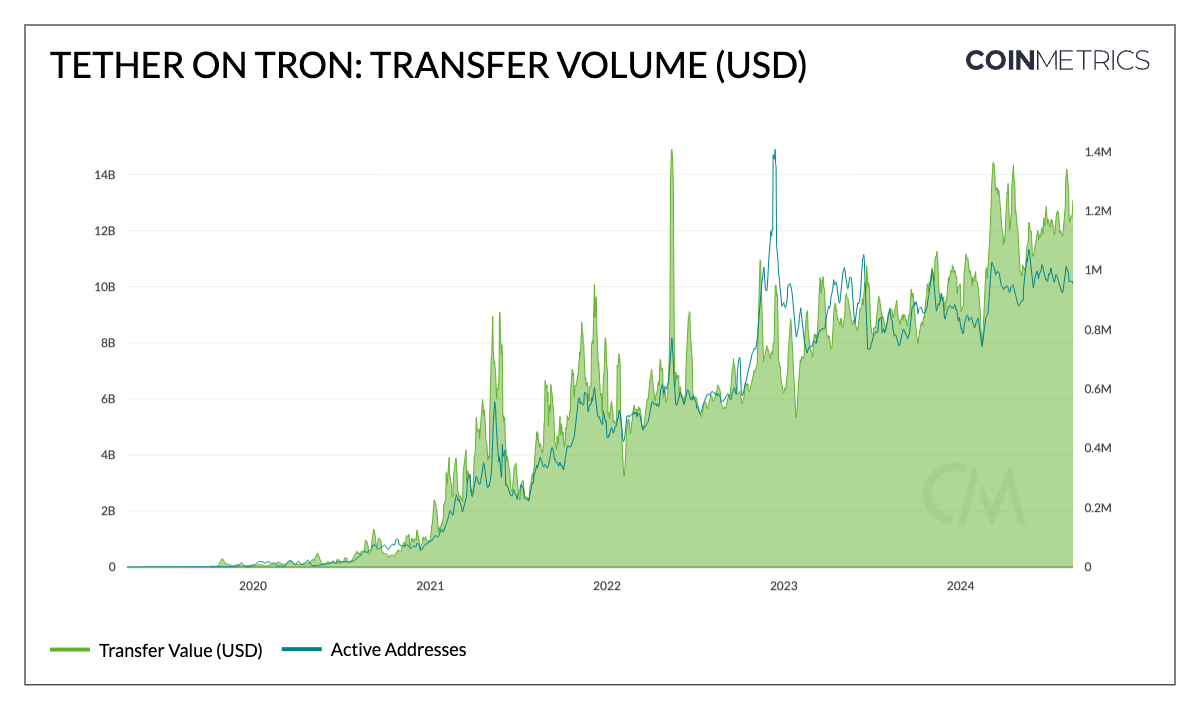

Source: Coin Metrics Network Data Pro Product Market Fit: Tether on TronTether (USDT) on the Tron network is a prime example of a stablecoin that has established a product-market fit. It has displayed strong adoption and usage as a medium of exchange and store of value across a range of metrics. Not only does it boast the largest current supply of 118B with ~61B on Tron and ~53B on Ethereum (in addition to Solana & Avalanche), but records the highest transfer volumes and counts relative to other stablecoins. Tether’s (adjusted) transfer volume on Tron is nearing a record $14B, with close to 1M active addresses. This usage is propelled by a combination of Tron's low transaction fees, enabling lower value payments and remittances with low median transfer sizes and USDTs deep liquidity across exchanges, facilitating transactional activities as a quote-asset. Therefore, it provides the means to protect savings, seek economic stability and democratizes access to banking infrastructure, enabling peer-to-peer transactions of various purposes—especially in emerging markets.

Source: Coin Metrics Network Data Pro Low fees on networks like Solana and Ethereum layer-2s, combined with the distribution of businesses like Coinbase and easier onboarding through smart-wallets or point of sale systems, offer an opportunity for stablecoins to establish a strong base across these networks and around the globe. Stablecoins In A Changing Interest-Rate EnvironmentStablecoins are primarily collateralized by U.S Dollars or equivalents like cash or treasury bills. Most traditional stablecoins (e.g., USDT, USDC, PYUSD) retain interest earned on their collateral rather than passing it to token-holders. Tether's Q2 attestation exemplifies this, reporting $5.4B in profits partly from direct and indirect ownership of U.S. Treasury holdings, which reached a new high of $97.6B. This brought their exposure to treasuries above Germany, the United Arab Emirates, and Australia—ranking 18th out of countries holding U.S debt.

