So leading SaaS growth stage VC fund Insight Partners surveyed 100+ of its top later-stage B2B companies to see how they did marketing and demand gen and pipeline creation in particular.

What they learned:

- Marketing drives 48% of pipeline across B2B companies. Sales drives 33%. And Partners and Channel 15%. An interesting break-down. Not a shocker but useful to see this across 100+ leading B2B scale-ups. See above.

- 70% of pipeline for marketing comes from events, search both paid and free, and social. That’s it. SEO is undergoing the biggest change, but it’s still in the Big 4 Here.

- SEO is under stress today from GenAI and changes at Google, but is still the second-highest driver of pipeline after events. SEO may not be the same, but is still works. If you adapt. Like outbound.

One thing that really jumps out is the mismatch today on energy into events vs the ROI. You can see here how events and trade shows are what helped put Datadog on the map.

|

|

|

SF Bay Area, May 13-15, 2025 |

|

|

We held a SaaStr Annual executive de-brief to share some of the last Annual data and trends we saw across all 100+ sponsors and 10,000 attendees of last SaaStr Annual. A lot of this proprietary data is I think too good not to share, and maybe help even give you a gauge on where at least some of your compatriots in B2B trended for an event at this scale.

It’s not too late to sponsor SaaStr Annual 2025 — May 13-15 in SF Bay — but it’s getting close to too late!

|

|

|

There are a lot of posts about how VCs make a ton of money with liquidation preferences when founders make zero.

I find that’s rarely true. There are cases — 100% for sure.

The way in theory a “liquidation preference” works is the VCs get their money out first in a deal, and sometimes, they get it out first and then they get out their pro-rata stake.

So yes in theory, if you sell for less than you raise in VC money, the VCs in theory would get it all back, and the common stock and founders nothing. But like so many things … it’s not that simple:

- First, even if a startup sells for say $20m after raising $50m and ev even if the VCs were able to keep all that $20m, that’s still a big loss.

- More importantly, when an acquirer goes to buy a company, they almost always want the founders to stay and go big. Departed founders, that’s different. But they almost always want as much consideration as possible to go to the founders and top execs still there — and NOT the VCs.

In fact, in my worst investments so far in 11 years of investing, the founders made $20m+ and the VCs lost most of their money. The opposite of this narrative.

|

|

|

At a manager level, my #1 red flag is if they don’t quickly move to integrate the team they inherit. Because this something totally actionable, immediately. No matter what the facts on the ground.

This is different than changing things up, or even deciding who to keep.

But true managers always at least try to integrate with the team they inherit on Day 1, or at least half-way through Week 1.

- If you hire a new VP and you see legacy folks on his/her team excluded in the first week, not invited to things, cut out of the loop … that’s a flag.

- If you see one part of the team that the new VP hasn’t even reached out to in their first few days, say the SMB team or the European team … that’s a flag.

Of someone not quite yet seasoned enough to be a true VP.

You have to go to battle with the team you have. The best managers know this. Yes, you can change the team and usually should at least evolve it — but not on Day 1.

|

|

|

This edition of the SaaStr Daily is sponsored in part by Prismatic

|

An integration is so much more than it first appears. Even though your engineers are capable of building your them, is the effort worth the cost?

|

|

|

It’s a weird thing, but some of the worst fundraising advice comes from … your existing investors.

Why? It’s usually not wrong, it’s just often, so, so biased:

- Accelerators view VCs as fungible. They often tell you to raise at the highest price irrespective of investor quality or ability to support the company later. Is this the right advice?

- Seed investors worry about dilution. Their check sizes are relatively small. But dilution is often the price of scaling.

- Series A and B investors want to “control the ball” and decide who invests more. So they don’t always want to let new folks in on the cap table. Is this best for the company?

- VCs with lots of money to deploy often want you to raise a lot more if you are doing well — even if you don’t need it. They are biased in favor of overloading you with capital. Sometimes. But not all the time.

- VCs with no more money to deploy often advise you not to raise more — even if it might help. They are biased in favor of keeping lean. Sometimes that’s the right call. But is it always?

Growth investors want to manage downside risk. If you invest at a $1B valuation, you worry about the downside. If you got in at $10m? Maybe less so.

You can even get conflicting advice from VCs in the exact same board meeting. You might hear keep the burn rate low, but if they also want to increase your ownership, they may push for you to raise more from the insiders … at the exact same board meeting. Which is it? Spend less? Or spend more?

The biases creep up in many places: What terms are fair? How much should you raise? When?

I recently coached a founder of a rocketship raising the capital they needed at a $700m valuation where the seed investors told them to turn down all the term sheets they got because of a liquidation preference. Was this right for the company? Or right for the seed investors? Or even right for anyone? Just an example.

Yes, get tons of fundraising advice from your existing VCs and investors. They all have great experience.

Just realize 100% of it will be … biased.

|

|

|

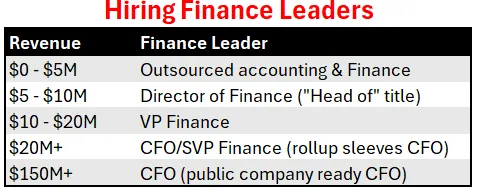

A topic I find founders get a bit or often a lot wrong is … When To Hire Your First CFO. We’ve got a guest post below from OnlyCFO on this very topic! If I had to summarize all my learnings, it’s that you can’t really hire a full-time head of finance too early, but many of us go to hire a “CFO” around $10m-$30m ARR, when we really need a VP/SVP of Finance. Per OnlyCFO’s point below. And I’d even bring someone full-time in as early as $1m-$2m ARR if you can find someone great. Especially once the renewal cycle heats up and once you have a ton of customers to invoice. That has saved my bacon several times. — jason, ed.