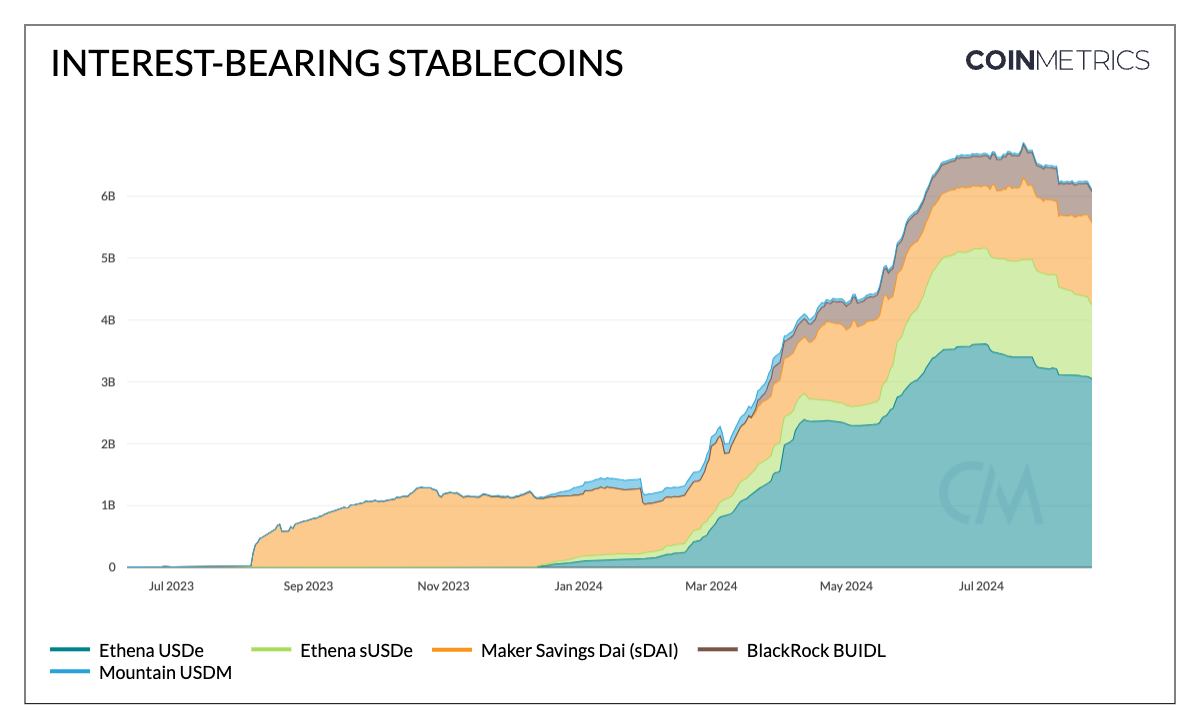

Source: Tether & Circle Attestations Where Does the Yield Come From?However, the post-2021 rise in federal funds and global interest rates introduced an opportunity cost for pure U.S. dollar exposure. This sparked the emergence of interest-bearing stablecoins, collateralized by short-term U.S. treasury bills, money market instruments, and other real-world assets (RWAs), which passed yield to holders. Mountain Protocol's USDM, for instance, derives its yield from a reserve composition of treasury bills, accruing interest through a rebasing mechanism. Maker protocol's savings DAI (sDAI), takes another approach, accumulating interest from DAI deposited in the DAI Savings Rate (DSR). This yield originates from a basket of real-world assets (RWAs), crypto-assets, and excess reserves backing DAI, implemented through an ERC-4626 vault standard. These products essentially function as crypto savings accounts. The integration of RWAs with public blockchains has also paved the way for institutional-grade offerings like BlackRock's BUIDL, a tokenized money market fund issued by Securitize that utilizes a USDC redemption fund to provide a continuous, 24/7 offramp into stablecoins. While tokenized treasury products rely on such off-chain sources of yield, others like Ethena’s USDe generates yield through a basis trade involving delta-neutral hedging (long position in staked ETH or other collateral and a corresponding short position in perpetual futures contracts.)

Source: Coin Metrics Network Data Pro However, Federal Reserve Chair Jerome Powell's suggestion of interest rate cuts at the 2024 Jackson Hole symposium raises questions about stablecoins in a low interest-rate environment. While fiat collateralized stablecoin issuers may see reduced profitability due to the interest-rate sensitivity of their business models and yield-bearing stablecoins might lose some of their appeal due to diminishing returns, a risk-on environment could bring new capital inflows to the crypto ecosystem. This influx, driven by investors seeking to capitalize on lower borrowing costs and higher asset valuations, could potentially offset these effects through increased demand for stablecoins as a medium of exchange. ConclusionThe recent growth in stablecoin supply, pushing towards new highs, signals increasing liquidity and capital availability in the crypto ecosystem. As the landscape continues to evolve, we're witnessing stablecoins optimizing for different use cases and risk profiles with diverse collateralization methods from RWAs to crypto-assets and innovative approaches like the tokenized basis trade. As we look ahead, navigating regulatory hurdles and a low interest-rate environment introduces both opportunities and challenges, potentially reshaping business models, user preferences and the overall competitive landscape of this burgeoning sector. Coin Metrics UpdatesThis quarter’s updates from the Coin Metrics team:

Subscribe and Past IssuesAs always, if you have any feedback or requests please let us know here. Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data. If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here. © 2024 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is” and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.

|

Older messages

Unwrapping Wrapped Assets & wBTC

Tuesday, August 20, 2024

Wrapped Bitcoin (wBTC) custody transition, business model and implications in DeFi ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Futures Falter, Funding Flips

Tuesday, August 13, 2024

Stability of Decentralized Finance ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

An Update on Crypto Markets & Coinbase Q2 2024 Earnings

Tuesday, August 6, 2024

Analyzing recent events gripping crypto markets and Coinbase Q2 2024 earnings ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The Story of Ethereum Staking So Far

Tuesday, July 30, 2024

Uncovering Ethereum's staking ecosystem, from "The Merge" to "Shapella", the rise of liquid staking tokens (LSTs) and beyond ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

The Launch of Ether ETFs

Tuesday, July 23, 2024

A look into ETH ETF fees, Grayscale funds and demand & supply dynamics heading into Ether ETF Launch ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

You Might Also Like

Central African Republic’s CAR memecoin raises scrutiny

Friday, February 14, 2025

Allegations of deepfake videos and opaque token distribution cast doubts on CAR's ambitious memecoin project. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

January CEX Data Report: Significant Declines in Trading Volume Across Major CEXs, Spot Down 25%, Derivatives Down…

Friday, February 14, 2025

According to data collected by the WuBlockchain team, spot trading volume on major central exchanges in January 2025 decreased by 25% compared to December 2024. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Previewing Coinbase Q4 2024 Earnings

Friday, February 14, 2025

Estimating Coinbase's Transaction and Subscriptions & Services Revenue in Q4 2024 ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

ADA outperforms Bitcoin as Grayscale seeks approval for first US Cardano ETF in SEC filing

Friday, February 14, 2025

Grayscale's Cardano ETF filing could reshape ADA's market position amid regulatory uncertainty ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

AI project trading tips: investment targets and position management

Friday, February 14, 2025

This interview delves into the investment trends, market landscape, and future opportunities within AI Agent projects. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

DeFi & L1L2 Weekly — 📈 Polymarket recorded a new high of 462.6k active users in Jan despite volume dip; Holesky a…

Friday, February 14, 2025

Polymarket recorded a new high of 462600 active users in January despite volume dip; Holesky and Sepolia testnets are scheduled to fork in Feb and Mar for Ethereum's Pectra upgrade. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

DeFi & L1L2 Weekly — 📈 Polymarket recorded a new high of 462.6k active users in Jan despite volume dip; Holesky a…

Friday, February 14, 2025

Polymarket recorded a new high of 462600 active users in January despite volume dip; Holesky and Sepolia testnets are scheduled to fork in Feb and Mar for Ethereum's Pectra upgrade. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Donald Trump taps crypto advocate a16z’s Brian Quintenz for CFTC leadership

Friday, February 14, 2025

Industry leaders back Brian Quintenz's nomination, highlighting his past efforts at the CFTC and potential to revamp crypto oversight. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

⚡10 Tips to Make a Living Selling Info Products

Friday, February 14, 2025

PLUS: the best links, events, and jokes of the week → ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Interview with CryptoD: How He Made $17 Million Profit on TRUMP Coin

Friday, February 14, 2025

Author | WUblockchain, Foresight News ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