We all know that hiring the right people is critical for success, but what folks often forget is that it’s hiring the right people AND hiring them at the right time.

I have seen LOTS of companies fail at one or both of these when hiring for a finance leader. The right person to lead finance at a Series A company looks very different than the right person to lead finance at a true pre-IPO company (that is near an IPO).

|

|

|

This edition of the SaaStr Weekly is sponsored in part by Stripe

|

We've partnered with Stripe to give you access to the internet economy conference. Stripe Sessions brings together the payments and financial technology community to share ideas that drive progress.

|

|

|

There is one common factor, that founders know, but often lose track of in their pitch: every VC, at any stage, is looking for outliers. No matter the price or how early or late.

Your pitch, your team, your metrics, your market position, your vision, your TAM, your everything, should honestly and transparently but aggressively and positively show how you can be an outlier.

It is hard to make money as a VC, as odd as that may sound. You generally need several unicorns per fund, and 1 per year, to truly do well.

Now, VCs have a benefit in that not every single investment has to be a unicorn. They do have the benefit of a portfolio approach, which founders don’t. But 1 or more from each “batch”, from each, fund, does need to be to do extremely well. Far more than just 1 for a bigger fund.

The risk VCs try to take is that some signals of a potential unicorn are there. And then, they are OK if it doesn’t always pan out. They have 10–20 bets or more per fund, after all.

|

|

|

Closing your first B2B deals is about hustle, persistence, and creating urgency where there often really isn’t any. Early on, you’re not just selling your product—you’re selling yourself, your vision, and the idea that your product is going to solve a real pain point right now.

Here’s how to at least increase urgency in deals:

- Start with Warm Leads. Even If The Deals Are Small.

Your first customers are almost always people you already know or who are one degree removed. Reach out to your network, past colleagues, or anyone who might have a problem your product solves. These early customers are buying into you as much as the product. If you don’t have a network in your target market, hustle to build one—attend events, cold email, or leverage LinkedIn.

- Focus on the True Pain Point, Not Buzzwords

No one buys a B2B product just because it’s part of a trend — not on its own, at least. They buy because it solves a real, material problem that’s costing them time, money, or both. Be laser-focused on the pain point you’re solving. If you can quantify the ROI—how much time or money they’ll save—that’s even better. For example, if your product saves them $50K a year, that’s a compelling reason to act now.

- Create Urgency by Adding Value. For Real.

Urgency doesn’t just happen. You have to create it. The best way to do this is by adding so much value during the sales process that the prospect feels like they’re losing out by waiting. This could mean offering a free trial, doing a pilot, or even helping them solve part of their problem manually to prove your value. If you’ve already helped them, they’re more likely to move forward quickly.

- Use Deadlines — But Thoughtfully.

Deadlines can work, but they have to feel natural. For example, you could offer a discount or extra services if they sign by the end of the month. But don’t overdo it—if it feels like a used car sales tactic, it’ll backfire. Instead, tie the deadline to something real, like a limited capacity for pilots or onboarding slots 78.

- Always Get the Next Step on the Calendar.

After every meeting or call, schedule the next step before you hang up. Whether it’s another demo, a discussion with their team, or a follow-up to review the proposal, always have something on the books. This keeps the momentum going and prevents deals from stalling 7.

- Ask for the Close — Once You’ve Added a Ton Of Value. Ask.

This sounds obvious, but a lot of founders don’t do it. Once you’ve added value and addressed their concerns, ask directly: “Can we get this done by [specific date]?” If you’ve done your job well, they’ll often say yes. And if they don’t, you’ll at least learn what’s holding them back so you can address it.

- Leverage Social Proof.

Even if you don’t have paying customers yet, you can still use social proof. Talk about beta users, testimonials, or even just the interest you’ve received. People want to buy what others are buying. If you can show that others are excited about your product, it’ll create FOMO and urgency.

- Be Persistent Without Being Annoying.

Follow up regularly, but always add value in your follow-ups. Share a case study, a new feature, or an insight that’s relevant to their business. If you’re just pestering them to “check in,” you’re not helping your case.

- Share How Competitors And Similar Customers Are Using Your Product.

This always helps. It shows how others are getting ahead using your product. But it has to be for real, with real details of true results.

- Your first deals are generally going to take longer and be harder than you expect, but that’s normal. Once you close a few, you’ll have the momentum and proof points to make the next ones easier.

|

|

|

Nick Mehta is the CEO of Gainsight, the customer success platform that helps businesses deliver value to customers and drive scalable growth.

Over the past 12 years, Nick has met with more than 5,000 companies and hundreds of investors, becoming one of the foremost authorities on customer success strategies.

|

|

|

The Official SaaStr Podcast |

|

|

|

New Episodes of the SaaStr Podcast with, Gainsight, SaaStr, Founder Collective and More!

|

-

SaaStr 794: The Top 10 Customer Success Metrics Investors Care About in 2025 with Gainsight CEO Nick Mehta

-

SaaStr 793: The 10-Point Checklist For When You Sell Your Company with David Frankel Managing Partner at Founder Collective and SaaStr CEO and Founder Jason Lemkin

-

SaaStr 792: Why I’m Scared to Buy New SaaS Apps Now with SaaStr CEO and Founder Jason Lemkin

Listen on Apple Podcast, Spotify or Google Podcasts

|

|

|

|

I like to invest in outsiders with a hint of traction and the ability to ship tons of good software that also like sales

That is my investment thesis

|

|

|

|

© SaaStr 2025

644 Emerson St. Suite 200, Palo Alto, CA 94301

If you'd like to stop receiving the SaaStr Weekly, click here

|

|

|

|